Key Takeaways

- Defensible audit pricing rests on three structural variables: site complexity, vertical LTV, and attribution depth, not page count or generic rate cards that compress margin over time.

- Audits scoped against Forrester's four TEI quadrants—benefits, costs, flexibility, and risk 3—produce a fee buyers can defend internally because every dollar maps to a named, interrogable input.

- Three working tiers calibrate market pricing: Diagnostic at $1,500–$5,000, Comprehensive at $6,000–$18,000, and Enterprise multi-location at $20,000–$75,000-plus, each tied to footprint and modeling depth.

- Agency owners should standardize the modeling template across the portfolio and cap audit hours at the point where additional analysis no longer changes a benefit, cost, flexibility, or risk input.

Why audit pricing breaks down without an economic model

Most SEO audit pricing collapses the moment a client asks what the deliverable is actually worth. A 60-page PDF priced at $4,500 reads the same as a 60-page PDF priced at $18,000 if neither is tied to a revenue model the buyer can defend internally. That is the underlying reason audit fees compress year after year, and why agencies that sell audits as deliverables end up competing against freelancers running Screaming Frog exports.

The fix is not better packaging. It is reframing the audit as the first input to an economic business case, the same way Forrester's Total Economic Impact methodology treats any strategic spend — benefits, costs, flexibility, and risk modeled together rather than priced in isolation 3, 4. Audits scoped this way carry a different fee logic because the output is not a checklist; it is a quantified path to revenue with named assumptions.

Three structural variables set defensible audit price: site complexity, vertical lifetime value, and the depth of attribution work required to convert findings into a forecast. Each one moves the cost curve independently. An article that benchmarks SEO audit cost without naming these variables is benchmarking the wrong thing — the price tag rather than the model that justifies it.

The three variables that should set audit price

Site complexity: page count, template variants, and regulatory overlay

Complexity is the variable agencies most often underprice. A 240-page personal injury site running 12 practice-area templates, three location templates, and a blog with five author profiles requires a different crawl, sample, and remediation plan than a 60-page B2B site running two templates. The work scales with template variants more than raw page count — every template carries its own schema, internal linking pattern, and indexation logic that has to be validated independently.

Regulatory overlay compounds this. A behavioral health network operating across state lines, a dental DSO publishing provider bios under HIPAA-adjacent content rules, or a senior living operator subject to ADA accessibility scrutiny all require audit scope that goes past technical SEO into substantiation review. That work is not optional, and it does not finish in a week.

Three complexity drivers move the cost curve:

- Template variants (each one adds QA hours)

- Multi-location footprint (each location multiplies local entity, NAP, and schema validation)

- Regulatory overlay (each adds review cycles)

Agencies that scope audits by URL count alone consistently underbid the work and absorb the margin loss themselves.

Vertical LTV: why a personal injury firm and a SaaS startup do not warrant the same audit

A signed personal injury case can be worth $25,000 to $80,000 in fee revenue. A new patient in a dental implant practice carries a multi-year LTV north of $6,000. A SaaS startup acquiring a $49/month subscription is operating on a different economic plane entirely. The audit fee that produces predictable ROI in the first two cases would be irrational in the third.

Forrester's ROI model for SEO frames the program as a business investment with modeled benefits, costs, risks, and flexibility 3. The same logic governs audit pricing. When a single recovered ranking on a high-intent term moves one additional case per quarter in a legal vertical, the audit fee is recovered before the second deliverable lands. When the same ranking recovery moves three additional trial signups in a low-ACV SaaS context, the math is structurally different.

Defensible audit pricing scales with the revenue value of the actions the audit unlocks. Agencies pricing every client off the same rate card are subsidizing low-LTV accounts with high-LTV ones — and usually losing both over time.

Attribution depth: from GA/GSC baseline to revenue-grade modeling

The third variable is how far the audit goes past diagnosis into measurement infrastructure. A baseline audit confirms that Google Analytics and Google Search Console are connected, that organic sessions tie to conversion events, and that ranking shifts can be correlated with inquiry volume — the standard mechanics UPCEA documents for tracking organic lift against enrollment goals 2. That is the floor, not the ceiling.

Revenue-grade modeling goes further: server-side event capture, call tracking with qualified-lead scoring, CRM-stamped attribution that follows an organic visitor to closed revenue, and cohort analysis that separates branded from non-branded organic. Each layer adds audit hours and pushes the deliverable into territory clients can actually defend to a CFO.

NIST's measurement framework names the standard: performance measures must be quantifiable, observable, and repeatable, and they must connect directly to the objective being managed 1. Applied to SEO audit KPIs, that means an inquiry count is not a measure unless its source, capture method, and conversion definition are stable across reporting periods. Audits that ship without that measurement spine produce findings that cannot be valued, which is why their fees stay compressed.

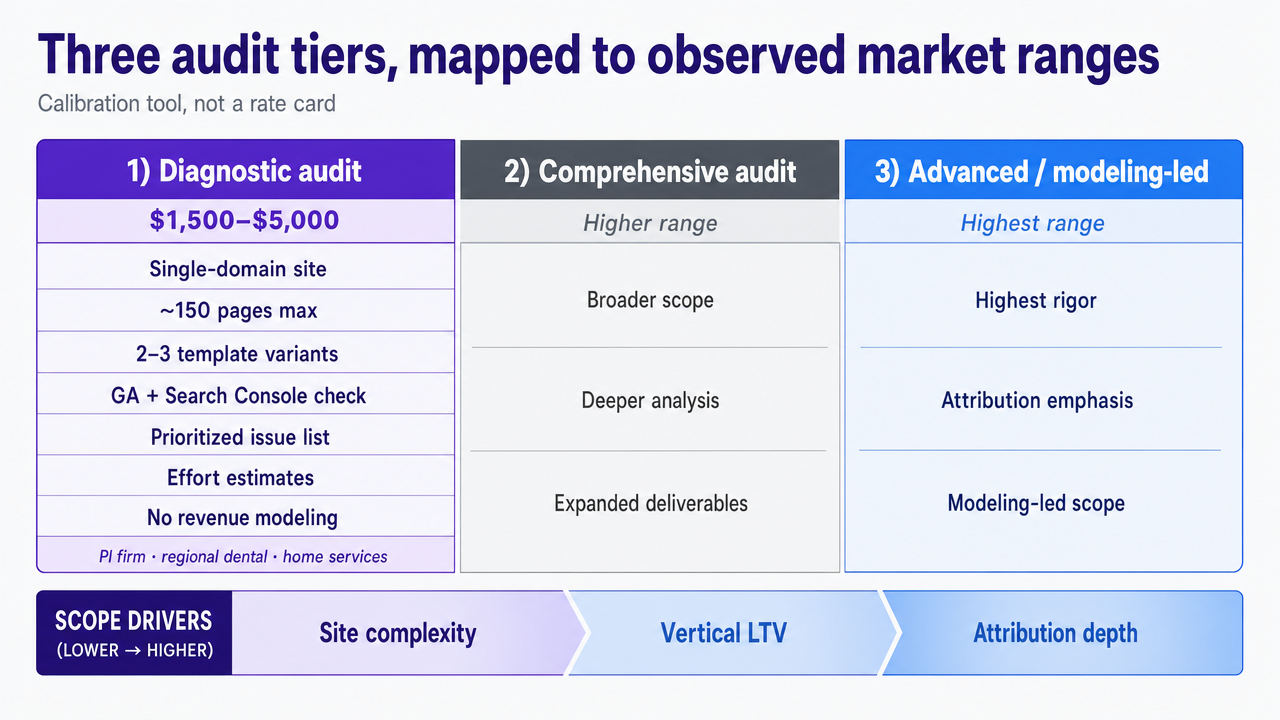

Three audit tiers, mapped to observed market ranges

The three variables — site complexity, vertical LTV, and attribution depth — collapse into three working tiers that hold up in client conversations. The price ranges below reflect observed market behavior across professional services agencies, not a sourced benchmark. They are useful as a calibration tool, not a rate card.

Diagnostic audit : Sits in the $1,500 to $5,000 range. It covers a single-domain site under roughly 150 pages, two or three template variants, and a baseline measurement check against Google Analytics and Search Console 2. The deliverable is a prioritized issue list with effort estimates. It does not include revenue modeling. A solo personal injury firm in one market, a regional dental practice with two locations, or a home services operator with a single service-area template fits this scope.

Comprehensive audit : Runs $6,000 to $18,000. Site footprint expands to 500-plus pages, five to ten template variants, and a content layer deep enough to require substantiation review. Attribution work goes past GA/GSC into call tracking and CRM-stamped conversion paths. The deliverable includes a modeled revenue case under a defined assumption set — the structure Forrester names benefits, costs, flexibility, and risk 3. A 12-attorney litigation firm, a 15-location dental group, or a behavioral health network operating in three states sits here.

Enterprise multi-location audit : Ranges from $20,000 to $75,000-plus. Site footprint moves into thousands of pages, location-template fanout, and regulatory overlay that requires named subject-matter review. A 40-location dental DSO, a national senior living operator, or a healthcare system with service-line architecture across regions defines this tier. Attribution depth includes server-side capture, qualified-lead scoring, and cohort separation of branded versus non-branded organic.

The three tiers are not interchangeable. An audit priced at the Diagnostic level for an Enterprise footprint produces a deliverable the buyer cannot defend internally. An Enterprise-tier fee charged against a Diagnostic-tier site produces margin the engagement cannot sustain past the first quarter.

Summarize the three pricing tiers and their scope drivers introduced in this section so readers can calibrate against site footprint, attribution depth, and modeling rigor

Summarize the three pricing tiers and their scope drivers introduced in this section so readers can calibrate against site footprint, attribution depth, and modeling rigor

Run a Complete SEO Audit Workflow Instantly

Benchmark audit costs and deliver real, actionable SEO insights on live projects in your first week.

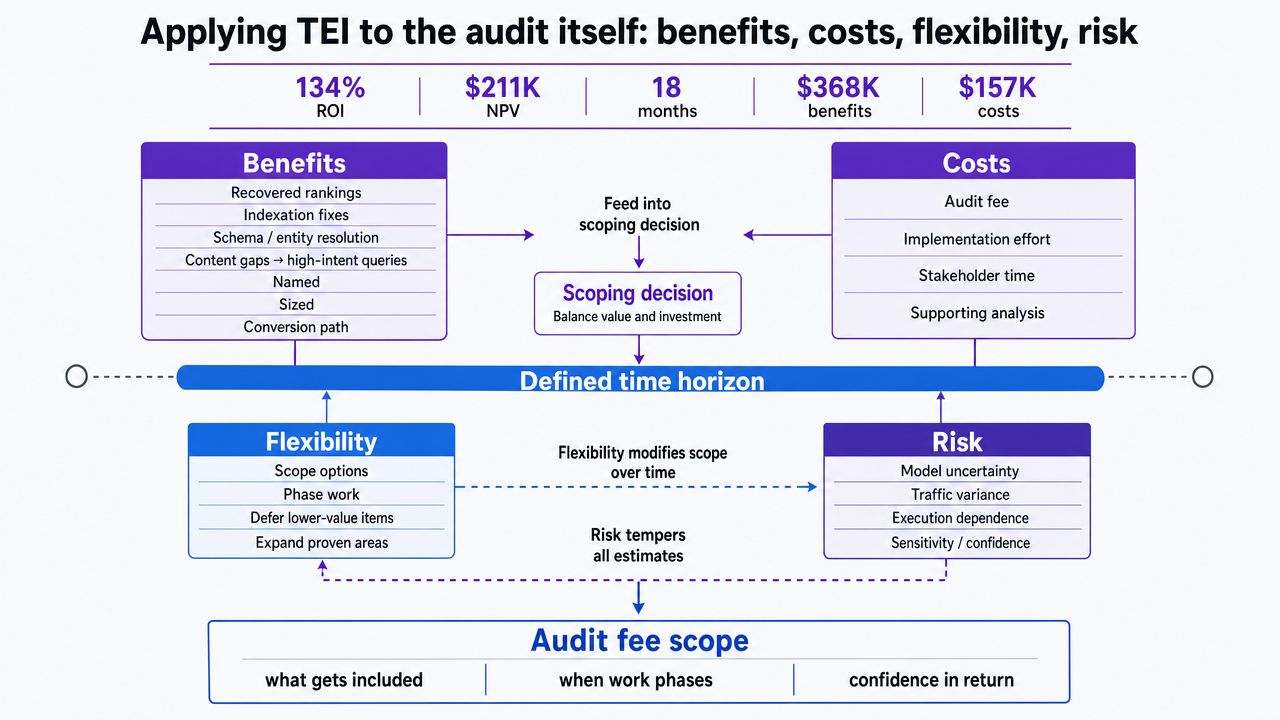

Applying TEI to the audit itself: benefits, costs, flexibility, risk

Forrester's Total Economic Impact methodology treats any strategic spend as four interacting variables — benefits, costs, flexibility, and risk — and models them against a defined time horizon. The TEI workbook itself produced a 134% ROI and $211,000 NPV over 18 months in one Forrester composite, with $368,000 in modeled benefits against $157,000 in modeled costs 4. The same four-quadrant logic applies to scoping the audit, not just the SEO program it informs.

Benefits : The modeled revenue lift the audit unlocks: recovered rankings, indexation fixes that surface previously buried inventory, schema work that improves entity resolution, and content gaps that map to high-intent queries. Each benefit gets named, sized, and tied to a conversion path before the audit invoice goes out.

Costs : The audit fee, the internal hours required to action findings, and the platform spend needed to instrument measurement. Agencies that report only the fee understate the engagement and lose credibility when the client's CFO adds the rest back in.

Flexibility : The option value the audit creates — the ability to expand into a new practice area, launch a new location, or shift content investment toward a higher-LTV segment once the technical foundation supports it. This is the quadrant most audit proposals omit entirely, and it is often where the largest defensible value sits.

Risk : The assumptions that can break the model: ranking volatility, algorithm shifts, regulatory changes, and competitor response. Forrester's ROI of SEO framing names this explicitly — benefits and costs modeled with risk and flexibility weights rather than point estimates 3. Audits priced against this four-quadrant structure produce a defensible fee because every dollar is mapped to a named input the buyer can interrogate.

Visualize the four-quadrant TEI framework the section explicitly walks through, giving readers a structural reference for how benefits, costs, flexibility, and risk interact when scoping audit fees

Visualize the four-quadrant TEI framework the section explicitly walks through, giving readers a structural reference for how benefits, costs, flexibility, and risk interact when scoping audit fees

From audit findings to a quantified revenue case

The composite SEO ROI figure and what it actually means

Forrester's most cited SEO data point is a 611% ROI recognized by a composite organization modeled across customer interviews 5. The figure is useful as a ceiling reference, not a forecast. The composite is an analytical construct — a synthesis of multiple buyers' modeled benefits and costs over a defined horizon, not a single company's actual returns.

Used correctly, the number sets the upper bound of what disciplined SEO investment can produce when benefits are sized, attribution holds, and risk weights are applied. Used carelessly, it becomes the kind of headline that gets cited on agency sales pages and then quietly retracted when a client asks for the underlying assumptions.

The operative move for an agency owner is to cite the figure once, name its scope in the same sentence, and pivot to the modeling discipline that produced it. The audit is what builds that model on a specific site. The composite ROI explains why the model is worth building.

A worked example: $140 CPI and $2,849 cost-per-student in higher ed

A concrete worked example clarifies how an audit finding becomes a revenue case. UPCEA's 2024 benchmarks for continuing and online education marketing put cost per inquiry at $140 and cost per enrolled student at $2,849, with breakdowns by program type 7. Those numbers function as the conversion economics layer that an audit's findings get multiplied against.

Consider a continuing-education program generating 4,000 organic inquiries annually with a 6% inquiry-to-enrollment rate — 240 enrolled students per year. An audit identifies indexation gaps, schema deficiencies on program landing pages, and three high-intent query clusters where the institution ranks between positions 8 and 14. Recovering those rankings produces a modeled 15% lift in qualified organic inquiries — 600 additional inquiries.

At the $140 CPI benchmark, the marginal acquisition value of those inquiries is $84,000 if the institution had to buy them through paid channels. Applied through the same 6% conversion rate, the lift produces 36 additional enrolled students. At the $2,849 cost-per-student benchmark, the substituted acquisition cost is $102,564. Combined modeled value sits near $186,000 against an audit fee in the Comprehensive tier — a defensible economic case before tuition revenue is layered in.

The scope matters. These benchmarks describe continuing and online education, not undergraduate enrollment, not B2B SaaS, not legal services. The methodology generalizes; the dollar inputs do not.

Generalizing the method to legal, healthcare, dental, and home services

The higher-ed math is a template, not a benchmark library. Each vertical carries its own CPI and LTV inputs that have to be sourced from the client's actual cost-per-lead data, CRM-stamped conversion rates, and signed-case or closed-treatment values.

A personal injury firm running paid intake at $380 per qualified lead with a 22% sign rate and an $18,000 average case fee produces a different model than the higher-ed example, but the same four-step structure: baseline inquiries, modeled lift, conversion rate, monetized outcome. A 12-location dental group with $220 cost per new-patient lead, a 40% consult-to-treatment-plan rate, and $4,800 first-year patient value produces a third variant. A regional HVAC operator with $95 cost per service call lead and $680 average ticket produces a fourth.

The discipline NIST applies to security measurement — quantifiable, observable, repeatable measures tied directly to objectives — is the same discipline that holds these models together 1. The audit's job is to surface the lift estimate and the assumption set. The client's data provides the cost and conversion inputs. The output is a defensible case the buyer's finance team can interrogate line by line.

Production economics: what an audit actually costs the agency to deliver

Audit fees are only defensible if the delivery cost behind them is known. Most agencies do not track audit production hours at the task level, which is why margins on audit work swing from 60% to negative depending on the engagement. The math is not complicated; it is just rarely done.

A Diagnostic audit typically absorbs 18 to 35 senior hours across crawl analysis, log review, GA/GSC validation, and prioritization. At a $185 blended internal cost, that floor sits near $3,300 to $6,500 in true delivery cost before the deliverable is written. Pricing the Diagnostic at $1,500 is not aggressive pricing — it is a loss leader booked against future retainer revenue, and it should be classified that way internally. Comprehensive audits run 60 to 140 hours once substantiation review, call-tracking validation, and modeled-case construction enter scope. Enterprise multi-location work routinely crosses 200 hours, and the regulatory review layer is where unplanned hours compound fastest.

Three margin pressure points show up consistently:

- Scope creep into competitive content gap analysis that was not bid

- Attribution rework when the client's GA configuration is broken

- Revision cycles when the economic case is presented without the assumption set named upfront

The discipline that holds margin together is the same discipline NIST applies to measurement — quantifiable, repeatable, observable inputs tied to a named objective 1. Audits scoped against that standard ship on time. Audits scoped against a page count do not.

See How Leading Agencies Standardize SEO Audit Spend for Predictable ROI

Request a tailored cost benchmarking analysis to compare your current SEO audit investments against industry averages and identify measurable opportunities to improve efficiency and margin control.

If you manage multiple locations or a client portfolio

The framework above prices a single audit. Agencies running 15 to 40 audits a year against a mixed-vertical book face a different problem: portfolio-level margin compression. The unit economics change when delivery capacity is the constraint, not client willingness to pay.

Three patterns hold up across multi-client portfolios:

- Diagnostic-tier audits scale linearly with senior hours and rarely cross 30% gross margin once revision cycles are counted.

- Comprehensive audits carry the strongest margin profile — 45% to 60% — because the attribution and modeling work is repeatable across clients once the agency's internal templates stabilize.

- Enterprise multi-location audits produce the largest absolute dollar margin but the longest cash cycle, often 90 to 120 days from kickoff to final invoice.

| Audit tier | Site complexity driver | ROI input that anchors the case | Margin pressure point |

|---|---|---|---|

| Diagnostic | Under 150 pages, 2–3 templates | GA/GSC-validated inquiry lift 2 | Revision cycles on undefined scope |

| Comprehensive | 500+ pages, regulated content layer | Modeled benefits, costs, flexibility, risk 3 | Attribution rework when CRM data is broken |

| Enterprise multi-location | Thousands of pages, location fanout | Per-location lift × LTV (worked via $140 CPI / $2,849 CPS in higher ed 7) | Regulatory review hours and cash cycle |

Portfolio operators that standardize the modeling layer across tiers — same four TEI quadrants, same NIST-grade measurement spine 1— compress delivery time on every subsequent audit because the analytical template is reusable. Standardizing the deliverable format, not the findings, is what moves portfolio margin from break-even to compounding.

When audit cost stops correlating with audit value

Audit fees scale with complexity, but value does not scale linearly with fee. There is a point on every engagement curve where additional audit hours produce diminishing returns against the revenue model — and agency owners who cannot name that point end up selling discovery work the client cannot action.

Three signals mark the inflection:

- When the audit's marginal finding moves into territory the client lacks the internal capacity to execute. A 200-hour Enterprise audit that surfaces 340 prioritized issues against a client team with bandwidth for 40 has produced shelfware, not value.

- When attribution rework outpaces lift modeling — when half the engagement is spent fixing the client's GA configuration rather than sizing the recovered revenue, the fee stops correlating with the economic case.

- When the deliverable redocuments findings the client's prior agency already surfaced; depth without new ground produces no incremental modeled benefit under the four-quadrant structure Forrester names 3.

The corrective is structural. Audit fees should be capped at the point where the next hour of analysis does not change a benefit, cost, flexibility, or risk input in the model. Past that line, the work belongs in the implementation engagement, priced against outcomes — not in the audit, priced against pages.

Closing the sale: pricing the audit as the entry point to a quantified engagement

The audit fee is rarely the number that closes the engagement. The model behind it is. Buyers approving five-figure audits are not paying for the deliverable — they are paying for a defensible path to revenue with named assumptions, a measurement spine they can interrogate, and a risk-weighted forecast their finance team can sign off on. Forrester's TEI work on its own advisory products produced a modeled 259% ROI and a 26% lift in transformation initiative success rates, reinforcing that decision-makers now expect quantified returns on any strategic spend — including the audit that scopes the program 10.

Pricing the audit as the entry point to that quantified engagement changes the sales conversation. The fee anchors against modeled benefits, costs, flexibility, and risk rather than against page count or competitor proposals. Retainer renewals follow because the measurement infrastructure the audit installed continues producing the inputs the model needs.

Agencies building this discipline once — and reusing the template across the portfolio — compound margin every quarter. That is the operating posture Vectoron is built to support.

Frequently Asked Questions

References

- 1.Performance Measurement Guide for Information Security (NIST SP 800-55 Rev.1).

- 2.How to Quantify Higher Education SEO ROI.

- 3.The ROI Of SEO - Forrester.

- 4.The Value Of Building An Economic Business Case With Forrester.

- 5.You Can Quantify The ROI Of SEO.

- 6.Performance measurement guide for information security.

- 7.Understanding Cost Per Inquiry in Higher Education Marketing.

- 8.Analyzing Effective Higher Education Marketing Strategies.

- 9.Higher Ed SEO Trends to Stay Competitive.

- 10.Understand The Return On Investment (ROI) Of Forrester Decisions.