Key Takeaways

- Traditional content ROI math fails because it treats content as a single-touch conversion channel, while branded content compounds across customer, product, and financial markets simultaneously 5.

- Report branded content through two ledgers: a quarterly pipeline ledger tracking qualified calls, booked revenue, and CAC efficiency, and an annual equity ledger translating awareness, relevance, and power into a valuation figure.

- Lead CFO conversations with the income-based valuation approach, footnote the cost-based number as a defensible floor, and reserve market-based comparisons for M&A contexts 1.

- Call-level attribution — dynamic number insertion, recording, and qualification tagging — is the instrumentation that connects content touches to booked revenue in high-consideration service categories 3.

Why the Old Content ROI Math Fails in the Boardroom

The standard content ROI formula — traffic times conversion rate times average deal size, minus production cost — collapses the moment a CFO asks the second question. It treats content as a direct-response channel with a single touch, a single conversion event, and a single accounting period. Branded content behaves nothing like that. It compounds, it shapes intent months before a form fill, and its financial signal shows up across customer, product, and financial markets simultaneously 5.

That mismatch is why marketing VPs lose budget arguments they should win. The engagement dashboard — sessions, dwell time, shares, MQLs — measures activity, not value. It cannot answer the question a board actually asks: what did this asset contribute to enterprise value, and how does that contribution compare to the paid media line item sitting next to it? Senior leaders evaluate marketing on strategic contribution and alignment with business strategy, not on tactic-level output 6.

There is a deeper methodological problem. Research on content marketing effectiveness finds that measurement is confounded by weak attribution and non-standardized metrics, which makes isolated tactic-by-tactic ROI claims fragile under scrutiny 3. In high-stakes service categories — legal intake, behavioral health admissions, dental consults, senior living tours — a single qualified inquiry can be worth thousands, yet the content touch that seeded that inquiry is usually invisible in the CRM. The math fails not because content lacks value, but because the ledger only records half of it.

The fix is not a better dashboard. It is a different reporting structure: one ledger for near-term pipeline outcomes and a second for the brand asset content builds over years. The sections that follow build both, in the vocabulary a CFO already uses for other capital on the balance sheet.

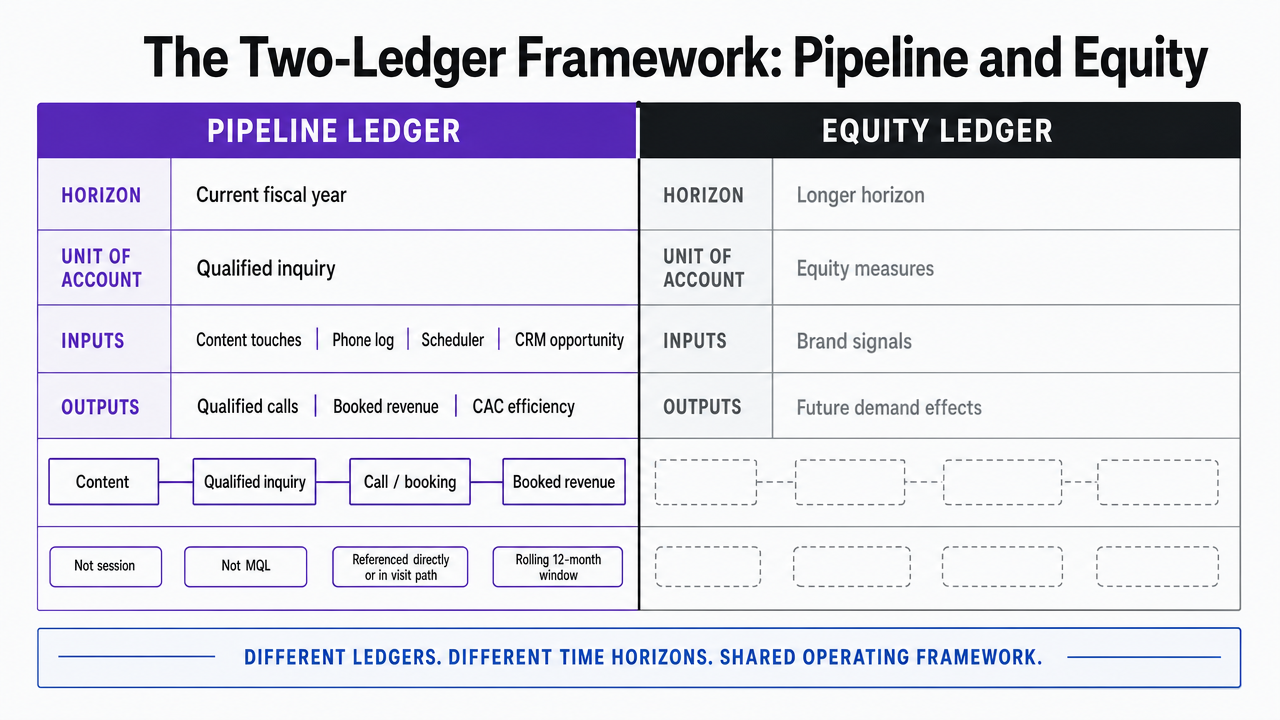

The Two-Ledger Framework: Pipeline and Equity

The Pipeline Ledger: Qualified Calls, Booked Revenue, CAC Efficiency

The pipeline ledger tracks what content produces inside the current fiscal year. Its unit of account is the qualified inquiry, not the session, and its terminal metric is booked revenue, not a marketing-qualified lead. For a service business where a single admissions call, consult booking, or intake conversation can carry four- or five-figure lifetime value, the ledger has to reach past the form fill and land on the phone log, the scheduler, and the CRM opportunity record.

Three line items belong on this ledger:

- Qualified inquiries attributable to content touches — calls and bookings where a piece of branded content sat in the visit path or the caller referenced it directly.

- Booked revenue from those inquiries, measured on a rolling twelve-month window to account for consideration cycles that stretch past a single quarter.

- Customer acquisition cost efficiency, expressed as content-influenced CAC versus paid-channel CAC in the same period.

Empirical work supports the underlying causal chain. A structural-equation study of digital content marketing delivered through a mixed-reality training platform found that content quality had a significant positive effect on online purchase intention, though the authors caution the finding is bounded by the specific environment they studied 2. Analogous evidence from higher-education recruitment — another high-consideration, high-stakes decision journey — shows content strategy influencing inquiries and enrollments through a multi-touch journey rather than a single conversion event 8.

Two disciplines keep the ledger defensible. Attribution has to be call-level and booking-level, not form-fill-level, because the qualified inquiry in these verticals is almost always a phone conversation. And measurement has to be standardized across the period, since content marketing effectiveness research finds tactic-by-tactic ROI claims collapse under weak, non-standardized measurement 3. Get both right, and the ledger reads like a revenue statement.

The Equity Ledger: Brand Value as a Compounding Asset

The equity ledger tracks what content builds beyond the current period. Its unit of account is the brand itself, treated as an intangible asset with measurable inputs and a capitalizable cash flow. Where the pipeline ledger answers what content earned this quarter, the equity ledger answers what content is worth on the balance sheet, and how that worth changed year over year.

Three inputs drive this ledger. Brand awareness, relevance, and power — the measurable proxies Harvard Business School Online identifies as trackable through surveys and digital data over time 4. These are not direct financial figures, and the same guidance flags that tension explicitly: equity metrics are proxies, and finance leaders will treat them as such unless translated into dollar terms 4. That translation is where valuation methodology enters, and where the equity ledger earns its seat next to the pipeline ledger.

Columbia Business School research reinforces why a second ledger is necessary at all. Brand equity manifests across customer, product, and financial markets simultaneously, meaning a content investment can improve loyalty, support pricing power, and lift financial-market perception at the same time — effects a single-period pipeline report cannot capture 5. The academic literature also provides a mechanism for capitalization: a brand perpetual value framework that treats brand-related cash flows as a perpetuity, discounted to present value, with explicit assumptions about growth and discount rate that a CFO can interrogate 7.

The equity ledger, in practice, records three things per year:

- Movement in the equity input scores

- The valuation output that translates those movements into dollars

- The assumptions behind the translation

That third column is what separates a defensible number from a marketing claim.

Visualize the core two-ledger framework that structures the entire article, showing how pipeline and equity ledgers differ in horizon, unit of account, inputs, and outputs

Visualize the core two-ledger framework that structures the entire article, showing how pipeline and equity ledgers differ in horizon, unit of account, inputs, and outputs

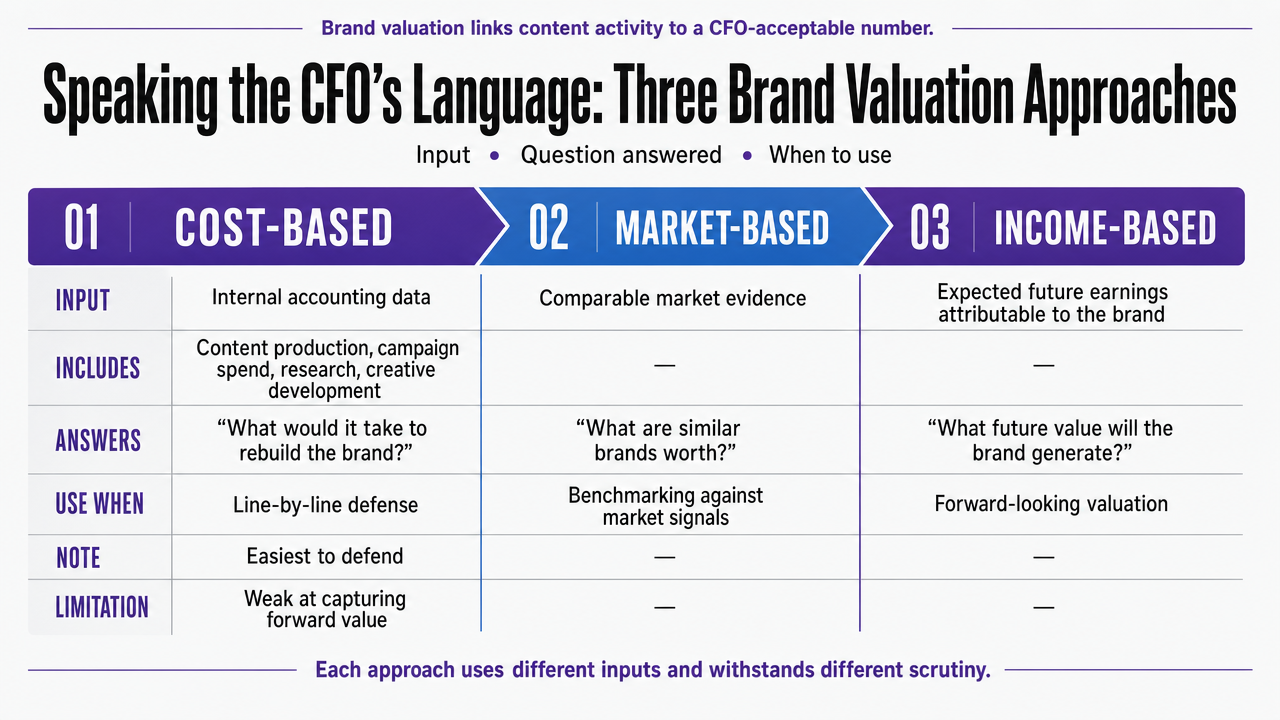

Speaking the CFO's Language: Three Brand Valuation Approaches

Brand valuation is the bridge between content activity and a number a CFO will accept on a financial report. Harvard Business School Online defines it as estimating the economic significance of a brand's tangible and intangible assets, and identifies three approaches finance leaders recognize: cost-based, market-based, and income-based 1. Each answers a different question, requires different inputs, and holds up to a different kind of scrutiny.

The cost-based approach values the brand at what it would take to rebuild it — cumulative content production, campaign spend, research, and creative development treated as capitalizable investment. Its input is internal accounting data, which makes it the easiest number to defend line-by-line and the weakest at capturing forward value. A CFO will accept the arithmetic and then ask what the brand is actually worth to a buyer or an income stream. Use this approach when the reporting posture is conservative, or when the goal is to establish a floor.

The market-based approach values the brand by reference to comparable transactions — what similar brands have sold for, or what royalty rates comparable brands command. Its input is external transaction data, which makes it persuasive in M&A conversations and thin in categories where comparables are sparse. Multi-location service brands in legal, dental, or behavioral health rarely find clean comps, so this approach tends to appear in appendix material rather than the primary valuation.

The income-based approach values the brand by the cash flows attributable to it, discounted to present value. Its input is a forecast of brand-driven revenue, a discount rate, and an assumption set the CFO can interrogate. This is the approach that most naturally connects branded content to enterprise value, because content investments that lift pricing power, retention, or acquisition efficiency show up directly in the cash flow forecast. HBS guidance flags a shared caution across all three: no single method is complete, and executives expect multiple approaches presented side by side to triangulate a defensible figure 1.

The operational takeaway is straightforward. Marketing VPs should lead with the income-based number, footnote it with the cost-based number as a floor, and reserve the market-based number for transaction contexts. Presenting all three, with assumptions visible, is what moves the conversation from marketing claim to valuation exercise.

Compare the three brand valuation approaches (cost-based, market-based, income-based) referenced from HBS, showing input, question answered, and when to use each — directly supporting the section's framework

Compare the three brand valuation approaches (cost-based, market-based, income-based) referenced from HBS, showing input, question answered, and when to use each — directly supporting the section's framework

Test branded content ROI measurement in real time

Validate your content’s business impact with live campaign data before committing to a long-term plan.

Instrumenting Content: Call-Level Attribution as the Missing Link

The pipeline ledger only works if the attribution model reaches the phone. In legal intake, behavioral health admissions, dental consults, and senior living tours, the qualified inquiry is almost never a form fill. It is a call — often prompted by content the caller consumed hours or weeks earlier, and rarely referenced explicitly on the CRM opportunity record. Without instrumentation at the call layer, the connection between a branded asset and a booked revenue event stays invisible, and the ROI argument stays theoretical.

Content marketing effectiveness research finds that measurement is one of the primary determinants of whether content investments produce demonstrable outcomes, and that non-standardized attribution is a recurring source of weak ROI claims 3. The higher-education recruitment analog is instructive: content shaped inquiries and enrollments through a multi-touch journey where the decisive interaction was rarely the first or last touch 8. Service categories with four- and five-figure lifetime values follow the same pattern. The caller has read the article, watched the explainer, or found the location page. The CRM only records the phone number.

Closing the gap requires three instrumentation layers working together:

- Dynamic number insertion assigns tracked numbers to content pages, so a call originating from a blog article, service page, or campaign landing page carries source metadata into the phone log.

- Call recording and transcription capture what actually happened on the call — whether the caller referenced specific content, whether the inquiry was qualified, whether the appointment was booked.

- Automated call analysis then tags qualified inquiries, flags missed opportunities, and links each conversation back to the content touch that seeded it.

The reporting output is a call-influenced revenue figure the CFO can audit. Each booked consult carries a content attribution stamp, a qualification tag, and a revenue value. Aggregated over a quarter, that becomes the top line of the pipeline ledger. Aggregated over a year, it becomes the input to the income-based valuation described earlier — content-attributable cash flows, discounted, translated into brand value on the equity ledger. This is the operational reason a VP can now credibly argue content ROI without expanding the team: call intelligence closes the attribution gap that used to require an analyst, a call center audit, and a quarter of manual reconciliation.

Measuring What Content Actually Moves in Brand Equity

Branded content does not move revenue directly. It moves the equity inputs that eventually move revenue, and the distinction matters when a marketing VP is arguing budget in front of a CFO. Harvard Business School Online identifies three measurable equity inputs finance leaders can be walked through: awareness, relevance, and power, each trackable over time through surveys and digital data 4. These are the levers content actually pulls. The pipeline metrics on the ledger downstream — qualified calls, booked consults, retention — respond to changes in those inputs, not to changes in session counts.

Awareness : The entry condition. It measures whether the brand is present in the consideration set when a caller starts researching a legal matter, an admissions decision, or a senior living tour. Content that expands awareness widens the top of the qualified-call funnel months later.

Relevance : The fit condition. It measures whether the brand is perceived as appropriate for the specific need, and it responds to editorial depth, category specificity, and expert framing — the exact attributes branded content controls.

Power : The preference condition. It measures whether the brand is chosen over alternatives at the decision point, and it shows up on the ledger as close rate on qualified inquiries and price realization on booked services.

Columbia research reinforces why this three-input model is worth the reporting effort: brand equity manifests simultaneously in customer, product, and financial markets, and content investments that move any single input can produce effects across all three 5. HBS guidance is equally direct about the limit — these inputs are proxies, not direct financial figures, and finance leaders will treat them as such unless translated into dollar terms through the valuation methods described earlier 4. The instrumentation is straightforward. A recurring brand tracker measures awareness, relevance, and power against a defined competitive set on a quarterly or semiannual cadence. Digital behavior data — branded search volume, direct traffic to service pages, return visits before a call — corroborates the survey signal. Each input is scored, movement is timestamped against content publication, and the movement is then mapped to the pipeline outcome it shaped one or two quarters later. That mapping is what turns an equity metric into evidence a CFO will accept as an input to valuation.

A Reporting Cadence That Survives a Boardroom Challenge

Cadence is what separates a ROI argument from a marketing update. The two ledgers described earlier need different reporting rhythms because they answer different executive questions on different time horizons. A quarterly report on brand valuation invites false precision. An annual report on qualified calls invites the wrong intervention. The rhythm has to match the signal.

The quarterly pipeline ledger is the near-term artifact. It carries three lines: qualified calls attributable to content touches, booked revenue from those calls on a rolling twelve-month window, and content-influenced CAC compared against paid-channel CAC in the same period. Presented every ninety days, it gives the C-suite what senior leaders expect from marketing — clear evidence of strategic contribution against business objectives 6. The report is short. Three numbers, a variance line against the prior quarter, and a note on any measurement changes that could affect comparability 3.

The annual equity ledger is the long-horizon artifact. It records movement in the three equity inputs — awareness, relevance, and power — measured through a recurring brand tracker and corroborated by digital behavior data 4. It then translates that movement into a valuation delta using the income-based approach as the headline number, with a cost-based floor and, where comparables exist, a market-based reference 1. The capitalized figure applies the perpetuity framework: brand-attributable cash flows discounted to present value, with growth and discount rate assumptions stated explicitly so the CFO can interrogate each one 7. That transparency is what makes the number defensible rather than promotional.

Two operational rules keep the cadence intact. Nothing on the equity ledger changes methodology mid-year without a footnote and a bridge to the prior figure. And no quarterly pipeline number is presented without its attribution model attached, so a board member can trace any booked revenue line back to the specific content touch that carries it.

Quantify Branded Content ROI With Data-Driven Attribution

Connect with a specialist to see how enterprise teams use unified analytics to attribute pipeline impact, measure conversion lift, and generate C-suite-ready ROI reports for branded content investments.

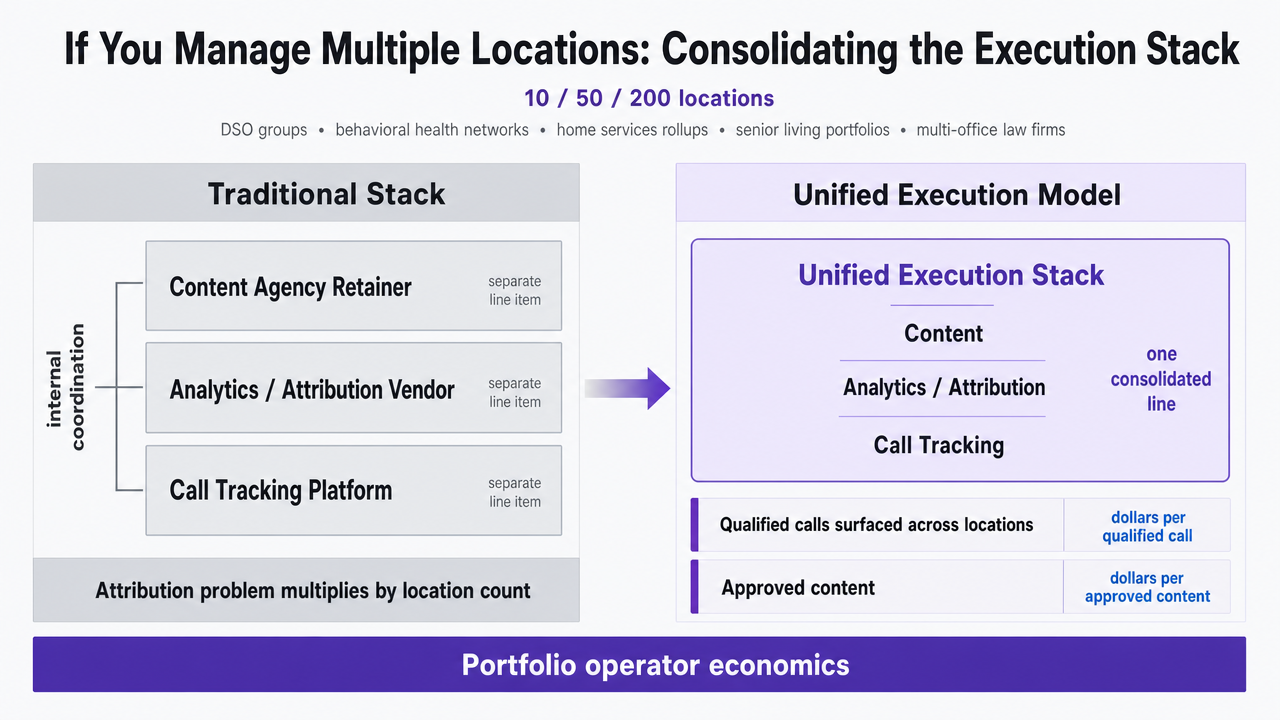

If You Manage Multiple Locations: Consolidating the Execution Stack

The reader shifts here. The framework above applies to any marketing VP defending content budget, but the economics change for operators running ten, fifty, or two hundred locations under a single brand — DSO groups, behavioral health networks, home services rollups, senior living portfolios, multi-office law firms. At that scale, the attribution problem multiplies by location count, and so does the vendor stack that used to solve it.

The traditional configuration carries three separate line items: a content agency retainer, an analytics or attribution vendor, and a call tracking platform, each priced independently and each requiring internal coordination. The unit economics that matter to a portfolio operator are not vague savings but dollars per qualified call surfaced across locations and dollars per approved content asset shipped. That is the frame a CFO will accept.

| Cost line | Traditional stack | Unified execution model |

|---|---|---|

| Content production | Agency retainer (variable) | Platform subscription |

| Call attribution | Call tracking vendor (variable) | Included |

| Analyst time | In-house FTE or agency reporting hours | Included in workflow |

| Anchor pricing | Sum of three contracts | $599/month after trial |

| Unit metric | Cost per asset shipped, tracked separately from calls | Cost per qualified call surfaced and per approved asset shipped |

Consolidation matters for a reason beyond price. Content marketing effectiveness research finds that non-standardized measurement across channels and periods is a primary reason ROI claims fail scrutiny 3. When each location reports through a different attribution stack, the pipeline ledger cannot be aggregated cleanly, and the equity ledger cannot be tied back to specific content investments. A single execution layer — where content publication, call attribution, and reporting sit in one approval workflow — is what lets a multi-location VP present one number to the board instead of reconciling twenty. Vectoron is one option built around that consolidation logic.

Visualize the traditional stack versus unified execution model comparison table already present in the section, reinforcing the cost line consolidation argument for multi-location operators

Visualize the traditional stack versus unified execution model comparison table already present in the section, reinforcing the cost line consolidation argument for multi-location operators

What the CFO Will Push Back On, and How to Answer

Three objections come up in every boardroom conversation about branded content ROI. Preparing exact answers before the meeting is what separates the VP who keeps the budget from the one who defends it every quarter.

"Your attribution model is picking winners." The CFO's suspicion is that content is being credited for calls it did not cause. The answer is methodological transparency, not a stronger claim. Present the attribution logic — dynamic number insertion at the page level, call recording as corroboration, qualification tagging at the conversation level — and name the known limits. Content marketing effectiveness research is explicit that non-standardized measurement is where ROI arguments break, so the defense is showing the standard, not hiding it 3. When the model is auditable, the number stops being a marketing claim.

"Brand equity scores are not dollars." This is the correct objection, and the honest answer concedes it. Awareness, relevance, and power are proxies, and HBS guidance flags that finance leaders will treat them as such until translated into financial terms 4. The translation is the income-based valuation on the annual equity ledger — brand-attributable cash flows discounted to present value, with growth and discount rate stated explicitly so each assumption is interrogable 7. The equity score is the input. The valuation is the output the CFO signs off on.

"Why not just spend the budget on paid media?" Because the two ledgers measure different assets. Paid media buys inquiries in the current period; content compounds across customer, product, and financial markets over multiple periods 5. Present the CAC efficiency comparison on the pipeline ledger and the valuation delta on the equity ledger side by side. The choice stops being content versus paid and starts being short-horizon spend versus asset accumulation — a framing the C-suite already applies to every other capital decision 6.

Frequently Asked Questions

References

- 1.What Is Brand Valuation? Expert Tips & Techniques.

- 2.Evaluating the Effectiveness of Digital Content Marketing Under Mixed Reality Training Platform Environment.

- 3.Determinants of content marketing effectiveness: Conceptual and empirical evidence.

- 4.Brand Equity Explained: How to Build and Measure Success.

- 5.Brands and Branding: Research Findings and Future Priorities.

- 6.The C-Suite Perspective: Leadership & Integrated Marketing.

- 7.Measuring the Financial Value of Brand Equity: The Perpetuity Perspective.

- 8.How Content Marketing Can Impact Colleges' Recruitment of Students.