Key Takeaways

- Traditional agencies clear only 2-3% net margins while engineering-led firms hit 40%+ on comparable revenue, because revenue compresses as AI replaces billable execution while coordination payroll stays rigid 3.

- Generative AI now produces briefs, drafts, and reporting at mid-career quality, yet agencies have not repriced rate cards, so 91% of leaders are cutting headcount instead of adjusting fees 8.

- Concentrated creative talent and media access no longer protect margins; durable advantage now comes from engineering capacity, with top firms allocating 20-30% of payroll to data and engineering roles 3.

- The flat monthly retainer billed for presence, not outcomes, and is being repriced into a defined production output plus a performance layer tied to metrics clients already track in GA4 and CRMs 6.

- With 85% of US B2C marketing executives planning agency reviews in 2026, CMOs are comparing retainers against in-house teams, specialist boutiques, and platform-delivered production priced on deliverables 2.

- Cutting juniors protects quarterly margins but dismantles the apprenticeship pipeline that produced senior strategists; surviving roles must be engineering-adjacent, focused on prompt design, quality systems, and output review 8.

- Across delivery models, only the traditional retainer carries coordination as its largest cost line, which is precisely what AI substitution and client transparency are repricing away 1.

- Holding company retrenchment, like WPP's $676M cost-cutting program, lowers expenses without changing unit economics, while specialist boutiques with narrower scope grew at roughly twice the industry average in 2025 7.

- Engineering-led firms position senior judgment only at the brief and approval stages, run drafting and reporting through automated workflows, and treat the production system itself as the durable competitive asset 4.

- The next contract cycle forces a binary choice: trim headcount inside the old retainer model, or rebuild delivery around production systems and outcome pricing before clients reprice the work themselves 3.

The P&L Math That Stopped Working

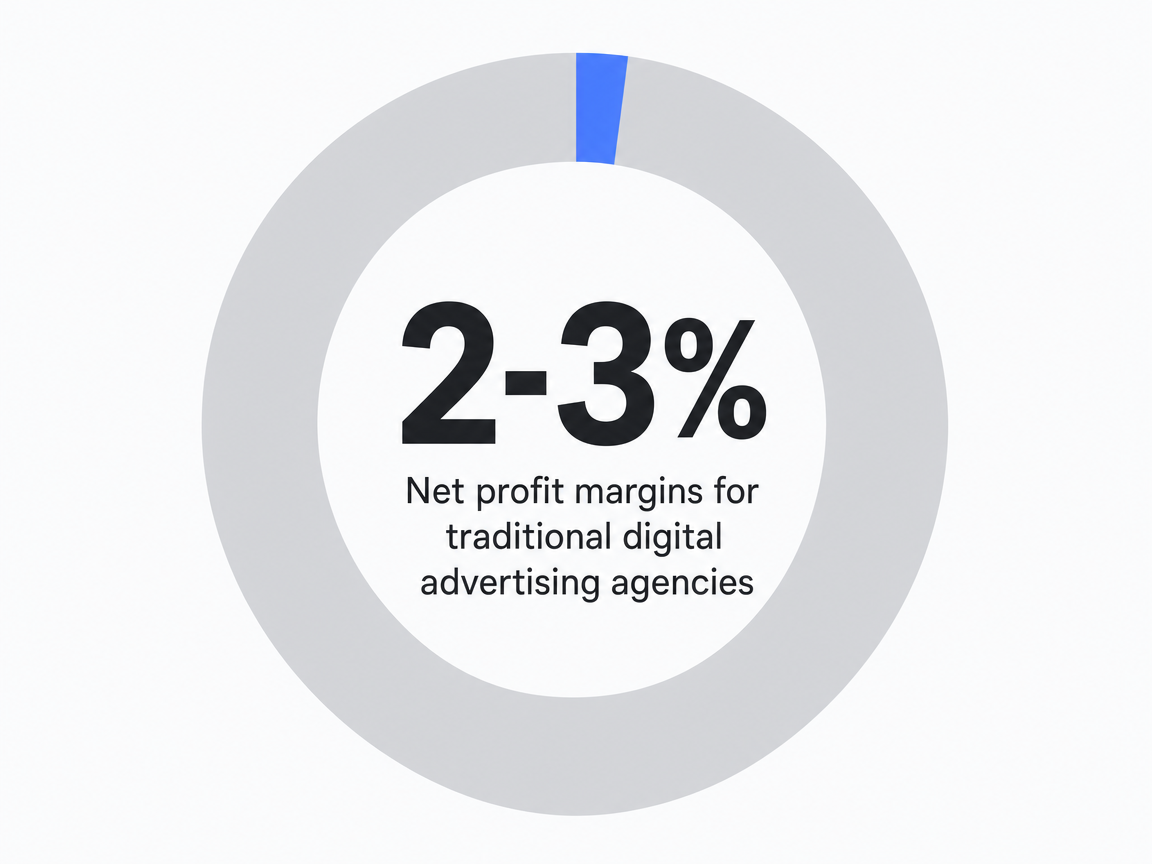

Net margins at traditional digital agencies have compressed to 2-3%, while engineering-led firms operating in the same digital advertising market are clearing 40%+ on comparable revenue 3. This disparity highlights a fundamental difference in business models, not just a competitive gap.

Net profit margins for traditional digital advertising agencies: 2-3%

Net profit margins for traditional digital advertising agencies: 2-3%

A 2026 survey of over 200 advertising professionals found that 87% believe the traditional agency model is broken or will be within three to five years, with 92% of senior leaders deeming it unsustainable 1. This widespread sentiment among those responsible for payroll signals a significant financial shift.

The financial challenges stem from both sides of the income statement simultaneously.

On the revenue side, deliverables agencies bill for—such as campaign builds, creative iterations, reporting, content drafts, keyword research, and bid adjustments—are now produced by AI at a quality level comparable to a mid-career professional 8. Clients are aware of this cost curve and are pricing services accordingly.

Conversely, on the cost side, major expenses like account managers, coordinators, junior strategists, and QA reviewers, along with the entire process of internal handoffs, cannot be reduced quickly enough. These roles were integral to the old model, facilitating the journey of a brief from client email to published asset, and enabling a 30-person agency to manage a $10M book.

The combination of revenue compression and cost rigidity has resulted in a P&L that no longer balances at the volumes agencies historically required. This arithmetic problem underpins all subsequent analysis.

Why Execution Labor Lost Its Price

AI Reached Mid-Career Output Before Agencies Repriced

The value of labor agencies bill for has a new baseline. Generative AI systems now produce campaign briefs, ad variants, keyword clusters, content drafts, performance summaries, and audience segmentations at the quality level of a mid-career professional, as noted by senior agency leaders 8. This single development has fundamentally altered the value proposition agencies were built upon.

For two decades, agency P&Ls were structured around a labor pyramid: junior staff produced, mid-level strategists shaped, and seniors approved. Margins were derived from the difference between junior staff costs and the billing rate for their output. AI did not enter at the base of this pyramid; it entered in the middle, displacing the highest-margin billable hours.

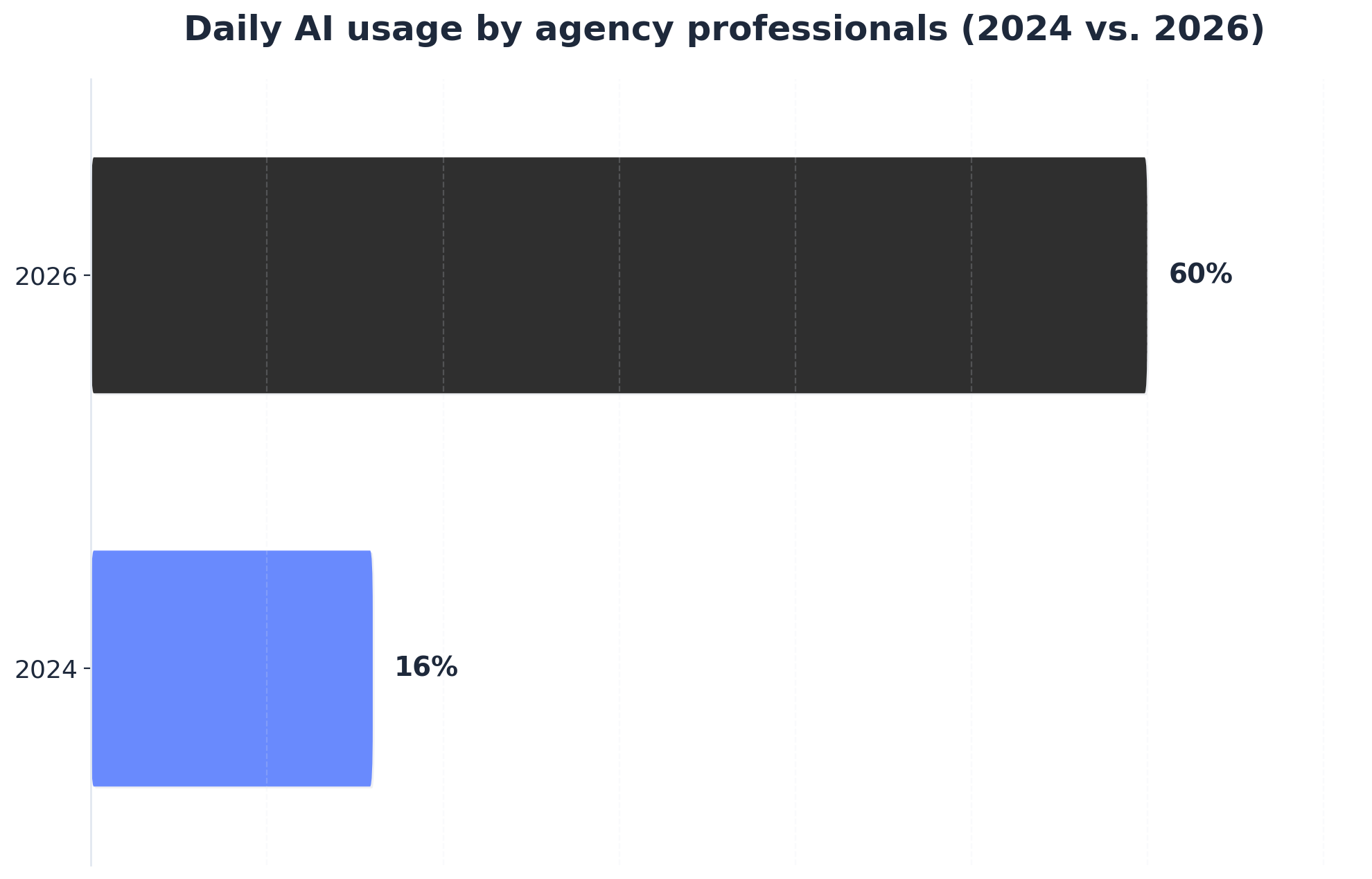

The rapid adoption curve confirms client awareness. Daily AI use among agency professionals surged from 16% in 2024 to approximately 60% in 2026 1. Clients, using the same tools, understand the actual cost of producing a draft and are negotiating from this informed position.

Daily AI usage by agency professionals (2024 vs. 2026)

Daily AI usage by agency professionals (2024 vs. 2026)

Daily AI usage by agency professionals (2024 vs. 2026): 2024: 16%, 2026: 60%. Illustrates the rapid adoption of AI tools within agencies over a two-year period. A bar chart comparing the two years would be effective.

Agencies have not adjusted their pricing in response. Most rate cards still reflect 2022 assumptions regarding hours, headcount, and turnaround times. The resulting gap between current production costs and agency charges manifests as compression. This is evident in 91% of senior agency leaders expecting AI to reduce headcount, and 57% having already paused or slowed entry-level hiring 8. Repricing is occurring through workforce contraction, not rate adjustments.

The Eroded Moat: Creative Talent and Media Access

The two historical pillars of agency pricing power—concentrated creative talent and privileged media relationships—no longer provide the same competitive advantage. McKinsey's analysis on competitive advantage emphasizes that durable advantage comes from operating models and hard-to-replicate assets, not capabilities easily acquired or replicated 4. Creative headcount and media buying access fail this test in 2026.

Creative talent has become more distributed. Senior creatives now often work as fractional contractors, run independent studios, or are integrated into the brand teams agencies once served. The premium for housing them under one roof has diminished as the agency structure itself no longer offers a significant recruiting advantage.

Media access followed a similar path. Self-serve platforms made pricing transparent, dashboards revealed performance, and many services agencies once charged premiums for are now handled in-house or by automation software 5. A planner with platform certifications and data access can replicate much of what an agency media desk provided, at a fraction of the cost.

The new asset that does protect margins is engineering capacity. Firms dedicating 20-30% of payroll to data engineers, rather than creative leads, are achieving 40%+ net margins on comparable revenue 3. The competitive moat has shifted, but most agencies have not adapted.

The Retainer Was a Pricing Artifact, Not a Business Model

The monthly retainer, historically an invoicing convenience, allowed agencies to bill for presence rather than measurable outcomes. For much of the digital era, this was sufficient. Clients focused on whether work was being done, not necessarily on its impact. The retainer addressed the former while sidestepping the latter.

This arrangement is now under significant pressure. Industry analysis indicates that retainers are being forced to justify themselves in terms of outcomes, a language they were not designed to speak 6. The fee was based on hours, headcount, and meetings, but clients now demand discussions about tangible results like pipeline growth, qualified leads, ranked pages, and booked appointments, along with their associated costs.

For years, agencies countered attribution questions by citing external variables, client-side execution risks, and multiple channels influencing buyers. This defense held when clients lacked robust measurement tools. However, in 2026, CMOs have access to GA4, Search Console, CRM-linked attribution, and platform-level reporting, enabling them to clearly discern agency contributions.

The procurement implications are substantial. Forrester predicts 85% of US B2C marketing executives will review their media agencies in 2026, and principal media—where agencies sell outcomes—is projected to reach approximately 33% of total agency billings 2. Pricing is increasingly tied to measurable results.

Internally, retainers also obscured agency cost structures. A flat monthly fee covered account manager time, strategist reviews, QA cycles, revisions, and status calls, none of which were itemized for the client. As pricing shifts to outcomes, this hidden coordination labor becomes visible and is difficult to justify against AI-augmented competitors delivering similar results at a fraction of the cost.

Retainers are not obsolete, but unexamined ones are. Agencies that successfully navigate this repricing are restructuring fees around two components: a defined production output that their delivery system can consistently achieve, and a performance layer linked to metrics the client already measures. Any elements outside this framework are parts of the old P&L that no longer generate sufficient value.

Test Autonomous Marketing Execution With Real Campaigns

Experience full-scale campaign deployment and performance insights before making any commitment.

Client Defection and the Procurement Reset

Client behavior shifted before many agencies recognized the change. Forrester projects that 85% of US B2C marketing executives plan to review their media agencies in 2026, the highest intent recorded by the firm 2. A review is not a renewal; it is a procurement event where agencies must defend their services against new alternatives.

CMOs now have three credible alternatives: an in-house team augmented by the same generative AI tools agencies use, a specialist boutique with a narrower scope and published outcome metrics, or a platform-delivered production system that prices based on deliverables rather than headcount. None of these were viable options in 2022, but all are in 2026.

Procurement language has evolved with these new options. Budget discussions, once focused on scope and headcount, now center on metrics like cost per acquired lead, cost per ranked URL, and cost per produced asset. Agencies built on opaque retainers find themselves explaining staffing decisions to procurement officers who are comparing platform invoices with agency bills 5.

Strained client relationships are reflected in agency data: 54% of professionals cite them as a primary obstacle, and 44% point to inefficient internal processes that clients increasingly identify 1. Defection risk is not primarily due to service failure but because clients can now independently price the work and are no longer accepting previous pricing models.

The Junior Pipeline Problem No One Can Trim Their Way Out Of

While cutting junior staff can quickly protect quarterly margins, it risks long-term damage to the firm. Agencies are nonetheless pursuing this path: 57% of US senior agency leaders have slowed or paused entry-level hiring, and 91% expect AI to reduce overall headcount 8. These cuts are concentrated in roles most susceptible to AI substitution, such as coordinators, junior copywriters, associate analysts, and paid media assistants.

However, these junior roles provided more than just deliverables.

Junior positions served as an apprenticeship. A coordinator performing QA for two years learned about campaign failures. An associate writing meta descriptions for eighteen months understood how search intent translates to revenue. The senior strategists agencies now rely on were developed through this pipeline. Eliminating the bottom rung not only reduces headcount costs but also removes the mechanism that produced the irreplaceable talent within the firm.

The substitution is also asymmetric. AI now performs execution tasks at a mid-career professional level, precisely where junior labor gained training without senior judgment 8. Seniors, retained for client strategy and review, are increasingly handling their own production due to the diminished junior cohort. This increases burnout risk among the critical senior layer, with 70% of agency professionals already reporting harder jobs than two years ago 1.

Agencies successfully navigating this shift are not rebuilding the old pyramid. Instead, they are pairing a smaller senior team with AI-augmented production and re-envisioning junior roles as engineering-adjacent: focusing on prompt design, quality systems, and output review. The talent pipeline is being rebuilt around tools, not around the headcount those tools displaced.

Transform Agency Delivery with Autonomous AI Marketing Execution

See how leading agencies eliminate bottlenecks and scale multi-channel campaigns with an AI-powered team—no added headcount, no missed deadlines. Book a strategy session tailored for high-volume digital marketing operations.

Where the Margin Actually Goes: Three Delivery Models Compared

To understand why the traditional agency model is failing, it's useful to trace the flow of money within a typical client account. Consider a multi-site healthcare operator with six locations, a common client profile for agencies today. The retainer dollar yields vastly different P&Ls depending on the delivery model.

In a traditional retainer agency, the dominant costs are personnel who do not directly produce client-facing output: account managers, project coordinators, traffickers, QA reviewers, and senior strategist hours spent on status calls. Specialist labor—like writers, paid media analysts, and link builders—operates beneath this coordination layer. Net margins in this setup typically range from 2-3% 3, and 44% of professionals within these firms identify inefficient internal processes as a primary obstacle 1. The retainer is substantial because the internal coordination is extensive.

With in-house delivery, the operator exchanges coordination overhead for fixed payroll. A small team of two to four marketers, supported by platform subscriptions, can manage most execution for a six-location footprint. Cost predictability improves. The trade-off is depth: in-house teams often struggle to staff specialist coverage across SEO, paid media, content production, and backlinks with the same headcount, a gap traditional agencies historically filled. Forrester's projected 15% agency headcount reduction in 2026 2 partly reflects clients making this calculation and acting on it.

Under an AI-augmented production model with human approval, the cost structure is inverted. Engineering and tooling account for 20-30% of payroll 3, specialist judgment is applied at the approval stage rather than during production, and coordination costs significantly decrease because briefs move through a system instead of a series of inboxes. Firms operating this way are achieving 40%+ net margins on comparable revenue 3.

| Cost line | Traditional retainer agency | In-house team | AI-augmented production |

|---|---|---|---|

| Dominant payroll allocation | Account management, coordination, QA | Generalist marketers, platform fees | Engineering and tooling (20-30% of payroll) 3 |

| Specialist coverage across SEO, PPC, content, backlinks | Yes, via specialist pod | Limited at typical headcount | Yes, via system plus approval layer |

| Coordination overhead per deliverable | High; cited by 44% of professionals as a primary obstacle 1 | Low to moderate | Low; production runs as a workflow |

| Net margin band on the work | 2-3% 3 | Not a margin question; cost center | 40%+ 3 |

| Pricing logic the client accepts | Presence-based, under review | Internal cost allocation | Output- and outcome-linked |

This comparison highlights that the traditional retainer is unique among the three models in having coordination costs as its largest line item. This is precisely what AI substitution and client transparency are repricing. The margin is not going to the specialist work clients value, but to the extensive apparatus built to move work between specialists.

Consolidation as a Symptom, Not a Strategy

Holding Companies Choosing Retrenchment Over Redesign

The largest agency groups are addressing model failure through financial maneuvers rather than fundamental delivery redesigns. WPP's $676 million annual cost-cutting program, intended to restore growth by 2028, exemplifies this approach: layoffs, real estate consolidation, and operational compression aimed at profitability without rebuilding production methods 7. The Omnicom-IPG combination, valued at approximately $25 billion, falls into the same category—achieving scale through subtraction and merger, not through a new production system 10.

This logic is financially sound from a CFO's perspective but operationally weak. Cutting headcount within a labor-priced delivery model reduces quarterly costs but does not alter the unit economics of future contracts. The retainer still prices presence, deliverables still move through the same handoff chain, and AI substitution continues to impact client-side operations.

Retrenchment offers temporary relief but does not yield the 40%+ margins achieved by engineering-led firms on comparable revenue 3. Holding companies aiming for profitability by 2028 are betting on weathering the transition without redesigning their P&L. Meanwhile, firms already operating with new models are not waiting.

Why Specialized Boutiques Are Outgrowing Generalists

The same market pressures affecting holding companies are benefiting specialized agencies. Agencies that reduced their service offerings in 2025 grew at roughly twice the industry average, with one-third of the sector fully implementing AI by Q2 2026 9. A narrower scope combined with production tooling is outperforming broader scope with increased headcount.

The market structure supports this divergence. North America has approximately 71,000 agencies, 87% of which employ fewer than 50 people 9. This fragmentation is an advantage for specialists, allowing a boutique focused on a single service line, vertical, or buyer profile to run an AI-augmented production system end-to-end without the coordination overhead that burdens generalists.

Valuations reflect these operational results. Agencies with proprietary AI workflows are commanding 1-2x EBITDA premiums in current M&A activity, while generalist shops lacking a defensible delivery system are seeing compressed multiples 10. Buyers are valuing the production model, not just headcount.

In this environment, specialization is not merely a marketing choice; it is a prerequisite for an efficient delivery system. A focused service mix enables standardized production, seamless AI integration, and senior reviewer approval instead of reliance on account managers. Generalist agencies attempting to maintain full-funnel breadth incur a coordination tax that engineering-led approaches have eliminated.

Replace Inefficient Agency Models with Autonomous AI Execution

Gain instant access to a unified AI marketing team that automates strategy, content, PPC, and backlinks—eliminating manual coordination and enabling scalable results across all client accounts.

What an Engineering-Led Delivery Model Actually Looks Like

Firms achieving 40%+ net margins on digital advertising revenue are not merely improving the agency model; they are operating a fundamentally different one 3. The structure of this model is now clear, and the primary distinction from traditional retainer shops lies in where labor is positioned within the production chain.

Three structural choices define the engineering-led firm.

First is payroll allocation. Twenty to thirty percent of headcount is dedicated to data and engineering roles, rather than creative leads, account managers, or coordinators 3. These engineers build and maintain the production system for client work, including ingestion pipelines from GA4, Search Console, ad platforms, and CRMs; standardized brief-to-output workflows; and quality checks implemented as code. The system itself is the asset, allowing headcount to scale sublinearly with revenue as new accounts leverage existing infrastructure.

Second is the placement of senior judgment. In traditional models, seniors review at the end of long handoff chains. In engineering-led firms, senior strategists are positioned at two critical points: the brief, where work is scoped against client outcomes, and the approval, where AI-augmented production output is reviewed before publication. The intermediate steps—drafting, formatting, optimization, and reporting—are handled by automated workflows. This eliminates the coordination burden cited by 44% of professionals as an inefficiency 1.

Third is service scope. Specialization is not a marketing stance but a prerequisite for productizing delivery. Agencies that narrowed their service mix in 2025 grew at roughly twice the industry average 9, and the M&A market values proprietary workflows with 1-2x EBITDA premiums over generalist headcount 10. A focused scope allows a firm to excel at one production system rather than managing multiple poorly.

The operational outcome is a smaller, more senior team supported by a production layer that performs tasks previously handled by an entry-level pyramid, but at a predictable cost. This model aligns with McKinsey's description of a hard-to-replicate operating asset rather than a readily available capability 4. It is also the model that holding companies focusing on retrenchment are not building.

The Operator Decision Ahead

Agencies are not choosing between maintaining the status quo and change; they are choosing between two distinct paths of change. One path, exemplified by WPP, involves trimming headcount to meet a 2028 profitability target, hoping the retainer book remains stable 7. The other path involves a fundamental delivery rebuild: shifting coordination labor into a production system, repositioning seniors for brief and approval stages, and pricing services based on measurable client outcomes.

The decision window is shorter than many P&Ls suggest. With 85% of US B2C marketing executives planning agency reviews in 2026 2, the next contract cycle will be critical for new pricing conversations. Agencies with coordination-heavy cost structures will find themselves defending against AI-augmented competitors achieving 40%+ margins on similar work 3.

The key question for operators is precise: which parts of the current delivery chain still justify their cost when clients can clearly see the true cost of deliverables? Any element that fails this scrutiny must be rebuilt or will be replaced by platforms that already offer a more efficient solution.

Frequently Asked Questions

References

- 1.Basis 2026 Advertising Agency Report: Industry Health & AI Adoption.

- 2.Forrester: Marketing Agencies Resign Their Agency - Business Model Transformation 2026.

- 3.Digital Advertising Market Outlook: Engineering-Led Firms Achieving 40%+ Margins While Traditional Agencies Compress to 2-3%.

- 4.McKinsey: Strategy's Biggest Blind Spot - Erosion of Competitive Advantage.

- 5.Why Marketing Agencies Are Struggling in 2025 - Entrepreneur Analysis.

- 6.Rethinking Agency Retainers: The Move Toward Performance-Based Fees.

- 7.ADWEEK Agencies Advantage: AI Is Upending Agency Business Models - February 2026 Report.

- 8.eMarketer: AI is Taking Entry-Level Ad Jobs—Except for Those Fluent in Tech.

- 9.Promethean Research: Digital Agency Industry Report - Market Fragmentation & Consolidation Dynamics.

- 10.Agency Marketing M&A 2026: Consolidation, AI & Exit Opportunities - PE-Backed Platform Activity.

- 11.The State of AI: Global Survey 2025 - McKinsey.