Key Takeaways

- Discovery tools earn their seat by producing defensible keyword sets, competitor gap views, and SERP-feature flags in a single export, eliminating manual reconciliation that drains analyst hours across portfolios.

- Technical crawlers did not become obsolete in the AI era because Google confirms AI features run through the same indexation pipeline as standard Search, requiring no additional technical work 3.

- AI-visibility measurement is the open problem, since legacy rank trackers cannot map citations inside AI Overviews; pairing Search Console's generative AI reports 5with a query-set monitor closes the gap.

- Execution and coordination tools emerged because discovery, technical, and AI-visibility layers created a backlog that moved the bottleneck from research to approval workflow and client delivery.

- Agencies pay twice in three predictable overlap zones: standalone rank trackers, duplicate monitoring crawlers, and third-party reporting tools that duplicate native exports and Search Console's direct AI-feature data 5.

- The 2025 selection framework runs one strong tool per layer, audited quarterly against throughput, and chosen in order from discovery through execution rather than the reverse.

Why Agency Tool Stacks Are Being Rebuilt in 2025

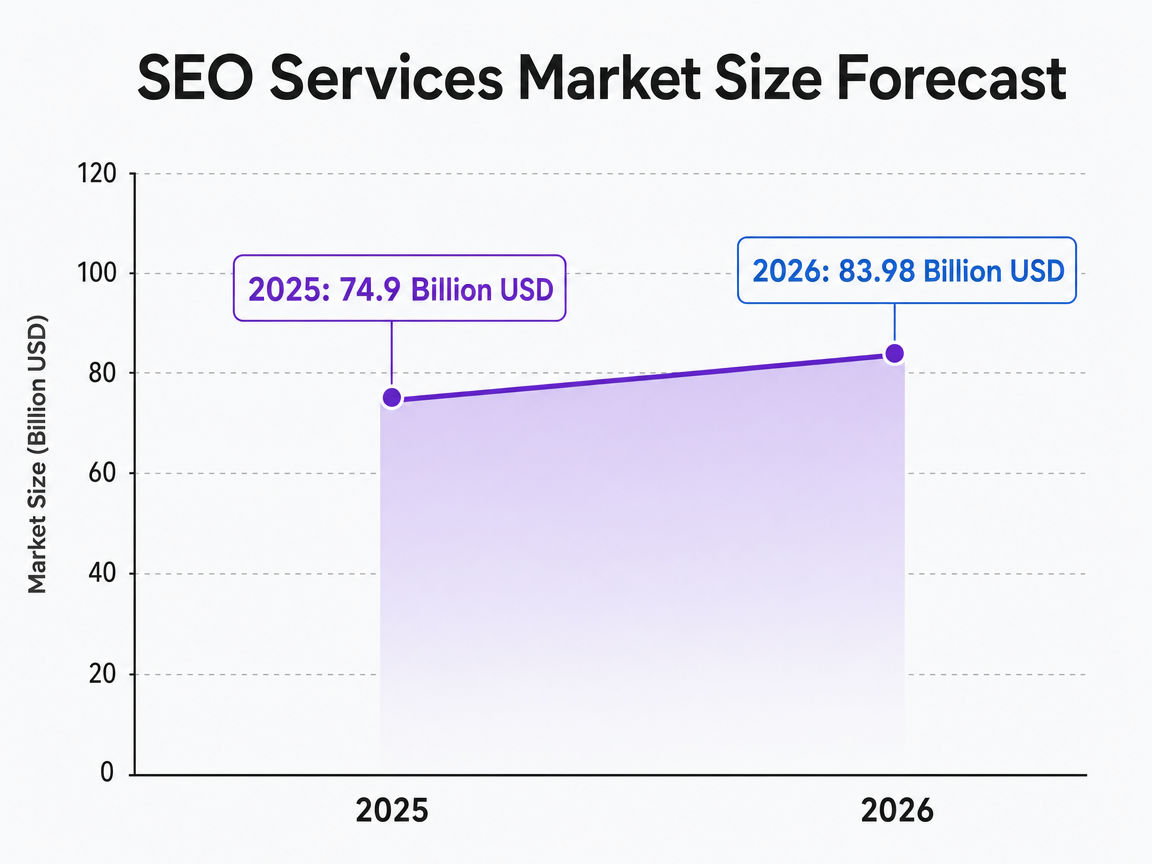

The SEO services market reached an estimated USD 74.9 billion in 2025 and is projected to hit USD 83.98 billion in 2026, expanding at a 12.12% CAGR through 2031 8. That figure measures buyer spend on agency-delivered SEO work, not internal software budgets, which means the demand side is healthy while the supply side, the agencies themselves, face a more complicated question: which tools actually produce that revenue, and which ones quietly drain margin.

Three forces are pulling agency stacks apart at the same time. Google's AI Overviews rolled out broadly across U.S. search in 2024 6, adding a new visibility surface that legacy rank trackers were never built to measure. Search Console now ships dedicated generative AI performance reports, giving agencies a primary-source view of impressions inside AI features rather than a vendor-modeled estimate 5. And Forrester's Q3 2025 Wave assessment confirms what most operators already feel, that SEO platforms have matured into enterprise systems evaluated on strategy, current offering, and market presence rather than feature counts 1.

The result is a stack rebuild driven by margin math, not curiosity. Agencies running 10 to 150 accounts are not adding tools, they are reorganizing them around what each layer must produce per analyst hour.

SEO Services Market Size Forecast

SEO Services Market Size Forecast

Forecasted size of the SEO services market for the years 2025 and 2026.

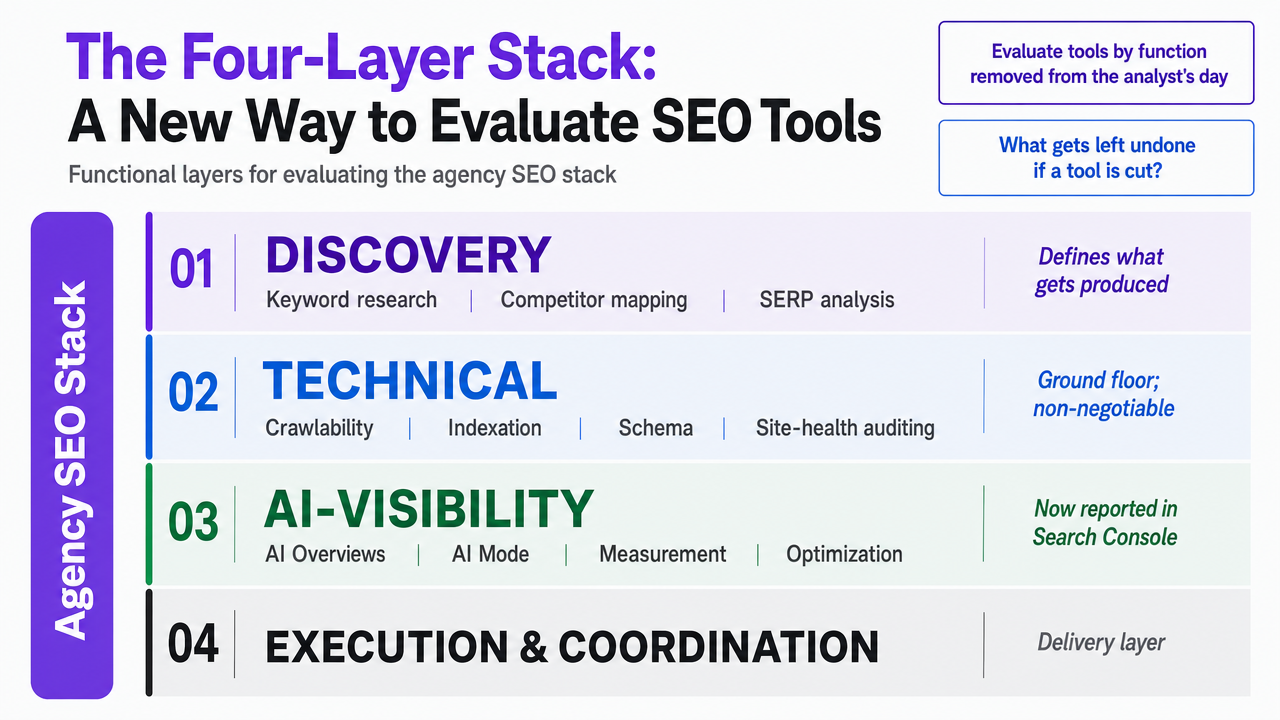

The Four-Layer Stack: A New Way to Evaluate SEO Tools

The flat ranked listicle has stopped being useful. Agencies running real client portfolios do not need to know whether Ahrefs beats Semrush by ten percentage points on backlink index size. They need to know which functions a tool removes from an analyst's day and what gets left undone if that tool is cut.

A more honest model splits the agency stack into four functional layers:

- Discovery covers keyword research, competitor mapping, and SERP analysis, the upstream work that defines what gets produced.

- Technical covers crawlability, indexation, schema, and site-health auditing, the ground floor Google still treats as non-negotiable in its starter guidance 7.

- AI-Visibility covers measurement and optimization for AI Overviews and AI Mode, a surface Google now reports on directly inside Search Console 5.

- Execution and Coordination covers the production, approval, and reporting workflows that determine how many client deliverables a team can ship per month.

Forrester's Q3 2025 Wave evaluated seven enterprise vendors, including BrightEdge, Conductor, Moz, Searchmetrics, Semrush, seoClarity, and Siteimprove, on strategy and current offering 2. Each of those platforms claims coverage across multiple layers, and each is genuinely stronger in some than others. That uneven coverage is the argument for the layered model. An agency buying a single suite expecting parity across all four functions almost always finds two layers underperforming, then bolts on point tools to compensate, then pays for the same capability twice.

The sections that follow work through each layer in order, with the tools that earn their seat and the operator economics that justify them.

Visualize the four functional layers of the agency SEO stack introduced in this section, giving readers a structural map they can reference through the rest of the article

Visualize the four functional layers of the agency SEO stack introduced in this section, giving readers a structural map they can reference through the rest of the article

Test AI-driven SEO execution on live campaigns

Experience measurable workflow efficiency gains by deploying real SEO content across client projects during your trial.

Layer One: Discovery Tools That Still Earn Their Seat

What Discovery Tools Should Produce Per Analyst Hour

Discovery is the layer where analyst time leaks fastest. An analyst running keyword research, SERP analysis, and competitor mapping across a portfolio of fifteen accounts can burn a full day per account per month if the toolset forces manual exports, cross-tab reconciliation, and screenshot-based reporting. The question is not which discovery tool has the largest index. The question is how many client briefs an analyst can produce in a fixed week using it.

Three outputs separate a discovery tool that earns its seat from one that drains margin:

- A defensible keyword set tied to commercial intent, ranked by something more useful than raw volume.

- A competitor gap view that an account manager can paste into a client deck without rebuilding.

- A SERP feature breakdown that flags which queries are now answered inside AI Overviews rather than blue links, since Google began rolling those out broadly in U.S. search in 2024 6.

Tools that produce all three in a single export shift discovery from a research exercise to a production line, which is the only economics that work when one strategist is covering ten or more accounts.

Ahrefs, Semrush, and the Enterprise Discovery Tier

Ahrefs and Semrush remain the default discovery layer for most mid-market agencies, and the reason is not feature parity. It is integration debt. Analyst teams trained on either platform produce client deliverables faster than teams forced to stitch together two or three point tools, and the switching cost for an established agency with template libraries built around one interface is rarely worth the trade.

The enterprise tier sits above both. Forrester's Q3 2025 Wave evaluation included seven vendors, BrightEdge, Conductor, Moz, Searchmetrics, Semrush, seoClarity, and Siteimprove, each positioned as a strategic platform rather than a research utility 2. The Wave assessed strategy, current offering, and market presence across these vendors, which means the comparison is about platform depth, not keyword index size 1. Agencies serving Fortune 1000 accounts or running content programs above roughly 200 published assets per month tend to land in this tier because the discovery work has to feed directly into governance, reporting, and content workflows the smaller tools do not consolidate.

The decision point is straightforward. A mid-market agency running ten to fifty accounts in the SMB or lower-middle-market range gets more throughput from Ahrefs or Semrush than from an enterprise suite, because the enterprise platforms are priced and scoped for in-house teams managing a single complex domain. An agency running fewer than ten accounts but each above seven figures in retainer value starts to justify the enterprise tier on reporting consolidation alone. The wrong move is the middle path, buying an enterprise license and using it as a keyword tool, which is where agencies discover they are paying for capabilities the discovery layer was never meant to deliver.

Layer Two: Technical Tools That Survive the AI Era

Why Crawlability Tooling Did Not Become Obsolete

A persistent vendor narrative in 2024 and 2025 claimed that AI search would reshape what agencies need to audit. Google's own documentation says the opposite. The guidance on appearing inside AI Overviews and AI Mode states there are no additional technical requirements for AI features, and that pages need only be indexed and snippet-eligible to qualify 3. Google reinforces the same point in its broader site-owner documentation, saying the same foundational SEO practices apply to AI features as to Search overall 4.

That single guidance changes the technical tooling argument. If AI-feature eligibility runs through the indexation pipeline rather than a parallel system, then the crawl, render, and indexation diagnostics agencies were running in 2022 are now the prerequisite for AI visibility, not a legacy obligation. The starter guide Google still maintains for SEO fundamentals reinforces that crawlability, structured content, and discoverability remain the most effective improvements a site can make 7.

For an agency, the operational consequence is direct. A crawler that surfaces orphaned pages, indexation gaps, render failures, and schema errors at scale across a portfolio is the layer that determines whether any of the work above it, discovery briefs, content production, AI-visibility tracking, actually compounds into rankings or impressions.

Screaming Frog, Sitebulb, and Platform-Embedded Audits

The technical layer splits into three distinct categories of tool, and most agencies make the mistake of treating them as substitutes. They are not.

- Screaming Frog remains the desktop crawler of record for diagnostic depth. An analyst running a one-time audit on a new client domain or investigating a specific indexation regression gets faster, more granular output from it than from any platform-embedded crawler. The tradeoff is that it is a single-seat, single-machine tool, which means audits are bound to the analyst running them and do not feed automatically into client reporting.

- Sitebulb sits in an adjacent slot. Its strength is the audit narrative, the rendered explanation of what was found and what it means, which shortens the gap between crawl output and a deliverable a client will actually read. Agencies running monthly technical audits across mid-market clients tend to standardize on it for that reason.

- Platform-embedded audits, the site health modules inside the Forrester-named enterprise vendors, BrightEdge, Conductor, Moz, Searchmetrics, Semrush, seoClarity, and Siteimprove 2, occupy the third slot. They are weaker on diagnostic depth than a dedicated crawler but stronger on continuous monitoring and integration with the rest of the platform's reporting. The Forrester Wave evaluates these platforms on strategy and current offering rather than crawler depth specifically 1, which is the point: enterprise audit modules are bought for workflow consolidation, not for the audit itself.

The agency stack that holds up across a 50-client portfolio runs one diagnostic crawler and one continuous-monitoring layer, not both diagnostic tools and not three monitoring layers.

See How Leading Agencies Streamline SEO Execution at Scale in 2025

Connect with our team to benchmark your current SEO tech stack and discover data-driven workflows that reduce production overhead without compromising on quality or client satisfaction.

Layer Three: AI-Visibility Tools and the New Reporting Surface

What Google's Generative AI Reports Actually Measure

Search Console now ships a dedicated set of generative AI performance reports, designed to give site owners impressions data specifically inside AI features rather than mixed in with standard web results 5. That is the first time agencies have a primary-source view of AI-feature visibility, which matters because every vendor estimate before this was a model. The report measures impressions inside generative AI surfaces, which means agencies can finally separate what AI Overviews are showing from what the ten blue links are showing for the same client.

The category response has been faster than the parent market. The AI-powered SEO software market is projected to grow at a 23.4% CAGR, nearly double the 13.37% CAGR estimated for the broader SEO software market through 2032 10, 9. The 23.4% figure measures dedicated AI-SEO tooling spend specifically, not AI features added to incumbent platforms, which is the relevant distinction for agencies deciding whether to add a new line item or wait for their existing vendor to catch up.

Roughly 75% of marketers already use AI to reduce time spent on manual SEO work such as keyword research and meta tag optimization 10. That figure measures self-reported AI use across marketing functions broadly, not agency-specific adoption, and it does not separate occasional from systematic use. It does establish that AI-assisted production is no longer a differentiator at the analyst level. The differentiator has moved to measurement.

Where Legacy Tools Fall Short on AI Overviews

Rank trackers built around position one through one hundred do not map cleanly to a surface where the answer is synthesized above the organic results. An AI Overview can cite a client domain without that domain ranking in the top ten for the underlying query, and it can omit a client ranking at position three. Legacy trackers will report the position three result as a win and miss the AI-feature exclusion entirely. That is not a calibration problem. It is a measurement-model problem.

The second gap is corpus coverage. Most rank-tracking platforms sample SERPs at a fixed cadence on a defined keyword list. AI Overviews trigger on a fluid set of queries that shifts faster than the keyword list refreshes, which means the tool is measuring the wrong universe before it measures position within it. Google's own guidance notes that AI features run through the same indexation pipeline as standard Search and require no additional technical work to qualify 3, which leaves measurement, not optimization, as the open problem.

The practical move for agencies is to pair Search Console's generative AI reports 5with a vendor layer that monitors AI-feature citations across a tracked query set. Agencies running this pairing produce client reports that distinguish AI-feature impressions from organic clicks, which is the deliverable retainers are starting to require.

Layer Four: Execution and Coordination Tools

Why Approval Workflow Became a Tooling Category

The execution layer is the youngest of the four, and it exists because the other three created a backlog. Discovery tools surface more opportunities than analysts can brief. Technical crawlers flag more issues than account managers can route. AI-visibility reports introduce a new client-facing data series that someone has to interpret, summarize, and ship. The bottleneck moved from research to coordination, and the tooling category caught up.

Salesforce's 2026 guide frames AI tools as instruments that assist and augment rather than replace specialists, automating time-consuming tasks such as keyword research, content optimization, and link building so that strategists can focus on planning and creative work 13. That framing is the operating principle behind approval-workflow tools. Production runs on automation. Judgment runs through human sign-off. The tool's job is to keep those two streams in sync without forcing an analyst to act as the courier between them.

For agencies, the consequence is a category that did not appear in Forrester's Wave because the Wave evaluated SEO platforms, not coordination layers 1. The execution slot is filled by approval workflows, briefing automation, and publishing pipelines that sit above the SEO platform and route work through a defined sequence of human checkpoints rather than slack threads and shared spreadsheets.

Throughput Comparison: Traditional Stack vs Consolidated Execution

The clearest way to see the execution layer's effect is to compare what a single analyst produces per client per month under each configuration. The table below uses the Forrester-named enterprise vendor set for the traditional column 2and a consolidated execution layer for the comparison. Hours and cadence are expressed as variables because they vary by account complexity, not as invented benchmarks.

| Variable | Traditional Multi-Tool Stack | Consolidated Execution Stack |

|---|---|---|

| Tools in active use | 4 to 6 (discovery + crawler + rank tracker + reporting + one Forrester-tier platform such as BrightEdge, Conductor, Moz, Searchmetrics, Semrush, seoClarity, or Siteimprove) | 2 to 3 (discovery + crawler + execution layer) |

| Analyst hours per client per month | H baseline (manual exports, cross-tool reconciliation, deck assembly) | Roughly 0.5H to 0.7H (briefs, audits, and reports routed through one approval queue) |

| Reporting cadence achievable | Monthly, with quarterly deep-dives | Weekly summary, monthly deep-dive |

| Number of accounts per strategist | A baseline | 1.4A to 1.8A at equivalent quality |

| Pricing | Per published pricing across vendors; enterprise tier typically requires annual contracts | Per published pricing; typically per-seat or per-account SaaS |

The throughput gain is not a software comparison. It is a coordination gain. When briefs, audits, and reports route through one approval queue, the analyst stops switching contexts between four interfaces and the account manager stops chasing status updates. That is where the hours come from. The Forrester-tier platforms still do the heavy lifting on discovery and technical analysis. The execution layer changes how that output gets reviewed, approved, and delivered.

Where Vectoron Fits in the Execution Layer

Vectoron sits in the execution and coordination slot, not the discovery or technical slots. The platform routes SEO production, content drafts, and reporting through a Command Center where every recommendation includes the strategic reasoning behind it and nothing ships without human sign-off. The model is approval-first automation, which maps directly to the Salesforce framing of AI tools as augmentation rather than replacement 13.

For agencies, the relevant question is what the execution layer does to the rest of the stack. It does not replace Ahrefs, Semrush, Screaming Frog, or a Forrester-tier enterprise platform. It replaces the manual coordination overhead that sits between those tools and the client deliverable. Agencies running multi-location service verticals, where review cycles are long and stakes are high, tend to feel the gain first because that is where briefing and approval friction compounds fastest across a portfolio.

The selection criterion is straightforward. An execution layer earns its seat when it measurably reduces analyst hours per client without reducing the number of human approval checkpoints. Anything that automates the approval itself belongs in a different category and a different conversation.

Centralize SEO Operations with Live Data and Instant Approval Workflows

Streamline multi-client SEO execution: access automated keyword tracking, content recommendations, and cross-channel reporting in one unified dashboard—purpose-built for agencies managing high-volume, high-stakes accounts.

What to Cut: Overlap Zones Where Agencies Pay Twice

Most agency stacks carry duplicate spend in three predictable places.

- The first is rank tracking. Ahrefs, Semrush, and every Forrester-tier platform 2include native rank tracking, yet a surprising number of agencies still pay separately for a dedicated rank tracker bought before the suite was added. The capability is now a feature, not a tool. The standalone subscription is the line item to cut first.

- The second overlap sits between platform-embedded site audits and a second monitoring crawler. Agencies running a Forrester-tier suite alongside a continuous-monitoring crawler are paying twice for the same dashboard. The diagnostic crawler that runs one-off audits, Screaming Frog or Sitebulb, is not the duplicate. The duplicate is the second always-on monitor, which produces overlapping site-health alerts that account managers triage twice and act on once.

- The third overlap is reporting. Most discovery and technical platforms ship client-ready report builders. Layering a separate reporting tool on top, then a third dashboard for AI-feature visibility now that Search Console publishes generative AI performance data directly 5, creates a stack where the same impressions number lives in four places and reconciles in none. Consolidating reporting into the platform with the strongest client-export workflow, and reading AI-feature data directly from Search Console, removes a paid seat without losing a single client deliverable.

Building the 2025 Stack: A Direct Selection Framework

The selection logic comes down to four questions, one per layer:

- For discovery, which platform produces a defensible brief, gap view, and SERP-feature flag in a single export that an account manager will not have to rebuild.

- For technical, which crawler runs deep diagnostics on demand and which monitoring layer feeds continuous site-health data into client reporting without duplicating it.

- For AI-visibility, whether Search Console's generative AI reports 5are paired with a query-set monitor that distinguishes AI-feature citations from blue-link rankings.

- For execution, whether the coordination layer cuts analyst hours per client without removing the human approval checkpoints that protect quality.

The order matters. Agencies that start with execution and back into discovery rarely choose well, because the execution layer's value depends on what it routes. Agencies that start with discovery and never reach execution stay stuck at the analyst-hours ceiling that triggered the rebuild. The stack that holds up in 2025 is one strong tool per layer, audited quarterly against the throughput it actually produces. Platforms like Vectoron occupy the execution slot; the other three layers stay with the specialists that earn them.

SEO Services Market CAGR (through 2031)

SEO Services Market CAGR (through 2031)

SEO Services Market CAGR (through 2031)

Frequently Asked Questions

References

- 1.Search Engine Optimization Solutions, Q3 2025 - Forrester.

- 2.Every Company Needs An SEO Platform.

- 3.Optimizing your website for generative AI features on Google Search.

- 4.AI Features and Your Website | Google Search Central.

- 5.Introducing Search Generative AI performance reports in Search Console.

- 6.Generative AI in Search: Let Google do the searching for you.

- 7.Search Engine Optimization (SEO) Starter Guide.

- 8.SEO Services Market Size, Share, Industry Report 2031.

- 9.SEO Software Market Size, Share & Growth Report 2032 - SNS Insider.

- 10.AI-powered SEO Software Market Size | CAGR of 23.4%.

- 11.SEO Software Market Size, Share, Growth, Analysis, Report, 2034.

- 12.North America SEO Software Market Size | Analysis 2031.

- 13.AI for SEO: Your Guide for 2026 - Salesforce.