Key Takeaways

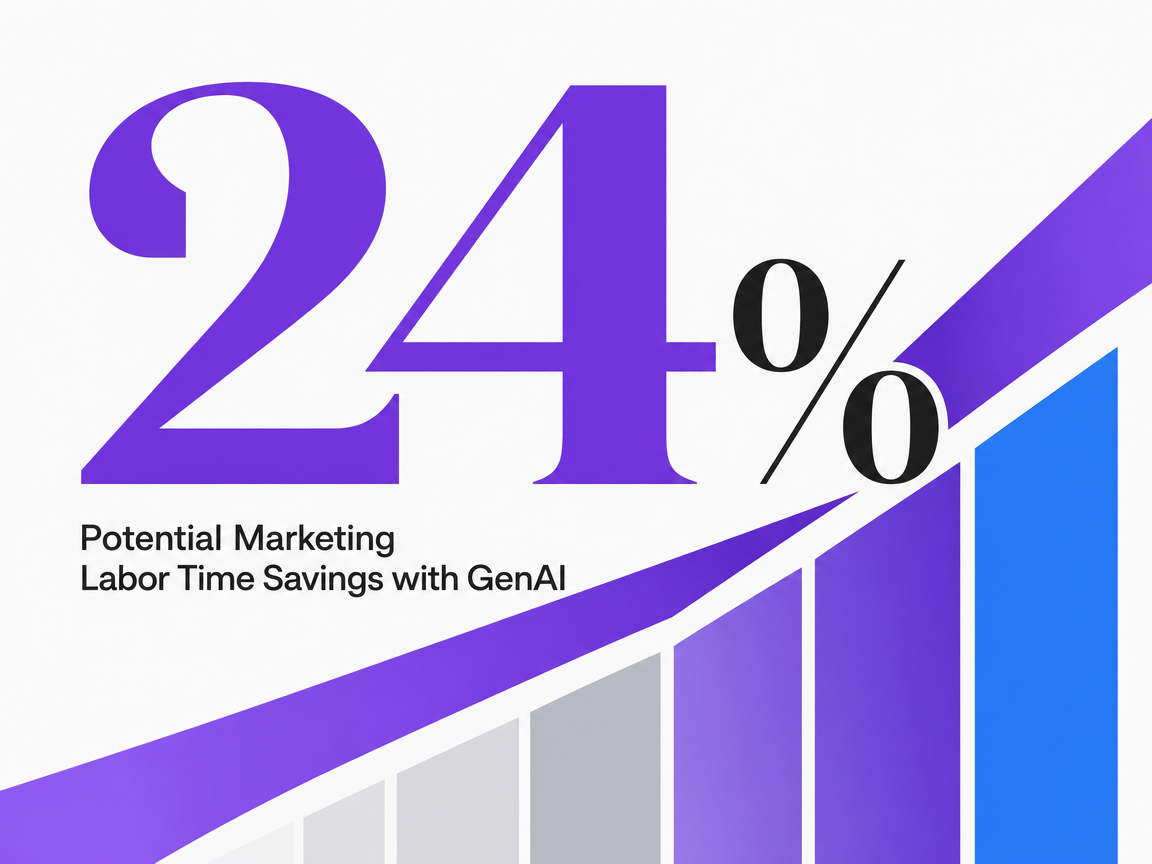

- The labor-hour retainer is what's collapsing, not the retainer itself; Bain estimates generative AI can reclaim 24% of marketing labor time, giving clients arithmetic to justify fee cuts 6.

- Horizontal consolidation and vertical integration are different games—owning the production stack, data, and measurement layer changes the cost of delivering an hour, while roll-ups only chase scale 5.

- Margin survives when agencies tightly integrate data, workflow, measurement, and production QA but keep strategy, creative direction, and client judgment modular and human-led 5.

- Reprice retainers around outcomes the agency defines and tracks, using shorter contract terms so productivity gains land in agency margin rather than becoming automatic client discounts 8.

The Labor-Hour Retainer Is What's Actually Dying

Retainers aren't collapsing; the billable-hour model underpinning them is. When a client agrees to a fixed scope for $15,000 a month, that figure was historically tied to the labor hours an agency needed. Generative AI has fundamentally altered this equation. Bain estimates that companies could reclaim 24% of marketing labor time using generative AI, translating to roughly a 30% productivity gain across the function 6. Clients are aware of these figures and are beginning to factor them into their pricing expectations.

The strategic shift occurring beneath headlines about in-housing and consolidation is vertical integration. Both brands and agencies are bringing production, data, and workflow into a single stack, rather than purchasing these services by the hour. For agency owners, the critical question isn't whether to defend the retainer, but whether that retainer is built upon a production stack the agency truly owns, or on borrowed labor that clients can now replicate with a subscription and a prompt.

In-Housing Isn't a Threat — It's a Signal About Where Margin Went

What the ANA Numbers Actually Say (and Who They Don't Represent)

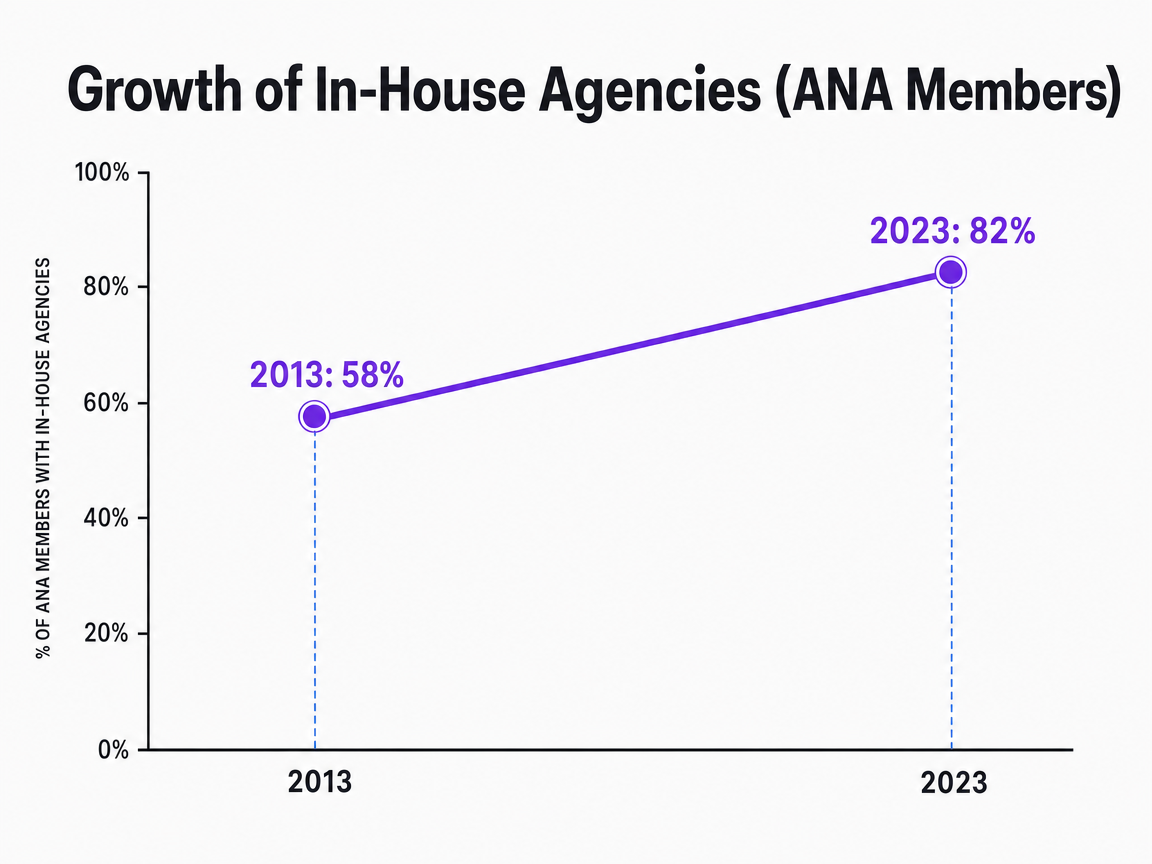

The frequently cited statistic states that 82% of ANA members now operate an in-house agency, a significant increase from 58% a decade prior 1. While this figure often fuels narratives about the decline of agencies, it's crucial to consider its context, especially for agencies managing $10,000–$50,000 monthly retainers.

ANA membership primarily consists of large brand advertisers—organizations with the financial capacity to establish dedicated internal teams and the media volume to justify such investments. Therefore, the 82% figure reflects trends at the enterprise level, where in-housing has been a growing practice long before generative AI became prevalent. It does not accurately represent the mid-market.

A more telling trend is the deceleration of this growth. The ANA's 2023 report shows internal agency adoption at 82%, a modest increase from 78% in 2018 2. This four-point rise over five years contrasts sharply with the 20-point jump observed between 2013 and 2018. This suggests that the trend is approaching saturation among brands most equipped to insource, rather than indicating a widespread stampede.

For mid-market agency owners, the takeaway is more nuanced: large-brand insourcing is a gradual, established trend, not a sudden shift. The pressure on $15,000-a-month retainers isn't coming from the ANA cohort, as these clients were rarely on their rosters. Instead, it stems from mid-market clients observing enterprise brands and questioning why their agencies cannot deliver comparable efficiency.

Growth of In-House Agencies (ANA Members)

Growth of In-House Agencies (ANA Members)

Percentage of ANA members with in-house agencies grew from 58% in 2013 to 82% in 2023.

The Vertical Proof Point: When In-House Teams Double in a Year

This section examines a specific service vertical to illustrate the impact of in-housing, as the real estate example closely mirrors the multi-location, franchise-style clients often served by mid-market agencies.

Between 2022 and 2023, the average size of in-house marketing teams at real estate firms nearly doubled, according to industry research on brokerages and franchise operators 3. This represents a rapid, significant change within a single fiscal year, in a sector characterized by fragmented local execution alongside national brand campaigns.

The real estate industry offers valuable insights because its client base—multi-location operators, franchisees, affiliated service businesses, and complex local-plus-national mandates—resembles that of many mid-market agencies. When these firms double their internal marketing headcount in twelve months, the work must originate from somewhere. While some of this is genuinely new capacity, a substantial portion comprises work that previously fell under agency retainers.

The implication is not that mid-market clients will fully insource, but that categories of work most susceptible to internal absorption—such as production, campaign trafficking, and localized content—are precisely those that historically contributed to retainer hours. When these hours shift in-house, the remaining components of the retainer must justify their value on a different basis.

Where the Retainer Dollars Are Actually Migrating

Marketing technology now constitutes 19.9% of marketing budgets and is projected to reach 30.9% within five years, according to CMO Survey data 10. This significant shift in spending is not occurring in a vacuum; it is often reallocated from the same budget lines that previously funded external execution.

This migration can be understood as a substitution effect. Funds once allocated to agency labor hours—for production, media trafficking, reporting, and iteration—are now being directed towards platforms that promise to perform these tasks with reduced human overhead. The CMO Survey also highlights a critical challenge: many marketers struggle to translate martech spend into tangible performance gains 10. This indicates that budget allocation is outpacing the development of effective operating models.

For agency owners, the implication is clear: the retainer is not solely losing ground to in-house teams. It is also competing with a category of spend that barely existed a decade ago. To reclaim these dollars, agencies must position themselves against platforms, not just internal hires. This necessitates that the production stack supporting the retainer increasingly resembles software, rather than a timesheet.

Test full vertical integration workflows in real time

Validate integrated delivery speed and oversight by publishing live campaigns during your no-risk trial period.

Horizontal Consolidation vs. Vertical Integration: Stop Conflating Them

Industry publications often categorize all major agency news under the umbrella of "consolidation." This typically refers to horizontal consolidation, where holding companies acquire others, networks absorb independents, or clients reduce their agency rosters. This strategy involves combining similar businesses at the same level of the value chain to achieve scale, enhance pricing power, and expand cross-selling opportunities.

Vertical integration, however, is a distinct strategy. It involves the decision to own more of the underlying stack required for the work: data infrastructure, production tools, measurement frameworks, and publishing workflows. Bain articulates the CMO's role in these terms—determining what to integrate tightly (measurement, data, workflow) and what to keep modular (creative, brand voice) 5. This decision is about where value is created, not merely the size of an agency roster.

Conflating these two strategies is problematic because they yield opposing outcomes for mid-market agencies. A network roll-up aims to gain market share and negotiate better media rates. In contrast, a vertically integrated agency fundamentally alters the cost of delivering a retainer hour. One is a balance-sheet maneuver; the other is a margin-driven strategy.

For agency owners lacking the capital for consolidation, this distinction presents an opportunity. Owning the production stack—the AI-driven layer that transforms a brief into delivered work—is accessible through subscriptions, not private-equity investments. The advantage here is not headcount, but throughput per human hour.

The Retainer Math After Clients Price in AI Productivity

The 24% Question: What Bain's Number Does to a P&L

Bain's estimate that generative AI could reclaim 24% of marketing labor time, leading to a roughly 30% productivity gain, is central to the current agency-pricing debate 6. The difference between these two figures—labor time reduction versus output gain—is where the entire retainer conversation now resides.

Clients will likely reference the 24% labor-time figure during renewal discussions. Agency owners, however, should focus on the 30% productivity gain when evaluating their profit and loss. These are not interchangeable arguments. A direct 24% reduction in hours, if passed on as a discount, impacts the top line. Conversely, a 30% gain in output, if captured by the agency, boosts the margin line—but only if the agency controls the production stack underlying the retainer.

Bain's framework is significant because it positions AI as a catalyst, not the sole cause, of these pressures. Retainer pricing was already strained by in-housing, martech substitution, and shorter CMO tenures. Generative AI now provides clients with a quantifiable basis for these pressures. Previously, a client requesting a 15% discount had to argue about value; now, they can cite arithmetic, backed by a Bain estimate.

For agency owners, addressing the 24% figure is not optional. Clients are aware of the same Bain insights. Ignoring this number in renewal conversations means allowing the client to dictate the terms of its application.

Potential Marketing Labor Time Savings with GenAI

Potential Marketing Labor Time Savings with GenAI

Potential Marketing Labor Time Savings with GenAI

Three Retainer Scenarios, One Margin Line

To illustrate the impact of Bain's numbers on a retainer's P&L, consider a single engagement across three scenarios. The following table uses an illustrative $15,000 monthly retainer with a 40% starting margin, representing a plausible mid-market benchmark. The only research-derived variable is Bain's estimate of a 24% reduction in marketing labor time via generative AI, associated with a roughly 30% productivity gain 6.

| Scenario | Monthly Fee | Labor Cost | Margin $ | Margin % |

|---|---|---|---|---|

| 1. Traditional labor-hour retainer | $15,000 | $9,000 | $6,000 | 40% |

| 2. Client demands 24% pass-through discount | $11,400 | $9,000 | $2,400 | 21% |

| 3. Vertically integrated production, agency captures gain | $15,000 | $6,300 | $8,700 | 58% |

Scenario one represents the pre-AI baseline. Scenario two demonstrates the outcome if the client applies Bain's 24% labor-time figure directly to the fee, and the agency has no corresponding cost reduction—margin drops from 40% to 21% for the same scope. Scenario three assumes the agency has reconfigured its production processes so that the 24% labor reduction benefits its own cost structure rather than being passed to the client. In this case, margin expands to 58% on an unchanged fee.

The disparity between scenarios two and three underscores the importance of owning the production stack. Both scenarios assume the same underlying AI productivity gain; the only variable is which party captures it. In a labor-hour retainer, the client can reasonably claim savings because they are paying for labor. In an outcome-priced retainer built on an integrated production layer, the input cost becomes the agency's responsibility and benefit.

Bain also highlights the inherent tension: brands expect efficiency gains to translate into lower fees, while agencies must protect their margins. This tension is already evident in remuneration discussions 6. This negotiation will occur regardless of an agency's preparedness. Scenario three illustrates how an agency can proactively address this by having its financial model in order.

Why 91% Adoption Means AI Alone Won't Save the Retainer

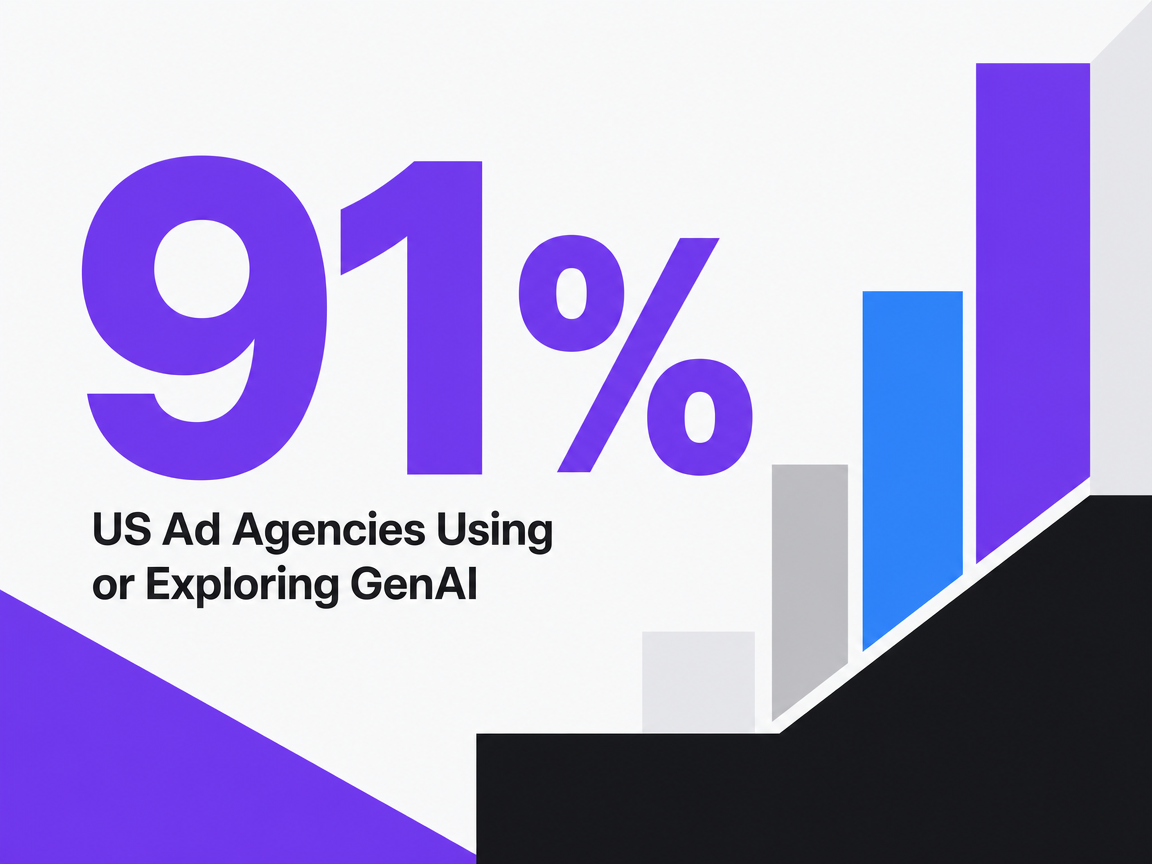

Forrester's 2025 outlook for U.S. marketing agencies indicates that generative AI adoption stands at 91%, either in active use or under exploration 7. This figure represents the baseline of the current market, not a competitive advantage. With nine out of ten agencies using or piloting the same tools, "we use AI" becomes a statement of market average, not differentiation.

The strategic implication is challenging. If an agency's unique selling proposition in 2025 is simply "we use AI," it describes a common practice, not a competitive edge. The productivity gains quantified by Bain are accessible to every competitor and to clients' internal teams if they choose to build them 6. Therefore, mere adoption commoditizes rather than protects.

What truly distinguishes agencies within this 91% is not just their use of generative AI, but how deeply these tools are integrated into their data, measurement, and workflow—the layers Bain identifies as crucial for tight integration 5. An agency that treats AI as an add-on to a labor-hour workflow will capture only a fraction of the potential gains and remain vulnerable on pricing. Conversely, an agency that embeds AI as the foundation of its production can capture the full productivity delta and defend its retainer based on output, rather than hours.

The retainer that endures is one where AI is seamlessly integrated and load-bearing to the operation, making its presence invisible to the client.

See How Vertical Integration Reduces Overhead and Increases Efficiency

Request a data-driven analysis of your current delivery model and explore how AI-powered vertical integration can streamline multi-channel execution while preserving margin and control.

The Agency-Side Integration Play: What to Own, What to Keep Modular

Integrate Tightly: Data, Measurement, Workflow, Production QA

Bain's perspective is clear: measurement, data, and workflow should be tightly integrated within an agency's operations, while creative excellence and brand voice should remain distinct 5. This distinction provides a blueprint for agency-side vertical integration.

Data is the foundational layer to integrate. An agency that doesn't control the flow of client performance signals—such as call logs, form fills, media spend, and conversion attribution—is essentially renting the raw material for its own recommendations. When these data streams reside within a client's system or a third-party dashboard outside the agency's control, every reporting cycle involves a handoff, which translates into billable labor hours that are now targets for discounts.

Measurement follows a similar logic. If the criteria for a qualified lead, a booked appointment, or pipeline-influenced revenue are embedded within the agency's system, rather than being renegotiated quarterly, the retainer shifts from billing for effort to billing for a defined outcome. This reframe is only credible when the agency controls how that outcome is measured.

Workflow and production quality assurance (QA) are where the traditional labor-hour model truly breaks down. A brief that moves from strategist to writer, editor, trafficker, and then to a reporting analyst—involving multiple handoffs, queues, and potential points of quality degradation—is precisely the process targeted by Bain's 24% labor reduction figure 6. Consolidating these handoffs into a single, governed loop, with AI handling the production load and humans providing approvals at specific checkpoints, transforms productivity gains into agency margin rather than client discounts.

Keep Modular: Strategy, Creative Direction, Client Judgment

The error in the opposite direction is over-integration. Bain explicitly states that creative excellence and brand voice should remain separate from the tightly integrated operational core 5. Agencies that attempt to systematize judgment often end up systematizing mediocrity.

Strategy remains modular because it relies on contextual factors that platforms cannot discern. Whether it's a regulated behavioral health client preparing for payer negotiations, a home services operator repositioning with a new service line, or a DSO integrating an acquired practice—these decisions are not improved by faster workflows. They are enhanced by senior human expertise that can analyze and interpret complex situations.

Creative direction falls into the same category. AI production can generate hundreds of headline variations rapidly. However, selecting which variant aligns with the brand—and which ones could actively harm it—requires a judgment call that clients are still willing to pay a premium for. Forrester's finding that 91% of U.S. agencies are using or exploring generative AI 7 underscores why the human element above the AI must remain sharp: if everyone has similar generation capabilities, differentiation shifts upstream to taste, positioning, and strategic direction.

Client judgment—the relationship layer—is the final modular component. It is also frequently mistaken for something that can be automated, which it cannot. This human connection is what a retainer truly purchases once production is no longer the primary justification for the invoice.

US Ad Agencies Using or Exploring GenAI

US Ad Agencies Using or Exploring GenAI

US Ad Agencies Using or Exploring GenAI

Repricing the Retainer Around Outcomes, Not Hours

A labor-hour retainer prices the input, whereas an outcome retainer prices the result. This fundamental distinction determines who benefits from productivity gains when AI is introduced into the workflow, and it is a contractual shift consistently highlighted in current pricing literature.

The pricing dilemma is now well-established: as generative AI productivity gains become widely known, advertisers are pressuring agencies to reduce fees and retainers, expecting efficiency savings to be passed on to them 8. This pressure is only logical within a labor-hour contract. If a retainer is defined by hours delivered, a client can reasonably question why the cost per hour remains the same when tools have improved efficiency. However, if the retainer is defined by specific outcomes—such as qualified leads generated, pipeline influenced, or content published against measurable performance targets—the discussion shifts away from labor hours.

Repricing around outcomes requires three sequential actions from an agency:

- Define the outcome using metrics the agency can control and measure—e.g., booked appointments, maintained keyword rankings, or cost per qualified lead—rather than relying on metrics defined by the client's finance team each quarter.

- Price the outcome based on AI-driven production costs, not traditional billable-hour costs.

- Structure contracts with short enough terms to allow for recalibration as the productivity delta evolves.

Bain clearly articulates the underlying tension: brands expect efficiency gains to be reflected in lower fees, while agencies need to maintain margins. The resolution lies in redesigning remuneration models, rather than simply negotiating discounts 6. Agencies that proactively implement this redesign will establish new reference prices, while those that delay risk being repriced by clients who are informed by the same public research.

Benchmark Your Agency’s Efficiency Against AI-Driven Vertical Integration

Gain access to a unified platform that replaces manual production cycles with data-backed, approval-first automation—eliminating up to 60% of delivery overhead while maintaining full control and measurable outcomes across every channel.

The Counter-Case: Why Agencies Aren't Fading

The most compelling argument against the "death of the retainer" thesis comes from the client's perspective. CMO tenures are shortening, performance expectations are tightening to 12–18 month windows, and the pressure to demonstrate measurable impact quickly is driving marketing leaders to seek more agency support, not less 4. MediaPost's commentary is direct: agencies are becoming more essential, not fading 4.

This appears contradictory only if the retainer is defined by hours. When viewed through the lens of an outcome-priced, vertically integrated model, it becomes a significant advantage. A CMO operating on an eighteen-month timeline cannot afford to build an internal team from scratch, hire senior specialists, and wait for institutional knowledge to develop. What that CMO can afford is an external partner who provides a pre-built production stack, an integrated measurement layer, and the strategic capacity to oversee the workflow.

The agencies that are struggling are those that rent labor to clients who can now acquire it more cheaply elsewhere. Conversely, the agencies that are becoming indispensable are those offering access to a production system that clients cannot easily replicate.

A Decision Framework for the Next Twelve Months

For a mid-market agency owner, the next twelve months require a series of operational decisions that will determine whether their retainer book grows or shrinks, rather than a simple rebrand.

The work should be sequenced into three phases:

- In the first quarter, audit which retainer hours can already be replicated by generative tools—such as production drafts, initial reporting, media trafficking, and QA cycles. These are the hours clients will likely target for repricing first 6. Transition these tasks to an integrated production layer controlled by the agency, rather than relying on per-seat licenses that clients can also purchase.

- From months four to eight, integrate data and measurement internally. Take ownership of defining key metrics like qualified leads, booked appointments, and pipeline revenue. Bain explicitly states that data, measurement, and workflow are the layers that warrant tight integration 5. Without this ownership, an outcome-priced retainer lacks a defensible basis.

- In the final third of the year, revise contracts. Price services based on measurable outcomes that the agency tracks, using terms short enough to allow for recalibration as productivity gains expand 8. Maintain strategy, creative direction, and client judgment as human-centric functions—these are the true value propositions of the retainer now. Platforms like Vectoron are designed to handle the production and measurement load beneath this human layer.

Frequently Asked Questions

References

- 1.ANA: In-house agency trend continues to gain steam.

- 2.ANA Report: 82% Of Marketers Have In-House Agencies.

- 3.Exploring the Shift Toward In-House Marketing Teams.

- 4.Forget the In-Housing Debate: Why CMOs Still Need Agencies to Win.

- 5.What Agency Consolidation Means for CMOs.

- 6.Marketers' Agency Partnerships Are Strained. Now Comes AI.

- 7.The State Of Generative AI Inside US Marketing Agencies, 2025.

- 8.GenAI and the Pricing Dilemma: How Advertising Agencies Can Adapt.

- 9.Service Marketing in Online Shopping Platform: Psychological and Behavioral Aspects.

- 10.The CMO Survey: Marketers Spend on New Technologies as They Battle Usage and Impact.

- 11.2026 CMO Survey | Deloitte US.