Key Takeaways

- Vendor shortlists shift past ten locations because coordination cost, not creative quality, becomes the constraint, and per-location billing models break at scale.

- Six operator filters disqualify vendors quickly: account-level execution, full-funnel attribution, real HIPAA posture, integrated channels, publish velocity, and local adaptation without brand drift.

- Traditional full-service agencies excel at brand and high-production work but hit throughput ceilings once a group needs sustained location-page output across 20-plus sites.

- Point-solution specialists win on channel depth yet force the in-house team to become the integration layer across five dashboards, invoices, and quarterly reviews.

- In-house augmentation and fractional CMO models give operators control but cap throughput, often requiring specialist vendors to cover production volume during expansion.

- AI marketing operating systems run strategy and execution against the account, and only qualify if they actually publish, bid, and acquire links rather than just recommend.

- Cost curves diverge sharply from 5 to 30 sites: per-location retainers scale linearly, centralized agencies dampen the slope, and platform models flatten it.

- The centralization-versus-localization debate resolves into a single account-level plan paired with location-level adaptation on copy, bids, reviews, and referral outreach.

- Seven vendor archetypes deserve evaluation, from hospital-system retainer agencies and DSO specialists to PPC shops, listings platforms, reputation tools, referral CRMs, and Vectoron's operating-system model.

- A 30-day evaluation cycle—internal brief, four-vendor shortlist, working-session 90-day plans, then reference and BAA verification—prices the two-year commitment at projected site count.

Why the Vendor Shortlist Looks Different at 15 Locations

A marketing vendor that performs at three locations rarely performs at fifteen. The breakpoint is not creative quality or healthcare experience, but coordination cost. Once a group crosses roughly ten sites, per-location account managers, separate reporting decks, and parallel approval queues consume more leadership time than the campaigns themselves produce in patient volume.

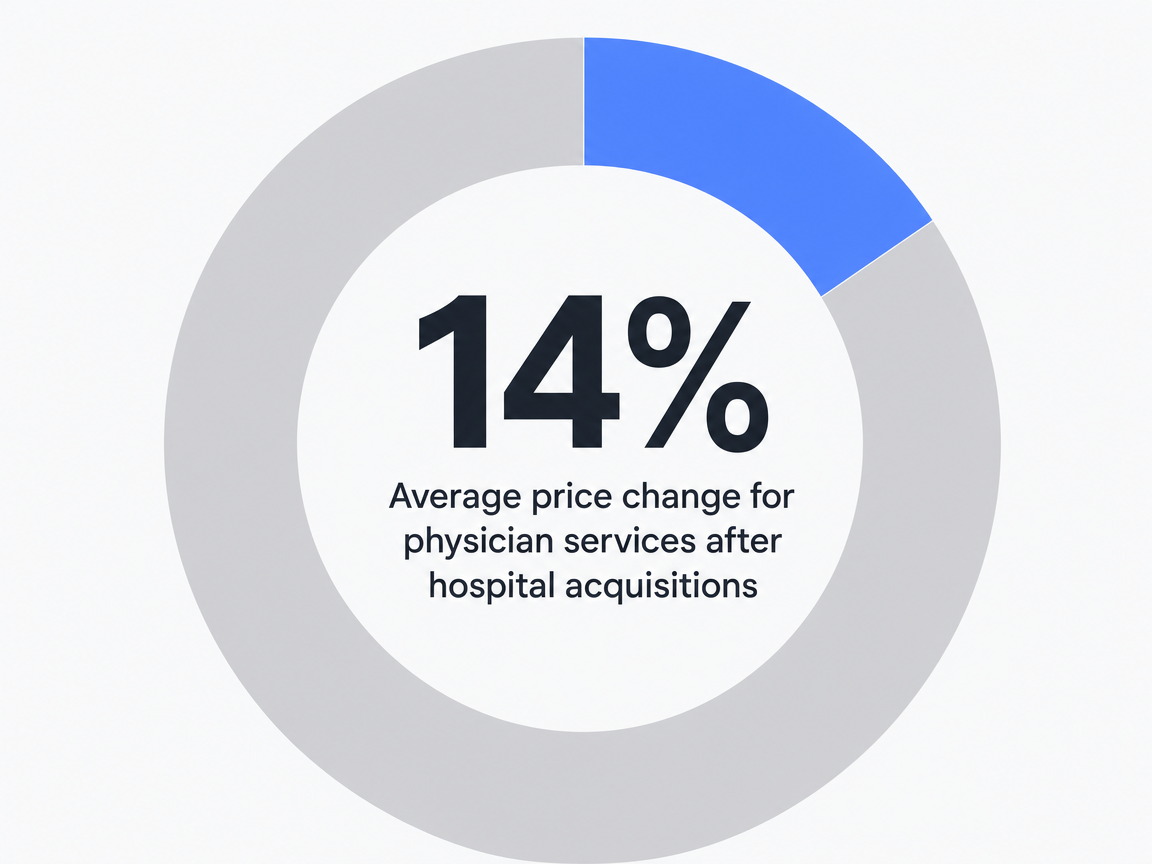

The pressure is not abstract. Hospital-to-hospital mergers can raise prices 6 to 65 percent, and physician practice acquisitions push prices up roughly 14 percent on average, meaning consolidated groups now operate under sharper payer and policy scrutiny than independent practices ever faced 4. Marketing must defend its share of revenue with attribution that ties spend to scheduled visits, not just impressions.

Average price change for physician services after hospital acquisitions: 14%

Average price change for physician services after hospital acquisitions: 14%

The execution gap is the deeper issue. Healthcare leaders who connect data to execution outperform peers who treat strategy as a separate exercise from delivery 9. At 15 locations, the vendor question stops being "who has medical experience" and becomes "who can run a single account-level plan across every site without manual handoffs breaking the system." The shortlist that follows is built around that filter.

Six Operator Criteria That Disqualify Vendors in 20 Minutes

Account-Level Execution vs. Per-Location Billing

The first qualifying question is structural: does the vendor price and execute against the account, or against each address? Per-location retainers create a math problem that gets worse as the group grows. A 22-clinic urgent care brand running the same vendor at every site pays for the same strategy work 22 times, then absorbs the coordination tax of 22 status calls.

Account-level vendors price against a single growth program covering every site, service line, and channel under one plan. The test in a sales call is direct. Ask how the proposal scales from 12 to 30 locations. If the answer is a multiplier on a per-site fee, the model breaks at scale. If the answer separates account-level strategy from location-level adaptation, the conversation is worth continuing.

Attribution Depth Across the Full Funnel

Last-click reporting flatters paid search and starves the channels that actually move patient decisions. Response hierarchy research shows prospects pass through awareness, consideration, and decision stages, and marketing communications must address each stage to convert efficiently 5. A vendor that cannot map content, organic, paid, and referral activity to the same patient journey will optimize toward whatever fires last.

The diligence question is whether the vendor instruments GA4, Search Console, the call tracking layer, and the EHR or scheduling system into one attribution view at the account level. If reporting is delivered as a per-location PDF deck, the group is buying a presentation, not an attribution system. Ask to see a live dashboard from an existing multi-site account before signing.

Compliance Posture Beyond a HIPAA Checkbox

HIPAA marketing rules require authorization for any use or disclosure of Protected Health Information for marketing purposes, with narrow exceptions for face-to-face communications, nominal promotional gifts, refill reminders, and care coordination 3. Most vendor pitch decks claim compliance. Few can describe how their pixel configuration, retargeting audiences, and CRM enrichment respect that line.

The 20-minute filter is whether the vendor can explain, without consulting legal, how they handle conversion tracking on appointment-request pages, how they segment audiences without ingesting PHI, and what their Business Associate Agreement actually covers. Vague answers signal the group will own the regulatory risk while the vendor owns the campaign upside.

Channel Integration in a Single Plan

Omnichannel research is consistent: patient experience improves when channels operate in a harmonized environment rather than as parallel silos, and integration is a primary source of competitive advantage 1. Most vendor stacks fail this test by design. SEO sits at one agency, paid at another, reputation at a third, and the content engine answers to none of them.

Operators evaluating a primary vendor should ask what a single quarterly plan looks like across content, SEO, PPC, and link acquisition, and which strategist owns the trade-offs between them. If four people answer that question separately, the group is the integration layer.

Execution Velocity From Brief to Publish

Healthcare leaders who connect data to execution outperform peers who treat strategy as a separate exercise 9. Velocity is where most retainer relationships quietly fail. A service-line page that takes nine weeks from brief to publish across legal, clinical review, and agency revisions has already missed the demand window it was meant to capture.

The relevant benchmarks are concrete. How many days from approved brief to published location page? How many net-new pages per month across the account? How does the vendor handle medical accuracy review without adding two-week loops? Vendors that cannot answer in days lose to vendors that can.

Local Adaptation Without Losing Brand Control

The centralization-versus-localization argument is usually framed as a binary, and the binary is wrong. Generic centralized templates underperform because patient demographics, payer mix, and competitive intensity vary by metro. Pure local autonomy underperforms because brand voice fragments and compliance review collapses. Healthcare marketing has been moving from mass approaches to specific targeting and from generic messaging to personalization for years 2, and multi-site groups need vendors who can hold both ends.

The operator question is procedural: how does the vendor adapt a service-line page for a market with three competing groups versus a market with none? If the answer is a swap of city names, the local strategy is cosmetic.

Experience Unified Healthcare Marketing Execution Instantly

Test-drive coordinated, multi-location campaigns and publish live content with full system access during your free trial.

Four Vendor Archetypes and How They Behave at Scale

Traditional Full-Service Agencies

Full-service healthcare agencies built their reputations on hospital systems and academic medical centers. The model is recognizable: a senior strategist, an account director, a creative team, and a media buyer assigned to a named client, billed on retainer. At three to five locations, the model holds. The account director can hold the whole footprint in their head, and creative work moves through one approval queue.

Past ten sites, the cracks show. Every new location adds a status meeting, a reporting deck, and a creative brief that competes with the others for the strategist's attention. Pricing typically scales as a base retainer plus per-location add-ons, and groups end up paying twice for strategy work that should be account-level once. These agencies remain strong choices for brand campaigns, system-level positioning, and high-production video. They are weaker choices for groups that need 40 net-new service-line pages a quarter across 25 locations, because production volume runs into the same headcount ceiling that healthcare leaders cite when they describe execution discipline as the next defining capability 9.

Point-Solution Specialists (SEO, PPC, Reputation, Referral)

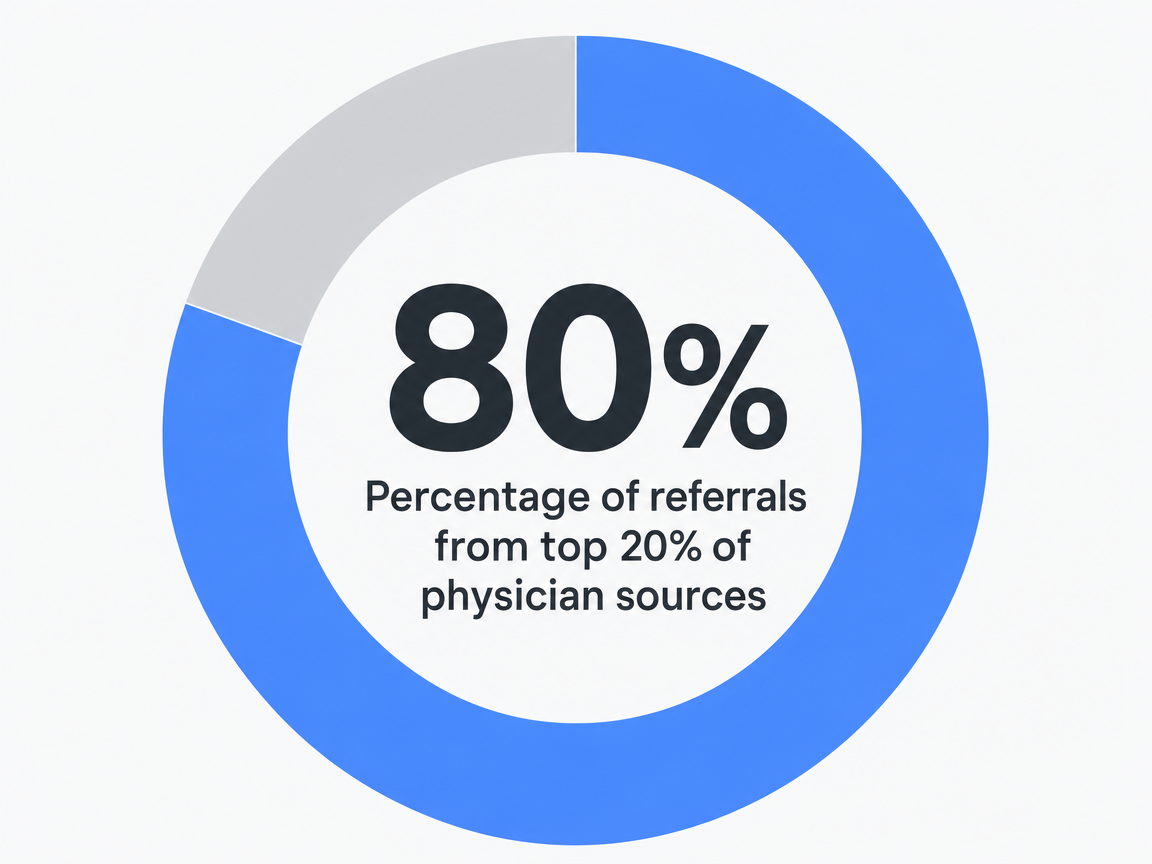

Specialist vendors win on depth in one channel. A local SEO platform manages listings and schema across hundreds of sites. A paid-search shop runs Google Ads and Performance Max with healthcare-specific bid strategies. A reputation vendor handles review solicitation and response. A referral platform tracks physician liaison activity against the 80/20 rule that governs most specialty groups, where roughly 80 percent of referrals come from 20 percent of sources 7.

Each one outperforms a generalist inside its lane. The problem appears at the seams. Five specialists produce five dashboards, five invoices, and five quarterly business reviews, and none of them owns the trade-off when paid search cannibalizes organic traffic on the same service-line keywords. Omnichannel research is direct on this point: integration across channels is itself a source of competitive advantage, and fragmented stacks forfeit it 1. Groups that go this route should expect the VP of Marketing or a senior in-house lead to function as the integration layer, full time.

In-House Augmentation and Fractional CMO Services

The augmentation model places a fractional CMO, a contract content lead, or a small embedded pod inside the operator's team. Pricing usually runs as a monthly fee per role, sometimes with a project layer for campaigns. The appeal is control. The senior strategist reports into the operator's leadership, attends the same standups as in-house staff, and treats the brand as a single account rather than one client among twenty.

The ceiling is throughput. A fractional CMO and two contractors can run strategy, edit content, and manage vendors, but they cannot produce 50 location pages, 12 service-line briefs, and a quarterly link plan in the same month. Multi-site groups that adopt this model often pair it with one or two specialist vendors to cover production volume. The combination works when the in-house lead has the bandwidth to coordinate the stack. When that bandwidth disappears during a roll-up or service-line launch, output stalls.

AI Marketing Operating Systems

The newest archetype runs strategy and execution as a single account-level system rather than a roster of humans. Specialist AI strategists handle content production, SEO, paid search, and link acquisition against one plan, with operator approval gates between strategy and publishing. Pricing is typically platform-based and does not scale linearly with location count. BCG's analysis of healthcare AI adoption is consistent with the design intent: organizations that succeed concentrate on a small number of transformative AI applications rather than running dozens of disconnected pilots 6.

The relevant test for operators is whether the system actually executes or simply recommends. A platform that generates 200 keyword opportunities and a content calendar is a research tool. A platform that produces approved location pages, ships technical SEO fixes, manages bids, and acquires backlinks against a single attribution view is an execution layer. The first replaces a research seat. The second replaces the agency relationship, which is the economic shift that makes the category interesting at 15-plus sites.

Consolidation Economics: How Cost Behaves From 5 to 30 Sites

The cost question is not which vendor is cheapest, but how the bill behaves as the footprint grows. Three vendor models scale differently, and the differences compound past 15 sites.

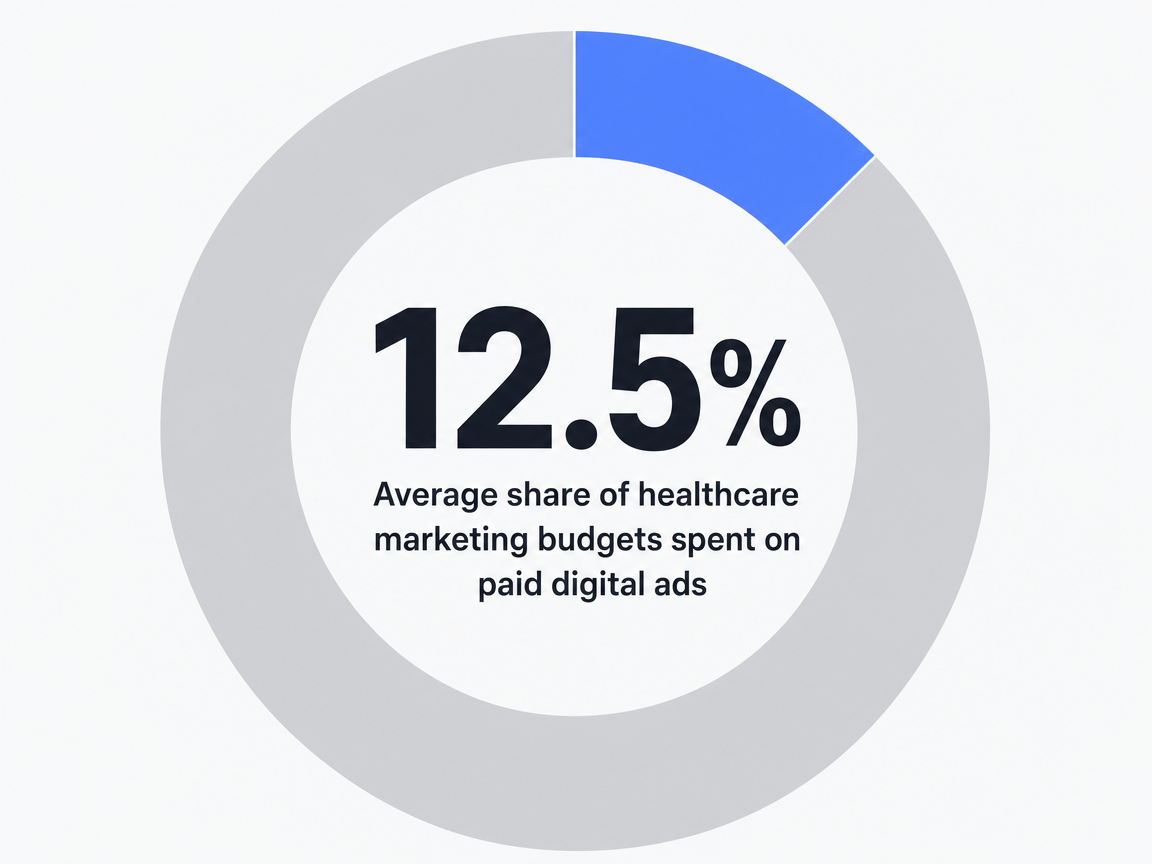

The table below compares cost behavior across the three archetypes that compete for multi-site work. Retainer figures are illustrative variables labeled as ranges, not vendor quotes. The paid-digital share reflects the 12.5 percent benchmark healthcare marketers reported in 2022 8. The platform trial figure reflects publicly stated entry pricing for AI marketing operating systems in this category.

Average share of healthcare marketing budgets spent on paid digital ads: 12.5%

Average share of healthcare marketing budgets spent on paid digital ads: 12.5%

| Dimension | Per-Location Retainer Agency | Centralized Agency + Add-Ons | Account-Level AI Operating System |

|---|---|---|---|

| Monthly cost structure (5 sites) | 5 × per-site retainer (variable R) | Base retainer + 5 × location fee | Single platform fee, trial entry near $599/mo |

| Monthly cost structure (15 sites) | 15 × R, near-linear | Base + 15 × location fee | Single platform fee, sub-linear scaling |

| Monthly cost structure (30 sites) | 30 × R, fully linear | Base + 30 × location fee, partly linear | Single platform fee, flat to step-function |

| Coordination overhead | 1 account manager per 4-6 sites | 1 lead + junior coordinators per region | Operator approval queue, no AM layer |

| Execution latency (brief to publish) | 4-9 weeks per asset | 3-6 weeks per asset | Days to under two weeks per asset |

| Attribution scope | Per-site reporting decks | Rolled-up dashboard, per-site PDFs | Account-level dashboard across sites |

| Paid-digital share of budget | ~12.5% benchmark, executed per site 8 | ~12.5% benchmark, partial pooling | ~12.5% benchmark, pooled at account |

The pattern is mechanical. Per-location retainers scale linearly with site count because the unit of billing is the address. Centralized agencies dampen the slope but still add a marginal fee per site to cover account management. Platform models flatten the curve because the unit of billing is the account, not the address.

Two cautions belong on the table. Lower cost curves do not guarantee better outcomes, and execution discipline is what separates platforms that publish from platforms that recommend 9. The diligence work is verifying that the flatter cost curve still produces the page count, the bid changes, and the link placements an operator can audit each month.

Scale Multi-Site Healthcare Marketing with AI-Driven Precision

Discover how leading healthcare groups and agencies unify content, PPC, and SEO execution across all locations with data-backed automation. Request a tailored demo and benchmark your current marketing performance.

The Centralization-vs-Localization Question, Settled

The question is usually framed as a choice. It is not. Centralized strategy with locally adapted execution outperforms either pure model, and the evidence sits in two places. Omnichannel research treats integration across channels as a primary source of competitive advantage, which only works when one team holds the plan 1. Healthcare marketing has also shifted from mass approaches toward specific targeting and personalization, which only works when execution adapts to local payer mix, competitor density, and patient demographics 2.

The practical model is a single account-level plan that defines positioning, service-line priorities, attribution rules, and brand standards, paired with location-level adaptation on landing page copy, paid bids, review response, and referral outreach. A 9-clinic urgent care brand in a fragmented metro should not run the same paid budget per site as the same brand in a market with two hospital-owned competitors. The strategy is shared. The execution variables are not.

Vendors that cannot describe both layers in one sentence are selling half the system. The disqualifying answer in a sales call is any version of "we centralize everything" or "we customize per location." The qualifying answer names which decisions live at the account and which live at the site.

Seven Vendors Worth a Real Evaluation Cycle

A Traditional Healthcare Retainer Agency Built for Hospital Systems

The category is anchored by full-service agencies serving health systems, academic medical centers, and large regional brands. The work is heavy on brand campaigns, service-line launches, and broadcast-grade creative. Strategy and account leadership are senior, and creative review is rigorous. The trade-off is throughput. Production runs through human teams against retainers that scale with location count, and groups managing 20-plus sites typically find that the same strategist cannot hold every market in equal focus. The fit is system-level positioning and high-production work, not weekly location-page output.

A Specialty-Focused DSO and MSO Agency

Specialty-focused shops know dental, dermatology, ophthalmology, orthopedics, or behavioral health well enough to write briefs without a discovery call. They understand payer-mix dynamics, recall cycles, and the referral patterns that drive specialty volume. Pricing is usually a base retainer with per-location creative and media management fees. The strength is vertical fluency, particularly around service-line growth and de novo openings. The weakness shows when a 22-location dermatology group asks for unified attribution across organic, paid, and referral channels and receives three separate decks instead of one account view.

A Performance PPC and Paid Social Specialist

Paid-media specialists win on bid-strategy depth, conversion-pixel discipline, and healthcare-aware audience structures that respect HIPAA constraints on retargeting 3. The 12.5 percent paid-digital benchmark sits inside their lane, and they tend to outperform generalists on cost-per-scheduled-visit at the campaign level 8. The constraint is scope. A PPC specialist optimizes against the funnel stage they touch, not the full hierarchy of effects that moves prospects from awareness to decision 5. Groups that hire one will need a separate owner for organic, content, and the trade-offs between channels.

A Local SEO and Listings Management Platform

Listings platforms manage Google Business Profiles, schema, citations, and review syndication across hundreds of locations from one console. The technical surface area they cover is real, particularly for groups whose local pack rankings drive a meaningful share of new-patient volume against the billion-plus daily health queries Google handles 10. The limit is content. Listings hygiene does not produce the location pages, service-line briefs, or condition-specific articles that organic visibility requires past a certain ranking threshold. The platform is a layer in the stack, not the stack.

A Reputation and Patient Experience Vendor

Reputation vendors automate review solicitation, route negative feedback to operations, and surface CAHPS-adjacent signals from open-text comments. The category matters because referred and self-referred patients research providers online before scheduling, and review depth correlates with conversion at the site level 7. The compliance line is sharper than it looks. Solicitation flows that touch appointment data must respect HIPAA marketing rules on PHI use 3. The vendor handles a real problem, but no reputation platform produces demand. It converts demand other channels create.

A Referral Marketing and Physician Liaison Platform

Referral platforms equip physician liaisons with CRM workflows, source-level reporting, and pull-through tracking against the 80/20 distribution that governs most specialty referrals, where roughly 80 percent of referrals come from 20 percent of sources 7. For specialty multi-site groups, the category is non-optional. The work the platform does well is operational, including visit logging, tier scoring, and follow-up cadence. What it does not do is connect referral activity to the digital channels that influence the same referring physicians, who increasingly research a specialty group's online presence before sending a patient 7. Integration with the broader marketing stack is the diligence question.

Percentage of referrals from top 20% of physician sources: 80%

Percentage of referrals from top 20% of physician sources: 80%

Vectoron: An AI Marketing Operating System for Multi-Site Groups

Vectoron sits in the operating-system category and runs strategy and execution against the account rather than the address. A Lead Strategist coordinates specialist strategists for content, SEO, conversion, PPC, and backlinks, with a Command Center where operators approve work before it ships. Production covers location pages, service-line content, technical SEO fixes, bid management, and targeted link acquisition under one plan, with attribution surfaced at the account level rather than rolled up from per-site decks. The design intent matches BCG's finding that healthcare organizations succeed with AI by concentrating on a small number of transformative applications rather than running disconnected pilots 6. Trial pricing starts at $599 per month, and the model does not bill per location, which changes the cost curve at 15 and 30 sites in ways the earlier table makes mechanical.

Unlock Unified Medical Marketing for Every Site—Data-Driven, Scalable, Proven

Access a centralized platform for executing SEO, PPC, and content strategies across all healthcare locations, backed by AI-driven analytics and measurable performance gains—no added headcount required.

Running the Evaluation: A 30-Day Path to a Decision

A disciplined evaluation cycle fits inside one month. Week one is internal: pull the last four quarters of spend by channel and location, identify the three service lines driving the most revenue, and write a one-page brief covering footprint, attribution gaps, and the page-production volume the in-house team cannot meet. Vendors cannot scope what the operator has not measured.

Week two narrows the field to four candidates spanning at least two archetypes. Send each the same brief and require live dashboard access from a comparable multi-site account, not screenshots. Score responses against the six criteria from the earlier framework. Vendors that cannot produce account-level reporting in week two will not produce it in month six.

Week three runs working sessions, not pitch decks. Ask each finalist to draft a 90-day plan covering one service line across five sample locations, with named deliverables, weekly publish counts, and bid-management cadence. Health systems perform best when strategy translates into measurable performance with clear accountability 9, and a concrete plan is the cheapest way to test whether the vendor can.

Week four is verification. Reference-check two existing accounts at similar site counts, confirm the Business Associate Agreement language against actual pixel and audience configurations 3, and price the two-year commitment at projected site count rather than today's. Sign the vendor whose cost curve, attribution scope, and execution velocity hold up at the footprint the group will operate twelve months from now.

Frequently Asked Questions

References

- 1.An Overview of Omnichannel Interaction in Health Care Services.

- 2.The Impact of Marketing Strategies in Healthcare Systems.

- 3.What are the HIPAA Marketing Rules?.

- 4.Health Care Provider Consolidation.

- 5.Response Hierarchy Models and Their Application in Health Care.

- 6.How AI Agents and Tech Will Transform Health Care in 2026.

- 7.A Guide to Maximizing Physician Referral Strategies.

- 8.U.S. Healthcare Firms' Marketing Budget Share 2025.

- 9.Execution, Alignment and Accountability Define the Next Era of Healthcare Leadership.

- 10.SEO for Healthcare: How to Boost Your Medical Practice's Organic Traffic.

- 11.The impact and challenges of digital marketing in the health care ....

- 12.Big data-driven public health policy making: Potential for the ... - PMC.