Key Takeaways

- Agency economics are restructuring around principal media, projected at 33% of billings by 2026 2, deprioritizing the labor-intensive work healthcare operators most need.

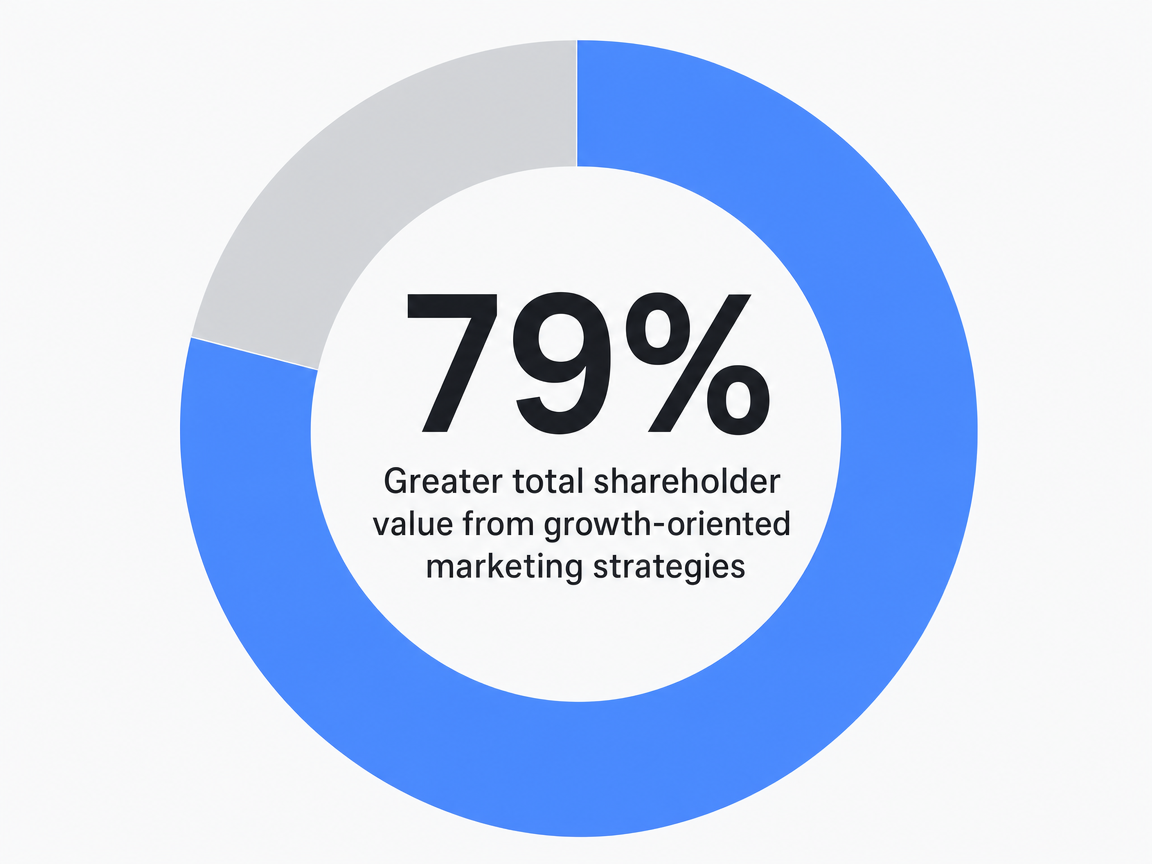

- Framing automation as a growth investment rather than cost reduction sets the ceiling, with strategic deployment delivering 2x marketing-driven profitability and 79% greater shareholder value 1.

- Governance must precede software, since fragmented ownership and unclear decision rights cause 70% of digital transformations to fail 5 regardless of platform capability.

- Most multi-location operators should hybridize before replacing, moving scaled activities onto a platform while building the decision rights and medical accuracy review workflows full replacement requires.

The agency model is repricing itself before clients walk away

Forrester expects 85% of US B2C marketing executives to put their media agencies under formal review in 2026, and agencies are proactively adapting. Headcount across the agency sector is projected to fall 15% next year, following an 8% cut in 2025 2. One global holding company CEO articulated the shift: "by 2028, double the profits and halve the people" 2.

This isn't a client-driven revolt; it's the supplier redefining its own value proposition. For healthcare VPs of Marketing managing patient acquisition across numerous locations, this reorders priorities. The question isn't whether to test marketing automation software against an incumbent retainer, but rather how to coordinate execution when the retainer model itself is being dismantled. Principal media, where agencies buy inventory with their own capital and resell it to clients, is forecast to reach 33% of total agency billings by 2026 2. The economic relationship is shifting from labor hours to inventory arbitrage, bringing brand stewardship questions to the forefront.

Healthcare operators experience this disruption differently than CPG or retail buyers. A multi-location DSO or urgent care chain needs continuous patient acquisition across service lines, geographies, and compliance constraints, not just a single campaign. As agency staffing thins and the billing model favors media markup, critical healthcare-specific tasks—such as medical accuracy review, location-level SEO, deep service-line content, and paid search hygiene per market—are often deprioritized. These are the least profitable activities for agencies restructuring around principal media 7.

This disruption is impacting agencies regardless of individual client actions. Healthcare marketing leaders are no longer initiating a transition; they are timing one. The following sections explore what this timing decision entails when patient acquisition cost, multi-location coordination, and medical accuracy are non-negotiable inputs.

Why healthcare VPs are revisiting the retainer in 2026

The primary driver for most healthcare retainer reviews in 2026 isn't dissatisfaction with creative output, but rather a fundamental math problem that the traditional agency relationship was not designed to solve.

Healthcare operations leaders identified deploying the latest technology, including AI, as a top priority for 45% of organizations in 2023, a 17 percentage point increase from two years prior 5. This trend is mirrored in marketing departments. When the operations chief is automating claims handling and scheduling, the VP of Marketing, facing board scrutiny on patient acquisition costs, can no longer justify a retainer that scales linearly with the number of locations.

Furthermore, the agency landscape is evolving. Forrester's 2026 forecast predicts agencies will consolidate, reduce staff, and shift towards solution-based pricing and principal media inventory 7. The retainer a healthcare VP signed in 2022 is fundamentally different from the services delivered in 2026, even if contract language remains unchanged. Account teams shrink, senior strategists rotate, and production moves offshore, while hourly rates often remain constant.

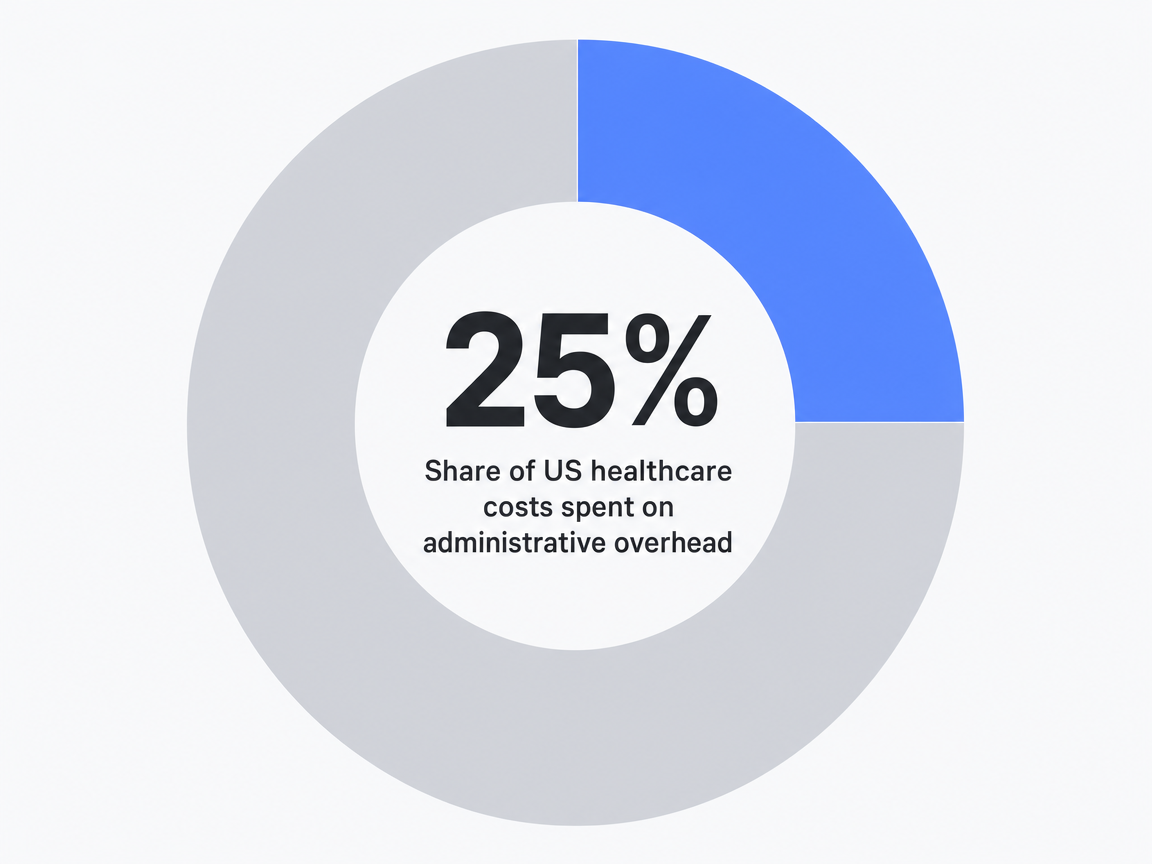

Healthcare faces an additional pressure point: clinician burnout and operational inefficiency are well-documented challenges across US health systems, and marketing teams are part of this cost-discipline conversation 6. A private equity sponsor reviewing quarterly reports does not differentiate between marketing and administrative overhead. McKinsey estimates administrative spend accounts for 25% of the $4 trillion US healthcare bill, and every component of that 25% is being evaluated for automation 5.

The retainer review is not an ideological stance; it's a strategic portfolio decision driven by adjacent automation initiatives already underway within the organization.

The principal media shift and its implications for healthcare buyers

Principal media fundamentally alters the agency's allegiance. When an agency purchases inventory with its own capital and resells it to clients, its profit margin is tied to the price difference, not to the client's patient acquisition cost. Forrester projects principal media will constitute 33% of total agency billings by 2026 2, representing a significant structural shift in agency revenue generation.

While this trade-off might be debatable for a CPG advertiser running national campaigns, it's much harder to justify for a healthcare operator managing geo-targeted paid search across 40 metro areas. Healthcare paid media is highly granular, requiring bid adjustments per service line, per location, per match type, and per device. It also involves compliance reviews for ad copy referencing conditions or treatments, and continuous negative keyword hygiene to adapt to seasonal symptom queries. None of these critical activities generate principal media margin.

Agencies prioritizing inventory arbitrage will naturally focus on activities with high media spend velocity, not those with stringent medical accuracy requirements. Forrester's analysis describes agencies moving from labor-based to outcome-based and inventory-based economics 2. Healthcare buyers must carefully interpret this. Outcome-based pricing is only effective if the outcome the agency is compensated for aligns with the operator's actual need—new patient appointments at a defensible cost, not just impressions or clicks.

PwC and ANA's work on AI in marketing highlights a similar point about perspective: strategic deployment leads to 2x or higher marketing-driven profitability, while narrow cost-cutting diminishes budgets and influence 1. The principal media shift pushes agencies towards a cost-and-margin perspective, whereas healthcare growth demands the opposite.

Multi-location operators and the hidden tax of per-location handoffs

The retainer cost on a healthcare operator's P&L often masks the true expense, which includes a significant hidden tax in coordination time.

A 25-location orthopedic group using an agency typically manages per-location intake forms, creative approvals, reporting cadences, and account manager interactions. Each handoff creates a queue, and each queue introduces a risk of missed deadlines. Marketing teams find their calendars filled with status calls that exist solely because work is fragmented across individual location engagements instead of being executed under a unified account-level plan.

McKinsey's research on healthcare service operations indicates that employees in related functions spend 20-30% of their daily work hours on nonproductive activities, largely information retrieval and coordination 5. Marketing teams managing multi-location agency relationships experience this same productivity drain. The VP isn't paying for this time on the agency invoice; they are effectively paying for it twice on internal payroll—once for coordinating with the agency, and again for rebuilding context lost between sprints.

Another aspect of this hidden cost is inconsistency. Service-line content developed for one location often doesn't transfer seamlessly to another when each engagement is scoped independently. This leads to drift in schema markup, location pages, GBP optimization, and review response workflows. Forrester's research on AI in marketing identifies fragmented ownership and unclear decision rights as structural issues that AI adoption exposes 3. Multi-location healthcare programs already have these conditions, and the retainer model perpetuates them.

Growth lens versus efficiency lens: the decision that sets the ceiling

The most critical decision a healthcare VP makes regarding marketing automation software isn't about features, but about the framing presented to the board.

PwC's research with the ANA clearly delineates the impact. Marketers who strategically deploy AI for growth, creative leverage, and patient acquisition velocity achieve 2x or higher marketing-driven profitability. Conversely, those who deploy AI narrowly for cost reduction see their budgets shrink and their influence within the enterprise diminish 4. The same software, vendors, and use cases can lead to vastly different outcomes, determined solely by how the initiative is positioned.

A CPG CMO interviewed in the PwC study articulated this perspective: "AI should be seen through a growth lens, not an efficiency lens, and the future will honor the brave who use it to create, not just optimize" 4. Another CMO in the same research highlighted AI's "biggest gift to marketing is objectivity, taking waste and bias out of the process and leaving more room for creative work" 1.

Greater total shareholder value from growth-oriented marketing strategies: 79%

Greater total shareholder value from growth-oriented marketing strategies: 79%

For healthcare VPs facing board questions, the temptation is to focus on easily quantifiable metrics like patient acquisition cost or headcount avoidance. While these are defensible and simpler to model, pitching automation solely as cost reduction often results in budget cuts that limit the technology's full potential. This approach confines the marketing function to a smaller mandate than the platform can support.

Framing automation as a growth investment is more challenging to articulate. It requires the VP to commit to a patient acquisition target rather than a savings number, and then justify the platform investment needed to achieve that target. PwC and ANA found that leading marketers adopting this growth-oriented framing deliver 79% greater total shareholder value than their peers 1. This disparity stemmed not from the technology choice itself, but from the strategic framing.

What 2x marketing-driven profitability actually requires

The "2x" profitability figure is not an inherent software outcome; it's a deployment outcome contingent on specific conditions.

First, AI must be applied to creative and strategic work, not merely to automate tasks previously handled by agencies. Replacing a copywriter with a generative AI tool offers a one-time cost saving. In contrast, building a service-line content engine that continuously generates topical authority across 40 locations creates a compounding traffic curve. The software stack might be the same, but the mandate differs significantly.

Second, measurement must align with board-level concerns. Forrester's research on CMO-led AI transformation indicates that organizations lacking clear decision rights and shared definitions of success often see pilots stall 3. For a multi-location healthcare program, this means pre-defining success metrics—such as new patient appointments per service line, cost per booked consultation, or location-level revenue contribution—and configuring the platform to report on these from the outset.

Third, the scope must be comprehensive. PwC's analysis of leading marketers shows that the profitability multiplier comes from AI deployed across the entire funnel, not confined to a single channel 4. A healthcare operator using automation only for blog content, while paid search is managed externally and SEO drifts per location, will capture only a fraction of the potential economic benefits. The 2x outcome assumes integrated execution across content, technical SEO, paid media, and conversion efforts, all driven by a single account-level plan.

Fourth, patience for the learning curve is essential. Billy Hackenson, a VP at Cisco, characterized AI success as empowering people with the right tools, education, and clarity to achieve outcomes, rather than expecting immediate returns 3. Healthcare programs that abandon automation after only four months because savings haven't materialized are giving up on an asset before it has had a chance to compound. The growth lens necessitates a longer measurement window than an efficiency-focused approach allows.

Experience Marketing Automation ROI in One Week

See measurable improvements in patient acquisition with live campaigns during your risk-free trial period.

Consolidation economics across a 25-location footprint

While the retainer fee is a visible cost, the true economics lie in how work is structured per location and the coordination overhead an operator incurs to maintain it.

A 25-location healthcare operator working with a traditional agency typically pays for the same activities twenty-five times over. Strategy is refreshed per market, content is briefed per service line per location, and paid search is managed in silos mirroring the organizational chart rather than the patient journey. Reporting arrives in twenty-five different formats, requiring internal reconciliation before any board presentation. The agency invoice covers some of this, but the operator's own marketing payroll absorbs the rest.

The table below compares typical cost categories under a per-location retainer model versus a centralized automation model. Dollar figures are variables for the operator to input from their own contracts, with sourced benchmarks cited. The goal is not to provide a total savings number, but to illustrate how line items shift when work is consolidated.

| Cost category | Traditional agency model (per location) | Centralized automation model (account level) | Source or assumption |

|---|---|---|---|

| Strategy and planning | Refreshed per location or per market; billed inside retainer | One account-level plan covering all locations and service lines | Variable: assumed retainer $X per location per month |

| Content production | Briefed and produced per service line per location; per-asset fees common | Service-line content engine running continuously across the footprint at account-level cost | PwC and ANA: strategic AI deployment delivers 2x+ marketing-driven profitability when scaled across the funnel rather than parked in one channel 4 |

| SEO execution | Per-location technical audits, schema, GBP work; consistency drifts between engagements | Single technical baseline applied to every location; location pages templated and version-controlled | Forrester: fragmented ownership and unclear decision rights are the conditions AI exposes; consolidation is the precondition for outcome 3 |

| Paid media management | Hourly or percent-of-spend management; principal media markup increasingly embedded | Bid management and negative keyword hygiene executed against one account-level taxonomy | Forrester: principal media projected at 33% of agency billings by 2026 2 |

| Reporting and analytics | Per-location dashboards reconciled manually into board view | Account-level reporting at the service line and location grain from a single data layer | McKinsey: employees spend 20-30% of work hours on nonproductive activity, much of it information retrieval 5 |

| Account management overhead | Account managers, status calls, and approval queues per engagement | Single approval workflow; no per-location account team layer | Variable: assumed internal coordination hours $Y per location per month |

| Administrative drag | Embedded in both agency invoices and internal payroll | Compressed to the approval and review layer only | McKinsey: administrative spend equals 25% of the $4T US healthcare bill, the line item under board scrutiny 5 |

Share of US healthcare costs spent on administrative overhead: 25%

Share of US healthcare costs spent on administrative overhead: 25%

Two key observations emerge from this comparison. First, cost categories that scale linearly with location count under the retainer model—such as strategy refresh, per-location SEO, and per-engagement reporting—are flattened under account-level automation. Second, categories that should not flatten, like medical accuracy review, location-specific compliance checks, and creative judgment on service-line positioning, remain unit-of-work activities even after consolidation.

Another observation concerns agency margin trajectory. As principal media approaches one-third of agency billings 2, the labor-intensive activities most needed by healthcare operators become those agencies have the least incentive to staff effectively. The retainer dollar now purchases a different mix of work than it did three years ago, and this mix is diverging from healthcare's specific requirements.

Operators who calculate their own retainer figures and internal coordination payroll often find the actual cost gap is significantly wider than the agency invoice alone suggests.

Governance has to exist before the software does

Forrester's research on CMO-led AI transformation reveals a critical insight for healthcare operators considering platform contracts: AI doesn't fix broken systems; it accelerates existing processes. This makes orchestration the most vital skill for marketing teams 3. A pharmaceutical executive echoed this, stating, "AI cannot fix a broken system. It only accelerates what works" 3.

For multi-location healthcare programs, this translates directly: if approval workflows are unclear before platform implementation, they will be ten times more chaotic afterward. If medical accuracy review relies on a single clinician's inbox today, that inbox will become the bottleneck determining how quickly 200 locations can publish content tomorrow. The platform will expose these underlying inefficiencies.

McKinsey's healthcare analysis reinforces this warning: only about 30% of large digital transformation efforts succeed, with the most common obstacle being the gap between pilot and production 5. Healthcare programs that treat governance as a secondary consideration often fall into the 70% that fail. Pilots may run smoothly because a small team understands the workflow, but production breaks down when processes aren't formally documented.

Governance for healthcare marketing automation isn't just a compliance document; it's a working agreement on four key questions, answered before procurement: who approves what, who owns medical accuracy sign-off, what data feeds the platform, and what constitutes success at the service-line and location level. Forrester is explicit: "Organizations without clear decision rights and shared definitions of success watch pilots linger and momentum fizzle" 3. The platform contract won't change this pattern; effective governance design will.

Decision rights, medical accuracy review, and the orchestration layer

Decision rights are paramount because they are the easiest to fix and the most costly to neglect. A multi-location operator with fragmented ownership across regional marketing managers, a corporate brand team, and a compliance office cannot effectively run an account-level platform until these groups agree on which decisions are centralized and which remain local. Forrester identifies fragmented ownership and misaligned incentives as structural conditions that AI adoption exposes 3. Healthcare operators who bypass this step will inevitably confront these issues under deadline pressure during content sprints.

Medical accuracy review is the second critical design choice, often underestimated. The review gate cannot be dependent on a single clinician's calendar. It requires a defined workflow with named reviewers per service line, measurable turnaround SLAs, and an audit trail that persists through staff changes. The goal is not to slow content creation but to ensure the speed is defensible to regulators, malpractice carriers, and boards reviewing patient outcomes. Research consistently flags clinician burnout as a constraint on processes that increase workload 6, meaning review tools must compress, not expand, reviewer time.

The orchestration layer is the third component, frequently understated in platform demonstrations. Orchestration is the connective tissue linking strategy approval, content production, paid media execution, SEO updates, and reporting. Billy Hackenson, a VP at Cisco, framed leadership's role as empowering people with the right tools, education, and clarity to drive outcomes 3. In a healthcare marketing function, this clarity manifests as a single workflow where a service-line strategy decision automatically triggers downstream content briefs, schema updates, and bid adjustments, without manual handoffs. McKinsey's work on scalable automation emphasizes reshaping work rather than layering software onto existing inefficiencies 8. Operators who design effective orchestration build a platform that compounds value; those who skip it merely accelerate the production of incorrect content.

See How Top Healthcare Marketers Are Replacing Agencies with Automation

Request a custom demo to benchmark automated marketing workflows against agency results. Discover scalable, compliant solutions that reduce costs and accelerate patient acquisition across all locations.

Platform architecture for medical accuracy and multi-location coordination

Software selection is a common stumbling block in healthcare automation transitions. The market is saturated with platforms designed for SaaS funnels, e-commerce, or B2B nurture sequences. Healthcare buyers often find that while these tools offer impressive demonstrations, their production reality fails to meet compliance requirements.

Three architectural questions differentiate platforms capable of handling a multi-location healthcare workload from those that will falter.

First, is medical accuracy review a native gate within the production workflow, or a bolt-on step that the marketing team must manually staff and enforce? For a dermatology platform or a behavioral health network, generic content velocity isn't the objective; defensible, reviewed content at velocity is. McKinsey's healthcare service operations research highlights that automation ignoring the review layer creates speed that cannot be legally utilized 5. The platform must treat clinical sign-off as a primary workflow object, not a mere checkbox.

Second, is the data model account-level or campaign-level? A 40-location urgent care chain doesn't need 40 instances of the same platform. It requires one instance with location, service line, and market as dimensions within a unified taxonomy. Forrester's analysis of AI in marketing organizations is clear: fragmented ownership and unclear decision rights are conditions that AI exposes, and the platform's data architecture either reinforces or compresses this fragmentation 3. Account-level platforms enable consolidation, whereas campaign-level platforms replicate the per-location handoff problem within the software itself.

Third, does the platform integrate execution across content, technical SEO, paid media, and reporting based on a shared plan, or does it cover only one segment, assuming the operator will integrate the rest? PwC and ANA found that marketing-driven profitability multipliers arise from AI deployed across the entire funnel, not confined to a single channel 4. Healthcare operators who purchase separate tools for content, SEO, paid media, and reporting merely recreate the agency coordination problem, but with software vendors instead of account managers. McKinsey's work on scalable automation makes a similar point about reshaping work rather than layering tools onto existing organizational seams 8.

Framed this way, the architectural discussion is concise. Platforms that fail any of these three questions are merely tools. Platforms that pass all three function as operating systems for a multi-location growth program.

The 12-stage content pipeline and where the review gate sits

Healthcare content production is a multi-stage pipeline, and the placement of the medical accuracy review gate within this pipeline is crucial for regulated operators.

A robust production sequence typically involves twelve stages: keyword and intent research, competitor gap analysis, search intent mapping, outline construction, draft generation, brand voice alignment, medical accuracy review, editorial pass, schema and metadata assembly, internal linking, image generation, and publishing with version control. Each stage is a distinct checkpoint with an owner and an artifact, ensuring an auditable end-to-end pipeline.

The medical accuracy review gate should be positioned in the middle of this sequence, not at the end. Placing review after editorial polish wastes reviewer time on content that might require clinical rework. Placing it before brand voice alignment forces clinicians to review raw, unrefined drafts. The optimal placement is after the substantive draft and brand alignment are complete, but before metadata, schema, and publishing artifacts are produced. This sequencing ensures clinician time is focused on clinical content, not copy editing.

The review workflow itself requires three properties: named reviewers per service line, so cardiology content isn't stuck in a generalist's queue; measurable and reported turnaround SLAs, to identify bottlenecks before they impact publishing schedules; and an audit trail linked to the published asset, allowing regulators or carriers to trace who reviewed what and when. Healthcare adoption research consistently highlights clinician burnout as a constraint on processes that increase workload 6, meaning review tools must compress, not expand, reviewer time per asset.

Pipelines designed with this architecture produce content that organizations can confidently publish. Conversely, pipelines that treat review as optional often result in a backlog of drafts awaiting unprioritized sign-off.

Replace, hybridize, or delay: how operators are actually sequencing the transition

The transition decision typically falls into three patterns, primarily determined by the state of internal governance rather than the size of the operational footprint.

Replace is the most straightforward but also the rarest path. It suits operators who already have clearly defined decision rights, an established medical accuracy review workflow, and a marketing team capable of owning end-to-end execution. The retainer ends on a specified date, the platform assumes the work, and the team operates under the new model immediately. Forrester's CMO transformation research emphasizes that organizations with clear decision rights and shared definitions of success are those where AI adoption thrives 3. Operators lacking this foundation who attempt a full replacement often discover critical gaps within two months, such as a service-line launch missing its publishing window due to unresolved clinical sign-off.

Hybridize is the approach most multi-location operators are adopting in 2026. The platform takes over activities that scale linearly with location count—such as service-line content, location pages, technical SEO, paid search hygiene, and reporting—while the agency retains a narrower scope for brand campaigns, creative concepting, or specialized media buys. The retainer shrinks, and the agency relationship continues in a more focused capacity. The internal team uses this hybrid period to develop the governance capabilities required for eventual full replacement. McKinsey's work on scalable automation advocates for reshaping work in stages rather than layering software onto existing inefficiencies 8. Hybridization provides the necessary time for this reshaping.

Delay is the appropriate choice for operators whose internal conditions are not yet ready for either replacement or hybridization. This includes situations with fragmented ownership across regional managers and corporate brand, no named clinical reviewers, or a lack of agreement on what constitutes a successful patient acquisition outcome at the service-line level. Forrester's finding that AI accelerates existing systems cuts both ways here 3. An operator who signs a platform contract before addressing these foundational issues will merely accelerate the production of work that cannot be approved, published, or measured. Delay does not imply inaction; it means prioritizing six months of governance work, followed by a hybrid entry point, and then a full replacement on a timeline that the team can confidently present to the board.

The most frequent failure pattern is a seemingly decisive full replacement announced at a quarterly review, executed within a 90-day timeline, with governance deferred. McKinsey's healthcare transformation data shows that only about 30% of large digital efforts succeed 5. The 70% that fail are rarely due to technology shortcomings; they are typically a result of flawed sequencing.

Frequently Asked Questions

References

- 1.PwC and Association of National Advertisers (ANA) AI Research.

- 2.Predictions 2026: Marketing Agencies Resign Their Agency.

- 3.AI Is Reshaping Marketing, And CMOs Must Lead The Transformation.

- 4.Marketing in the AI era: To matter more or cost less?.

- 5.Reimagining healthcare industry service operations in the age of AI.

- 6.Adoption of artificial intelligence in healthcare: survey of health systems in the United States.

- 7.Predictions 2026: Marketing Agencies - Forrester.

- 8.Making healthcare more affordable through scalable automation.