Key Takeaways

- Salesforce becomes the right call when the CRM must serve as the canonical system of record across sales, success, and finance, especially past forty Sales Hub seats or when custom objects exceed HubSpot's data model.

- Zoho CRM preserves the suite model at a fraction of HubSpot's per-seat economics, trading depth in marketing automation for breadth across CRM, email, helpdesk, and analytics in one bundle.

- Pipedrive fits sales-led motions where the CRM should stay a fast, predictable deal tracker, with marketing automation handled by a separate tool like Brevo or ActiveCampaign.

- Brevo works as a volume-priced automation layer beside a thin CRM, which behaves very differently from HubSpot's contact-tier pricing once databases grow past tens of thousands of records.

- ActiveCampaign offers automation depth closer to Marketing Hub Pro than to a basic ESP, making it the SMB choice when Brevo feels too light but HubSpot feels too expensive.

Why the alternatives question stopped being about CRM swaps

The Reddit threads where SaaS growth directors trade HubSpot opinions used to read like CRM bake-offs. Pipedrive versus HubSpot. Zoho versus HubSpot. Salesforce versus HubSpot. The question was always which suite to buy. That framing has aged poorly. The current argument, visible across r/marketing, r/SaaS, and r/HubSpot, is about whether to buy a suite at all, or to assemble a thinner stack and put an AI orchestration layer on top.

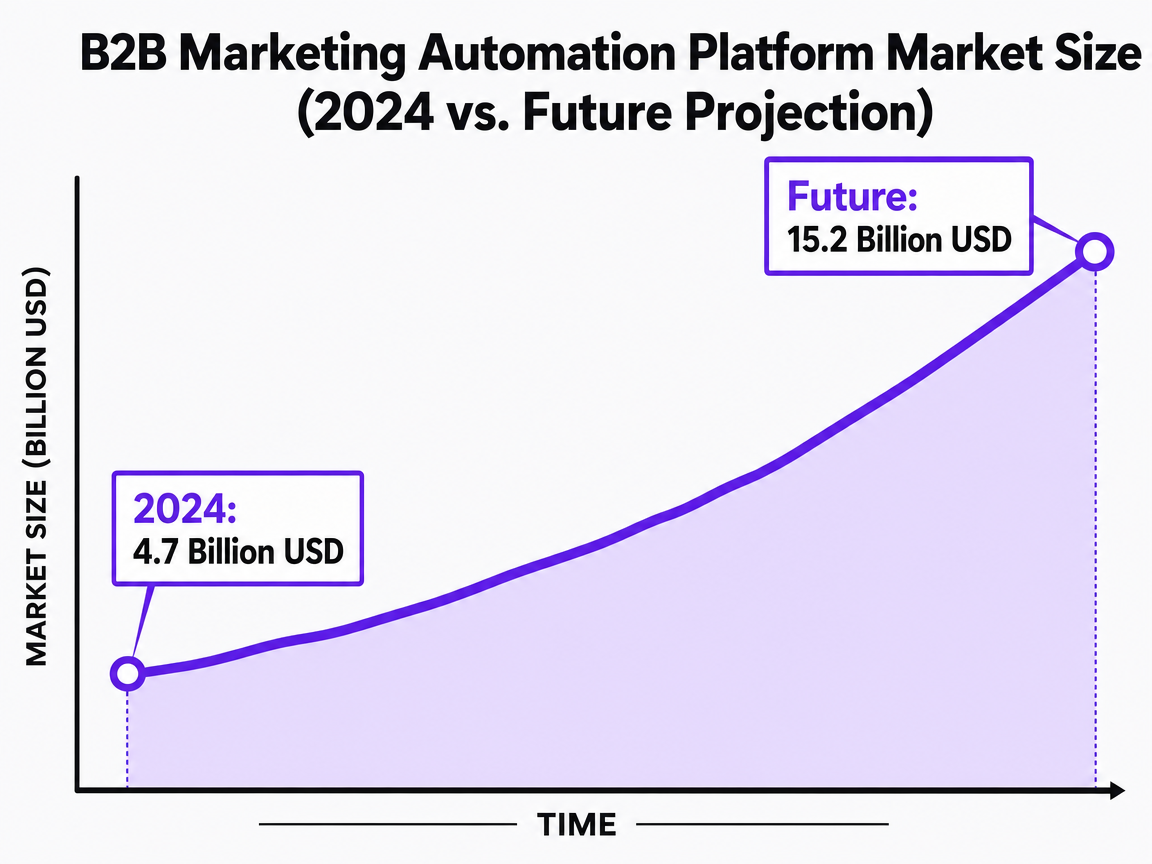

The market data supports the shift. The B2B marketing automation platforms market sat at roughly $4.7 billion in 2024 and is projected to reach about $15.2 billion in the years ahead, with growth driven by AI integration and multi-channel coordination rather than incremental feature releases from the incumbent suites 1. Forrester formalized the change by introducing a new analyst category, B2B Revenue Marketing Platforms, evaluating twelve providers across 23 criteria for targeting, personalization, and revenue orchestration rather than email blasts and form fills 13. Forrester's own analysts describe the category as a convergence of marketing automation, customer data, and analytics into integrated revenue systems 16.

That convergence reframes the alternatives question. A growth director comparing Marketing Hub Pro against a competitor is no longer choosing between two databases with workflow editors attached. They are choosing where automation lives, where the customer record lives, and where the orchestration logic lives, and increasingly those three layers belong in different products. HubSpot's own 2026 Spring Spotlight release acknowledged the trend by shipping AI Connectors that push CRM data into external models like ChatGPT, Claude, Gemini, and Copilot 5. Even the incumbent is conceding that the next decisions happen above the CRM, not inside it.

B2B Marketing Automation Platform Market Size (2024 vs. Future Projection)

B2B Marketing Automation Platform Market Size (2024 vs. Future Projection)

The market is valued at approximately $4.7 billion in 2024 and is projected to reach around $15.2 billion in the future, indicating significant growth.

What practitioners on Reddit are actually arguing about

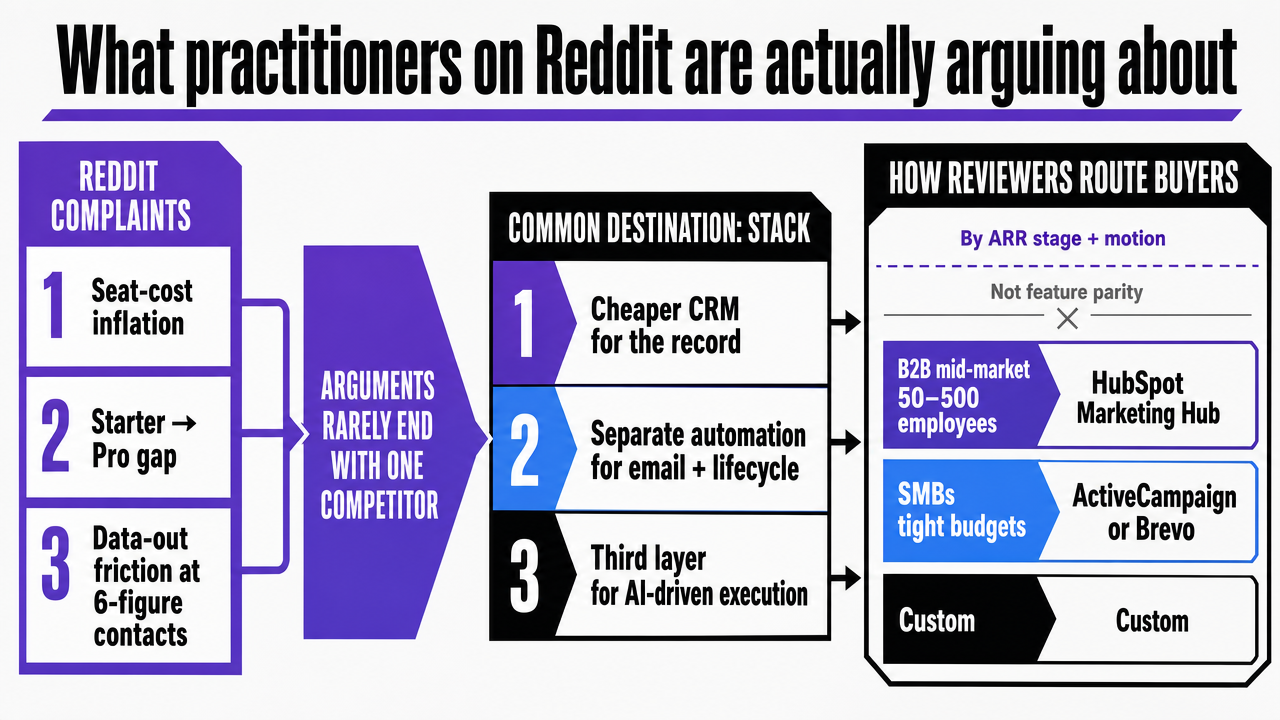

Scroll through any recent r/SaaS or r/marketing thread tagged with HubSpot, and the complaints cluster around three things:

- Seat-cost inflation as the team adds sales users

- The gap between Marketing Hub Starter and Pro

- The friction of moving data out once contacts pass six figures

The arguments rarely end with a recommendation to buy a single competitor. They end with a stack: a cheaper CRM for the record, a separate automation tool for email and lifecycle, and increasingly a third layer for AI-driven execution.

That pattern matches what independent reviewers see. Improvado's 2026 platform comparison routes buyers by ARR stage and motion rather than by feature parity, recommending HubSpot Marketing Hub for B2B mid-market companies in the 50 to 500 employee range, ActiveCampaign or Brevo for SMBs with tight budgets, and Customer.io for SaaS product-led growth 7. Zapier's 2026 alternatives list reaches similar conclusions, framing Salesforce as the choice when sales and marketing need to live in one CRM and positioning Zoho and Pipedrive against different motion types 4. Brevo's own competitor roundup concedes the central point: the ideal alternative depends on the business, not on a head-to-head feature score 6.

The Reddit consensus, then, is less about which logo replaces HubSpot and more about which architecture replaces the suite. The five tools below are the ones that show up repeatedly in those discussions, each forcing a different stack decision.

Visualize the comparison framework Reddit users and Improvado/Zapier reviewers actually use to route buyers to alternatives based on motion and ARR stage rather than feature parity

Visualize the comparison framework Reddit users and Improvado/Zapier reviewers actually use to route buyers to alternatives based on motion and ARR stage rather than feature parity

Test full-scale marketing automation in real time

Experience live campaign execution and analytics before committing—publish and measure actual results during your free trial.

The five tools growth directors switch to

Salesforce: when the CRM has to be the system of record

Salesforce shows up in Reddit threads less as a HubSpot competitor and more as the destination teams migrate toward once headcount, deal complexity, or board reporting demands force the CRM to behave as the system of record. Zapier's 2026 alternatives guide positions it bluntly as the choice when sales and marketing need to live in one CRM with enterprise-grade extensibility 4. That framing matches what growth directors describe in practice: the move usually happens when seat counts in Sales Hub push past forty, when revenue ops needs custom objects HubSpot's data model resists, or when the finance team wants forecasting tied to opportunity history rather than marketing-attributed pipeline.

The market share picture clarifies why this is the default escalation path rather than a lateral move. One 2026 vendor breakdown puts Adobe at 36% of the marketing automation market, Microsoft at 24%, Salesforce at 17%, HubSpot at 15%, and Oracle at 8% 3. HubSpot is not the category leader in installed base; it is the leader in mid-market mindshare. Growth directors who treat the alternatives question as a HubSpot-versus-everyone-else exercise tend to overlook how concentrated enterprise spend already sits inside Adobe, Microsoft, and Salesforce footprints, and how often those footprints already exist somewhere inside their own company.

The architectural decision Salesforce forces is whether the CRM owns automation or whether automation sits beside it. Pairing the core platform with Account Engagement (formerly Pardot) keeps both layers in one vendor relationship but raises total contract value substantially. Many teams pair Salesforce with a lighter automation tool instead, accepting integration work in exchange for cheaper email volume and faster iteration. Either way, Salesforce is the answer when the customer record needs to be canonical across sales, success, and finance, and when the rest of the stack should bend around it rather than the other way around.

Zoho CRM: the suite play for teams that won't unbundle

Not every growth team wants to assemble a stack. Some directors inherit lean revops functions, run finance pressure on tool count, or operate in regions where Zoho already has stronger local support than HubSpot. For those teams, Zoho CRM is the rational alternative because it preserves the suite model at a fraction of HubSpot's per-seat economics. Zapier's 2026 review describes it as an affordable CRM with strong native AI, and Brevo's competitor analysis groups it among the most realistic SMB-to-mid-market alternatives 4, 6.

The Zoho One bundle is the part of the conversation that doesn't translate well from feature comparisons. Beyond CRM, the same subscription covers email marketing, forms, analytics, project management, helpdesk, and document signing. A growth director replacing HubSpot Marketing Hub Pro plus a handful of point tools can collapse multiple line items into one. The tradeoff is depth: Zoho's marketing automation does not match HubSpot's workflow editor or attribution reporting feature-for-feature, and the UX consistency across the suite is uneven enough that practitioners regularly cite it as a complaint.

The decision Zoho forces is philosophical more than financial. A team that buys Zoho is choosing to keep the suite mental model, just with a cheaper vendor and broader functional surface. That works when the growth function is small enough that a single platform can carry sales, marketing, and support without specialist tools layered on top, and when the team has the operations capacity to configure a flexible but less opinionated system. It works less well when marketing wants best-in-class email deliverability, advanced lifecycle logic, or tight integration with product analytics, because the suite's breadth is purchased at the cost of depth in any single discipline.

Pipedrive: when the motion is sales-led and the marketing layer lives elsewhere

Pipedrive is the tool growth directors pick when they want to stop pretending the CRM should run marketing. Both Zapier and Brevo position it explicitly as a sales-led CRM with a deliberately narrow scope, designed around pipeline visibility and rep workflow rather than lifecycle orchestration 4, 6. The Reddit pattern is consistent: teams running outbound-heavy or AE-led motions migrate from HubSpot Sales Hub to Pipedrive, then bolt on Brevo, Customer.io, or ActiveCampaign for the marketing automation HubSpot used to cover.

That unbundling is the point. HubSpot's pricing assumes marketing and sales should share a database and a workflow engine. Pipedrive's pricing assumes the sales team needs a deal tracker that loads fast and behaves predictably, and that marketing automation is somebody else's problem. For growth directors managing a SaaS sales motion where SDRs and AEs touch hundreds of deals a quarter, that division of labor often produces a cleaner system. The CRM stays simple enough that reps actually use it; the automation layer can be picked on its own merits.

The cost shape is the other reason this combination shows up so often. Pipedrive's mid-tier per-seat pricing is materially below comparable HubSpot Sales Hub Pro seats, and pairing it with a sub-$100 monthly automation tool keeps total spend predictable as the sales team scales. The friction is integration: contact sync, lead routing, and attribution all become the buyer's responsibility rather than the vendor's. Teams that pick Pipedrive accept that orchestration work in exchange for tool independence. The decision is whether the growth function has the operations capacity to own those connectors, or whether the implicit integration tax inside a suite is actually the cheaper trade.

Brevo: the automation layer that pairs with a thin CRM

Brevo appears in two distinct positions on Reddit. Some teams use it as a full HubSpot replacement at the SMB end. More interesting for SaaS growth directors is the second pattern: Brevo as the automation layer that sits beside a thin CRM like Pipedrive, Zoho, or even a stripped-down Salesforce instance. Improvado's 2026 platform comparison endorses that framing, recommending Brevo or ActiveCampaign for SMBs with tight budgets and reserving HubSpot Marketing Hub for mid-market B2B companies in the 50 to 500 employee range 7.

The economics are the entry point. Brevo's volume-based pricing decouples cost from contact list size, which is the dimension HubSpot Marketing Hub punishes hardest as databases grow past tens of thousands of records. A growth team running a long nurture program against a large but mostly dormant list will see Brevo's monthly bill behave very differently from HubSpot's, particularly once Marketing Hub Pro tier minimums kick in.

What Brevo gives up is the depth of attribution, lifecycle scoring, and reporting that HubSpot bundles into Marketing Hub Pro and Enterprise. For SaaS teams that already run product analytics in a dedicated tool and attribution in a warehouse-based system, that gap is irrelevant. The CRM holds the record. Brevo runs the email, SMS, and basic lifecycle automation. Reporting lives downstream. The orchestration logic, increasingly, lives somewhere else entirely. Teams adopting Brevo are not buying a HubSpot clone at lower cost; they are buying the specific slice of HubSpot they actually used, and choosing to add the rest only if and when they need it.

ActiveCampaign: SMB automation depth without the suite tax

ActiveCampaign occupies the slot Reddit users reach for when Brevo feels too light but HubSpot Marketing Hub feels too expensive for the automation work they actually need. Improvado groups it alongside Brevo as the credible SMB-to-lower-mid-market choice for B2B teams with tight budgets 7. Brevo's own competitor roundup includes ActiveCampaign in the same consideration set, which is notable because vendors typically resist naming the alternative that compares closest to their own positioning 6.

The platform's distinguishing feature is automation depth. Its visual workflow builder handles branching logic, conditional waits, and lifecycle scoring at a level closer to Marketing Hub Pro than to a basic ESP. For SaaS growth teams running multi-step onboarding nurtures, trial conversion sequences, or expansion campaigns tied to in-product behavior, that depth matters. The CRM functionality is lighter than Pipedrive or Zoho, which is why it usually appears as the marketing layer beside a separate sales CRM rather than as a standalone replacement for HubSpot's full footprint.

The decision ActiveCampaign forces is about where automation logic should live. Teams that pick it are choosing to keep sophisticated lifecycle programs while accepting that the system of record sits in a different product. That separation is harder to operate than a suite. It also produces a cleaner architecture once the connectors are stable, because the automation tool can be replaced independently of the CRM if either side stops fitting. For growth directors planning a three-year stack horizon, that optionality is often worth the integration overhead it creates in year one.

Stack economics: what each path actually costs to operate

Sticker price is the part of the decision that travels well in Reddit screenshots. The harder number is what the stack costs to operate once integration work, data sync drift, and reporting reconciliation are priced in. A useful frame is to think in five buckets rather than five products:

- Suite spend

- Modular spend

- Integration tax

- Reporting tax

- Orchestration spend

HubSpot Marketing Hub Pro plus Sales Hub Pro collapses the first three into a single line item and charges a premium for that consolidation. The modular alternatives lower the line item but shift cost into engineering and revops hours that rarely show up in a procurement comparison.

Improvado's 2026 platform comparison is the cleanest sourced guide to which path fits which company shape. It recommends HubSpot Marketing Hub for B2B mid-market companies in the 50 to 500 employee range, ActiveCampaign or Brevo for SMBs operating under tight budgets, and Customer.io for SaaS product-led growth motions 7. That guidance maps directly onto the stack choices growth directors actually make. A 75-person Series B with a sales-led motion and a small revops team tends to keep the suite because the integration tax exceeds the seat savings. A 30-person seed-stage SaaS with a product-led motion picks Brevo or ActiveCampaign beside a thin CRM because the suite features it would pay for sit unused. A 250-person Series C with a dedicated data team unbundles aggressively because the engineering hours are already on payroll.

The variables that determine whether modular beats suite are predictable:

- Total contact volume drives email automation cost, which is where Brevo's volume-based pricing diverges sharply from HubSpot's contact-tier pricing.

- Seat count drives CRM cost, which is where Pipedrive's flatter per-seat structure compounds against Sales Hub Pro across forty or more users.

- Custom object complexity drives Salesforce-versus-everyone-else economics, because the moment a data model needs more than HubSpot's standard objects, the migration math changes.

- Reporting requirements drive whether attribution lives inside the marketing tool or in a warehouse, and that single choice often determines whether the suite premium is worth paying.

The orchestration spend is the bucket most TCO models miss. A modular stack with five tools needs a layer that decides what gets executed, in what order, against which segments. Teams that skip that layer end up paying for it indirectly through manual coordination, missed handoffs, or an agency retainer that quietly absorbs the gap. Pricing the orchestration layer explicitly is what makes the stack economics honest, and it is the variable that has shifted most in the last eighteen months.

See How Leading SaaS Teams Replace HubSpot and Agencies With AI-Driven Execution

Request a walkthrough of AI-powered marketing operations purpose-built for multi-location and enterprise teams—automating content, PPC, and reporting at scale without agency markups or manual workflows.

The orchestration layer above whichever CRM you pick

The five tools above answer different versions of the same question: where does the customer record live, and what runs the email next to it. None of them answer the question that has moved to the top of the Reddit threads in the last year, which is who decides what gets executed across the stack in the first place. That decision used to sit inside an agency retainer or a senior marketer's head. It increasingly sits in a separate software layer, and the shape of that layer is what HubSpot's 2026 Spring Spotlight quietly conceded when it shipped AI Connectors that pipe CRM data into ChatGPT, Claude, Gemini, and Copilot rather than trying to absorb those models inside the suite 5.

Forrester's framing is the cleanest way to describe what is actually happening. The analyst firm introduced the B2B Revenue Marketing Platforms category to capture the convergence of marketing automation, customer data, and analytics into integrated revenue systems, evaluating providers across 23 criteria that go well beyond the workflow editor and form builder lineage of classic marketing automation 13, 16. The category exists because the orchestration work, deciding which segment gets which message in which channel against which goal, no longer fits neatly inside the CRM or the ESP. It needs its own home.

For a growth director who has just unbundled HubSpot into a Pipedrive plus Brevo stack, or a Salesforce plus ActiveCampaign stack, or a Zoho-only configuration, the orchestration layer is what closes the gap between owning five tools and running a coherent program. It is the layer that reads what the CRM knows, decides what content and campaigns the next thirty days require, and pushes execution into the automation tool, the ad platforms, and the publishing systems without waiting on a weekly status call. AI-driven platforms in this category, including Vectoron, sit above the CRM rather than replacing it, which is the architectural point that matters when the alternatives question is reframed as a stack question.

How to decide in the next 30 days

A 30-day decision window is enough to settle the architecture question without forcing a full migration.

- Week one belongs to data, not vendors. Pull the current HubSpot bill, separate Marketing Hub from Sales Hub line items, count active contacts, count paid seats, and list every workflow that touches revenue. Most teams discover that fewer than a dozen workflows do the real work, and that contact-tier pricing accounts for more of the bill than seat cost. That inventory is what turns the alternatives question from a vendor preference into an architecture choice.

- Week two is for shortlisting against motion, not features. Sales-led teams with heavy AE workflows should price a Pipedrive plus Brevo or ActiveCampaign configuration. Mid-market B2B teams in the 50 to 500 employee range should keep HubSpot in the running, because Improvado's 2026 guidance still places it as the fit for that band 7. Teams already inside an Adobe, Microsoft, or Salesforce footprint should price the incumbent path before assuming HubSpot is the default. Zoho One belongs on the list when tool consolidation matters more than depth.

- Week three is for the orchestration layer. Decide whether the next twelve months of execution will be coordinated by a person, an agency, or a software layer reading from the CRM directly. That choice, more than the CRM itself, determines whether the modular stack delivers the savings it promises. Vectoron is one option in that category.

- Week four is for the contract.

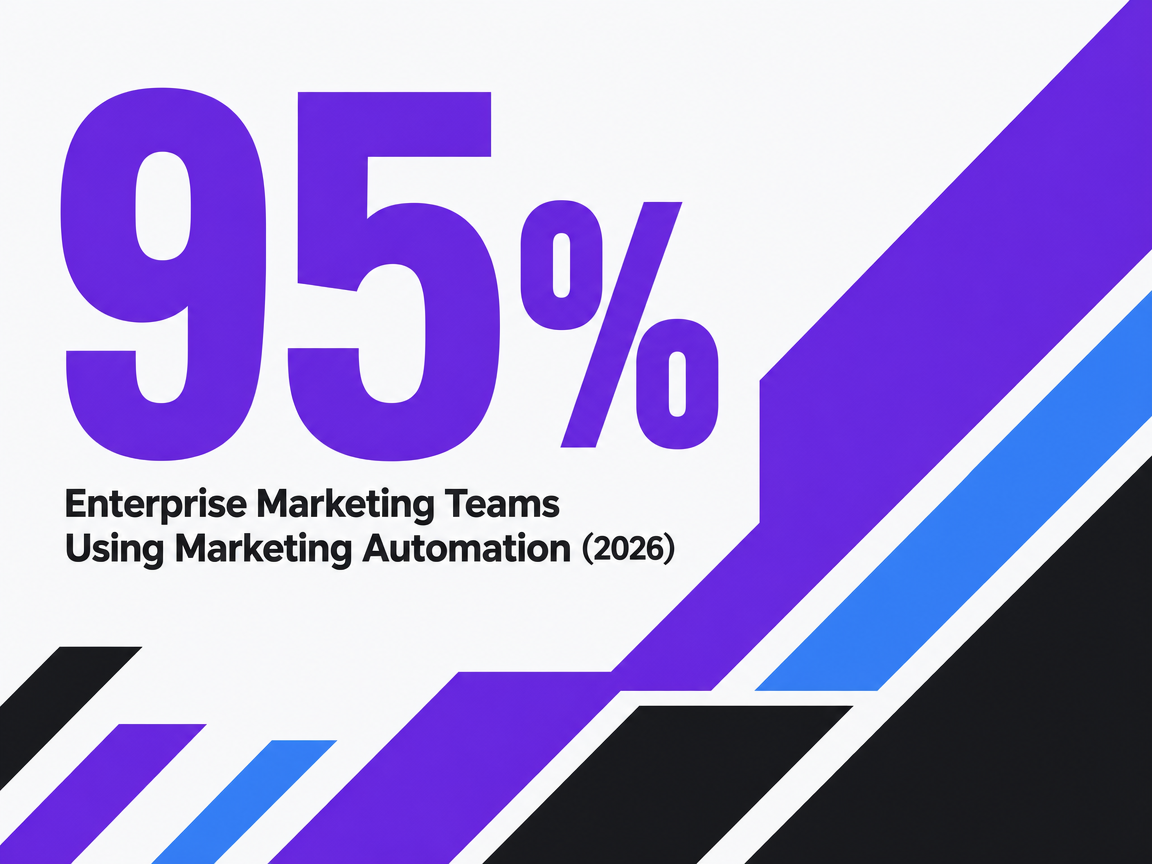

Enterprise Marketing Teams Using Marketing Automation (2026)

Enterprise Marketing Teams Using Marketing Automation (2026)

Enterprise Marketing Teams Using Marketing Automation (2026)

Frequently Asked Questions

References

- 1.B2B Marketing Automation Platforms Market Size, Growth, Share ....

- 2.Marketing Automation Statistics 2026: 130+ Key Metrics.

- 3.35+ Marketing Automation Statistics: The Definitive Guide.

- 4.The 8 best HubSpot alternatives in 2026 - Zapier.

- 5.From features to forward motion: what HubSpot's Spring Spotlight 2026 really means for B2B.

- 6.12 Best HubSpot Competitors (2026).

- 7.B2B Marketing Automation: 5 Best Platforms 2026 - Improvado.

- 8.FUTURE OF THE MARTECH STACK 2024 - Ascend2.

- 9.McKinsey: B2B buyers demand digitally enabled sales channels.

- 10.Future of B2B sales: The big reframe - McKinsey.

- 11.Marketing Technology Statistics: 30 Key MarTech Trends and Data ....

- 12.37 Must-Have MarTech Stack Tools for B2B in 2025.

- 13.The Forrester Wave™: B2B Revenue Marketing Platforms, Q3 2024.

- 14.The new B2B growth equation.

- 15.Artificial Intelligence Risk Management Framework: Generative Artificial Intelligence Profile.

- 16.Converging Platforms For Greater Efficiency: The Rise Of Revenue Marketing Platforms.