Key Takeaways

- The platform decision is really an operating model decision: which retainers, dashboards, and approval loops to retire so coordination cost stops capping pipeline output.

- A unified platform must clear Forrester's seven-capability floor—segmentation, automated programs, scoring, routing, reporting, data updates, and bidirectional sales integration—inside one data model 7.

- Multi-location operators should model consolidation in cost per qualified booking, since unified data lifts location-level conversion in ways cost-per-lead math hides 5.

- Evaluate AI features as a governance question: recommendations should carry visible rationale and route to a named approver before anything ships, not execute autonomously 3.

The Operating Model Question Behind Every Platform Decision

Most marketing automation evaluations start with the wrong question. VPs comparing vendors tend to ask which tool has the best email builder, the cleanest scoring model, or the deepest CRM sync. The harder question—the one that actually shapes pipeline outcomes—is whether the platform replaces an operating model or merely sits on top of one.

That distinction matters because the category has moved. Forrester's Q3 2024 evaluation of B2B revenue marketing platforms scored 12 providers across 23 criteria covering data management, orchestration, analytics, and partner ecosystems—a scope that now spans email, web, events, ABM, and sales enablement inside a single system 3. The tooling has converged. The way most marketing teams work has not.

Inside a typical growth-stage company or multi-location service group, execution still flows through a familiar pattern: an agency owns paid, a freelancer or junior owns SEO content, a separate vendor handles call tracking, social lives on its own calendar, and the automation tool nurtures whatever leaks through. Each handoff costs time, and each tool reports against its own definition of success.

Deloitte's CMO Survey, now in its 35th edition, captures the pressure that makes this stack untenable—rising AI investment, C-suite demands to prove value, and a push for disciplined experimentation rather than parallel spend 1. The platform decision is really a decision about what to stop doing: which retainers to retire, which dashboards to consolidate, and which approval loops to collapse into one. Everything that follows in this article works backward from that frame.

From Email Engine to Revenue Orchestration Layer

The label "marketing automation" still carries its 2010-era weight: drip campaigns, lead scoring, a CRM sync, maybe a landing page builder. That definition no longer matches what analysts evaluate or what buyers expect. The category has absorbed adjacent functions until the platform itself sits at the center of revenue execution rather than at the edge of it.

Forrester's Q3 2024 Wave on B2B Revenue Marketing Platforms makes the shift explicit. The evaluation scored 12 providers against 23 criteria covering data management, orchestration, analytics, execution, and partner ecosystems—spanning email, web, events, ABM, and sales enablement inside one rated system 3. That criteria set is the clearest signal that the unit of analysis has moved from "automation tool" to "orchestration layer." Email is one column in a much wider grid.

The convergence has a direction. Marketing automation, account-based marketing, journey analytics, and revenue execution tools are folding into single platforms because buyers were already trying to stitch them together with integrations, spreadsheets, and agency labor 9. Each integration was a tax on speed. Each handoff blurred attribution. Pulling the work inside one data model removes both costs at once.

What this means for a VP running a lean team is concrete. The platform decision now covers questions that used to live in five separate RFPs: how customer data is modeled across channels, how journeys are orchestrated in real time, how scoring and routing connect to a sales motion, how performance is measured against pipeline rather than opens, and how AI recommendations are surfaced inside execution workflows. Forrester's analysis notes that vendors are racing to add predictive scoring, journey analytics, and AI-powered recommendations as the new competitive frontier 3.

Treating the category as an email engine misreads the market. The platforms worth evaluating are the ones built to orchestrate revenue, not the ones that orchestrate sends. That reframing changes which capabilities matter, which budgets get consolidated, and which agency relationships stop earning their retainer.

What 'Unified' Means at the Capability Floor

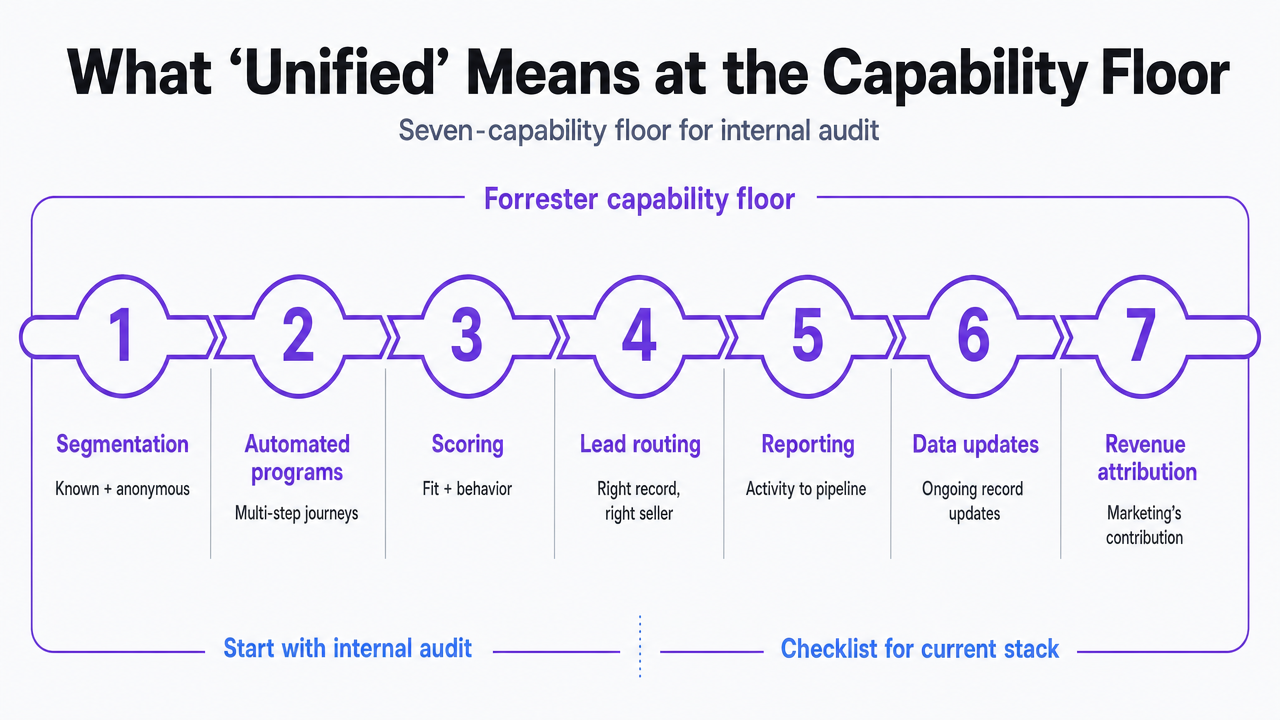

Before any vendor conversation, the word "unified" needs a definition that survives a procurement review. Forrester's working definition of a marketing automation platform is the system that seeds, creates, nurtures, and accelerates demand—and the analyst firm sets a specific capability floor any platform must clear to qualify 7. That floor is the right place to start an internal audit, because it converts a fuzzy strategy claim into a checklist a VP can run against the current stack on a Friday afternoon.

The minimum requirements cover seven capabilities:

- Segmentation across known and anonymous contacts

- Automated programs that execute multi-step journeys

- Scoring that ranks fit and behavior

- Lead routing that hands the right record to the right seller

- Reporting that ties activity to pipeline

- Ongoing data updates that keep records usable

- Bidirectional integration with sales force automation systems 7

Each capability is a join point. Lose one, and the unified story collapses back into the stack of point tools the platform was supposed to replace.

Two of those seven deserve closer reading. Bidirectional SFA integration is the difference between marketing reporting on its own activity and marketing reporting on revenue—without it, scoring and routing become marketing-internal exercises that sales ignores. Continuous data updates are the difference between a segmentation that reflects last quarter and one that reflects last week; stale data quietly degrades every downstream decision, from bid strategy to nurture sequencing.

The practical test is whether each of the seven capabilities operates inside one data model or is glued together by middleware, spreadsheets, and an agency project manager. If segmentation lives in the email tool, scoring lives in the CRM, routing lives in a separate operations workflow, and reporting lives in a BI dashboard pieced together monthly, the team has the surface area of marketing automation without the capability floor. The audit takes an hour. The results usually reframe the rest of the platform conversation.

This is also where AI-driven features should be evaluated. Predictive scoring, journey analytics, and AI-powered recommendations only compound when they sit on top of unified segmentation, clean data, and a routing layer the sales team trusts 3. Bolted onto a fragmented stack, the same features produce confident-looking outputs from inputs nobody can defend in a pipeline review.

Visualize Forrester's seven-capability floor that the section explicitly enumerates, giving readers a scannable framework reference

Visualize Forrester's seven-capability floor that the section explicitly enumerates, giving readers a scannable framework reference

Experience unified marketing execution risk-free today

Test-drive streamlined, data-driven marketing workflows and publish live campaigns with zero commitment.

The Hidden Cost of the Agency-Plus-Point-Tools Stack

The line item most marketing budgets underestimate is coordination. Software licenses appear on the SaaS spreadsheet. Agency retainers appear on the services line. The hours spent reconciling them—briefing two vendors on the same launch, rebuilding the same audience in three tools, chasing attribution across four dashboards—appear nowhere, even though they consume the team's capacity to ship anything new.

McKinsey's work on personalization is blunt about the failure mode. Many organizations invest in tools but never reorganize processes and governance, which caps the value of personalization and automation regardless of how advanced the platforms are 5. The cost shows up as flat conversion rates while licensing grows, and as senior marketers spending more time managing handoffs than designing programs.

The fragmentation has a customer-facing tax too. McKinsey's omnichannel research notes that buyers now expect to move between channels without repeating themselves, and that siloed data and channels make consistency structurally hard to deliver 4. A prospect who downloads a guide, books a tour, and then receives a generic nurture email is reading the org chart, not the brand. Each disconnected touch raises acquisition cost without anyone billing for it.

Inside the team, the math compounds in three places. Briefing cycles—the time between a strategy decision and a live campaign—stretch because each vendor needs context the others already have. Reporting drifts because each tool counts a lead differently, so the weekly pipeline number arrives with footnotes instead of conviction. And institutional knowledge leaves with whichever agency loses the next bake-off, because the playbooks live in their decks rather than in the platform.

Forrester's convergence analysis frames the alternative directly: integrated platforms that manage data, orchestration, analytics, and execution promise greater efficiency than maintaining separate point solutions, precisely because the coordination work moves inside one system instead of across many 9. The savings are not only in licenses retired or retainers cut. They sit in the hours a VP gets back when one approval, one audience definition, and one performance view replace the weekly reconciliation tax. That recovered capacity is what makes pipeline goals achievable without hiring against them.

Customer Journey as the Unifier of Marketing and Sales

Marketing-sales alignment is rarely a personality problem. It is a data problem dressed up as a meeting problem. Forrester's analysis of the long-running alignment debate lands on a simple corrective: the unifying object is the customer and their journey, not the org chart that sits behind it 10. When both teams work from the same view of how a prospect moves from first touch to closed booking, the weekly arguments about lead quality lose their fuel.

Harvard Business School research on customer journey data makes the same point from the analytical side. Integrating data across the journey—rather than reading each channel in isolation—gives managers a better read on customer needs and supports more effective personalization of retargeting, content sequencing, and offer design 2. Channel-by-channel analytics produce channel-by-channel decisions. Journey-level integration produces decisions a sales team can actually use on a call.

For a multi-location behavioral health group, the difference is concrete. A prospect researches a level-of-care question through organic search, clicks a paid ad two days later, requests a callback through a location page, and finally books an assessment after a nurture email. Five touches, five systems, one person. Without journey-level data sitting inside the platform, the intake team sees only the call. Marketing claims credit for the form. Paid claims credit for the click. The prospect's actual decision pattern—the sequence that would tell the team what to send the next thousand prospects—dissolves into attribution arguments.

McKinsey's omnichannel work frames the customer-side cost of that fragmentation: buyers expect to move between channels without repeating themselves, and siloed data makes consistency structurally hard to deliver 4. A unified platform changes what "alignment" means in practice. Shared journey data replaces shared opinions. Scoring reflects behavior across channels rather than activity inside one tool. Routing hands sales a record with context attached, not a name and a source code. The meeting still happens. It just has less to argue about.

Migration Risk and the Stakes of Platform Selection

Platform selection is a multi-year decision dressed up as a quarterly procurement event. Forrester's migration guidance puts a number on the churn: roughly 10% of B2B organizations running a marketing automation platform switch to a new one each year, with phased rollouts and explicit risk planning recommended to keep campaigns and data flowing during the transition 8. That rate sounds modest until it compounds. Across a five-year horizon, it implies that nearly half the market is in motion—either reselecting, mid-migration, or running parallel systems while the cutover stretches past its original deadline.

Two risk factors carry most of the weight in those projects:

- Team bandwidth. Migrations rarely fail on the technical merits; they stall when the same people running the current quarter's pipeline are asked to rebuild segments, scoring models, and integration logic in a second system on nights and weekends 8.

- Capability gap. A new platform that lacks a specific scoring behavior, routing rule, or reporting view the team relied on quietly forces workarounds that recreate the fragmentation the move was supposed to end.

The strategic read is straightforward. Picking a unified platform is not a feature comparison; it is a bet on which vendor's data model, roadmap, and integration surface a team can still defend three years from now. Cheap to enter, expensive to leave. The selection criteria that matter most are the ones that determine whether the next migration becomes a renewal conversation instead of a project—data portability, native channel coverage, and a capability floor wide enough that the next adjacent need shows up as a configuration, not a second vendor.

See Unified Multi-Channel Execution in Action—No Extra Headcount Required

Request a tailored walkthrough showing how enterprise teams use AI-powered marketing automation platforms to centralize approvals, accelerate output, and gain full cross-channel visibility—without expanding internal resources or juggling agency vendors.

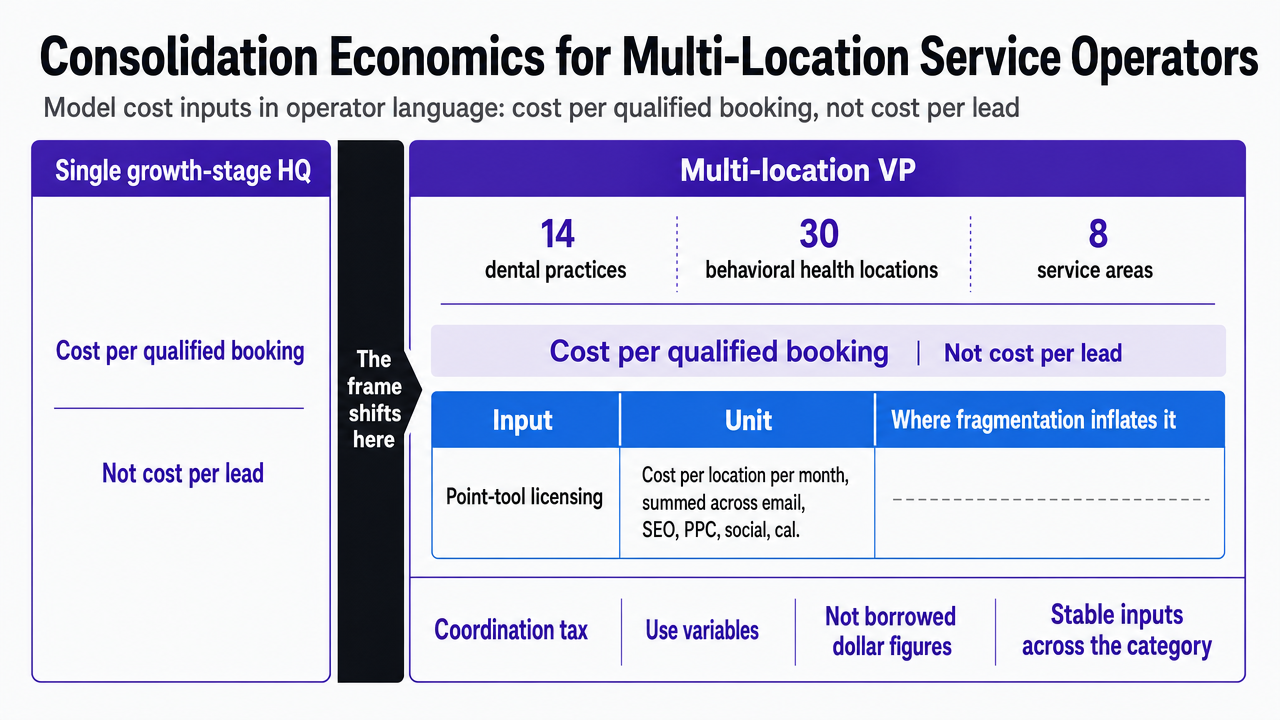

Consolidation Economics for Multi-Location Service Operators

The frame shifts here. The argument so far has addressed a VP at a single growth-stage headquarters. The math changes when the same VP runs marketing across 14 dental practices, 30 behavioral health locations, or a regional home services brand with eight service areas. Multi-location service operators carry a coordination tax the single-site case does not, and consolidation economics need to be modeled in their language: cost per qualified booking, not cost per lead.

A defensible model uses variables rather than borrowed dollar figures, because spend profiles in a 12-location DSO and a 40-location senior living group share almost no inputs. The inputs that matter are stable across the category.

| Input | Unit | Where fragmentation inflates it |

|---|---|---|

| Point-tool licensing | Cost per location per month, summed across email, SEO, PPC, social, call tracking | Per-seat or per-location pricing applied to overlapping capabilities |

| Agency retainers | Cost per channel per month | Separate retainers for paid, SEO, and social with duplicated strategy hours |

| Internal coordination | Hours per location per month spent briefing, reconciling, reporting | Briefing cycles and weekly status meetings across vendors |

| Lead-to-booking conversion | Percentage delta between unified and siloed data states | Routing, scoring, and journey context lost between systems |

| Switching cost | One-time hours and parallel licensing during migration | Phased rollouts and capability-gap workarounds 8 |

The output worth tracking is cost per qualified booking, calculated per location and rolled up. That metric absorbs the conversion-rate variable that point-tool stacks usually hide. McKinsey's personalization research is direct on the mechanism: integrating systems for shared data and a unified view of customer behavior produces measurable revenue lifts, while organizations that buy tools without redesigning processes cap their own returns 5. A unified platform that lifts location-level conversion from booking inquiry to scheduled appointment by even a few points changes the denominator on every paid dollar already in market.

Two variables get underweighted in most internal models. The first is coordination hours. A 20-location operator running four agency relationships and six SaaS tools spends real headcount on briefing and reconciliation that never appears in any vendor's invoice. The second is the migration variable. Forrester's guidance flags that roughly 10% of B2B organizations switch marketing automation platforms each year, and the projects that stall usually stall on team bandwidth rather than technology fit 8. A consolidation model that ignores switching cost overstates year-one savings; one that overweights it never moves.

The honest read for a multi-location VP is that the platform decision is a portfolio decision. The unit of analysis is the location-month, not the campaign. Consolidation pays back when one audience definition, one approval, and one performance view replace per-location reconciliation across vendors—and when the cost-per-qualified-booking number can be defended in the same operating review that owns clinical capacity, technician utilization, or chair time.

Render the article's own cost-input table as a clean visual framework so multi-location VPs can use it as a model reference. Mirrors the table verbatim and supports the section's operating-economics argument

Render the article's own cost-input table as a clean visual framework so multi-location VPs can use it as a model reference. Mirrors the table verbatim and supports the section's operating-economics argument

Approval-First AI Execution: The Next Differentiator

The capability arms race inside revenue marketing platforms has shifted from execution to recommendation. Forrester's Q3 2024 evaluation flagged predictive scoring, journey analytics, and AI-powered recommendations as the new competitive frontier for the category 3. Every serious vendor is racing to add them. The question for a VP is not whether the platform has AI features, but where the human sits in the loop those features create.

Two operating models are emerging:

- AI as an executor: the platform observes signals, decides what to send, and ships against a quota of touches.

- AI as a strategist that surfaces ranked recommendations—next best audience, next best offer, next best channel reallocation—and waits for a human approval before anything ships.

The difference looks subtle in a demo. It is decisive in a regulated vertical.

For legal intake, behavioral health admissions, or DSO marketing teams operating under HIPAA-adjacent constraints, autonomous send decisions are a liability surface. McKinsey's personalization research is clear that tools without process and governance redesign cap their own returns; the same logic compounds when AI sits inside that gap 5. An approval workflow is the governance layer that lets the AI features actually run, because every recommendation carries a reviewable rationale and a documented sign-off.

The practical test during evaluation is whether the platform can show the reasoning behind each recommendation, route it to the right approver, and execute the approved version across channels from one record. Platforms that pass that test convert AI from a marketing-confidence story into a defensible operating model. The ones that fail it produce volume the team cannot stand behind in a pipeline review.

What VPs Should Decide Next

The decision in front of most VPs is not which marketing automation platform to buy. It is which operating model to retire. The stack of point tools, agency retainers, and reconciliation meetings that produced last year's pipeline has a ceiling, and that ceiling is set by coordination cost rather than channel performance.

Three moves separate teams that consolidate well from teams that stall mid-migration:

- Run the seven-capability audit against the current stack before any vendor demo—segmentation, automated programs, scoring, routing, reporting, data updates, and bidirectional sales integration 7.

- Rebuild the budget around cost per qualified booking, not cost per lead, so the conversion lift from unified data shows up in the same model as the licensing savings.

- Treat AI features as a governance question rather than a feature checkbox; recommendations the team cannot approve and defend produce volume the pipeline review cannot stand behind 5.

The platforms worth selecting are the ones that let a lean team ship more without hiring against the goal. That is the lever Vectoron is built around.

Frequently Asked Questions

References

- 1.2026 CMO Survey | Deloitte US.

- 2.The Customer Journey as a Source of Information.

- 3.The Forrester Wave™: B2B Revenue Marketing Platforms, Q3 2024.

- 4.What is omnichannel marketing?.

- 5.The next frontier of personalized marketing.

- 6.The future of retail: Omnichannel shopping in 2030.

- 7.Marketing Automation Platforms: Minimum Requirements.

- 8.Marketing Automation Platform Migration: Timing.

- 9.Converging Platforms For Greater Efficiency: The Rise Of Revenue Marketing Platforms.

- 10.The Key To Marketing And Sales Alignment? The Customer.