Key Takeaways

- AI execution platforms with human approval lead the ranking because flat account-level fees, parallel specialist lanes, and approval gates handle multi-site portfolios without the per-location cost creep retainers carry.

- Hybrid agency plus AI stacks take second place by pairing senior strategic judgment with automated production, fitting teams that need roadmap guidance without paying retainer rates for execution underneath.

- Full-service retainer agencies still win category launches, rebrands, and single-site programs where strategic depth matters, but linear scaling and coordination tax penalize them across multi-location footprints.

- Boutique technical and content specialists deliver scalpel-deep work on audits, schema, or programmatic builds, yet rarely sign BAAs 2and function better as contractors inside another execution model.

- In-house SEO pods offer institutional knowledge, brand voice control, and native compliance fit, but throughput and technical breadth break once a portfolio pushes past roughly five sites.

- Freelancer networks finish last because per-asset pricing optimizes unit cost while losing on multi-location fit, claims substantiation under FTC guidance 1, and BAA scope 2.

The execution model is the product now

Growth marketing directors searching for the best SEO services in 2025 are not shopping for a logo. They are deciding how SEO gets executed across a portfolio that probably includes a primary site, a content engine, a paid program, and — in healthcare and franchise contexts — anywhere from three to fifty location pages that all need to rank, convert, and stay compliant.

That shift matters. A decade ago, ranking the best SEO services meant ranking agencies. The work was opaque, the deliverables were monthly, and the differentiation lived in the strategist's head. The category has since fractured. Freelancer networks absorbed the cheap end. Boutique technical shops took the audits. In-house pods absorbed the strategy. Generative AI absorbed a meaningful share of the production layer, with peer-reviewed work already documenting its use in healthcare marketing and patient communication 3, 4. What is left for a director to evaluate is not vendors. It is execution models.

This ranking treats them that way. Six delivery models are scored against the metrics a growth director actually defends in a quarterly review: cost behavior as the program scales, content throughput, technical coverage, multi-location fit, compliance fitness, and the coordination tax that eats hours before a single asset publishes. Vendor names appear only as representatives of a model, not as the unit of comparison.

The headline finding, stated early so the rest of the piece can defend it: AI execution platforms with human approval now lead the ranking on operator metrics for multi-site portfolios. Full-service retainer agencies still win specific engagements. Hybrid stacks dominate the middle. The rest of the article shows the rubric, the scores, and where the model breaks.

How the ranking was built: a director's rubric

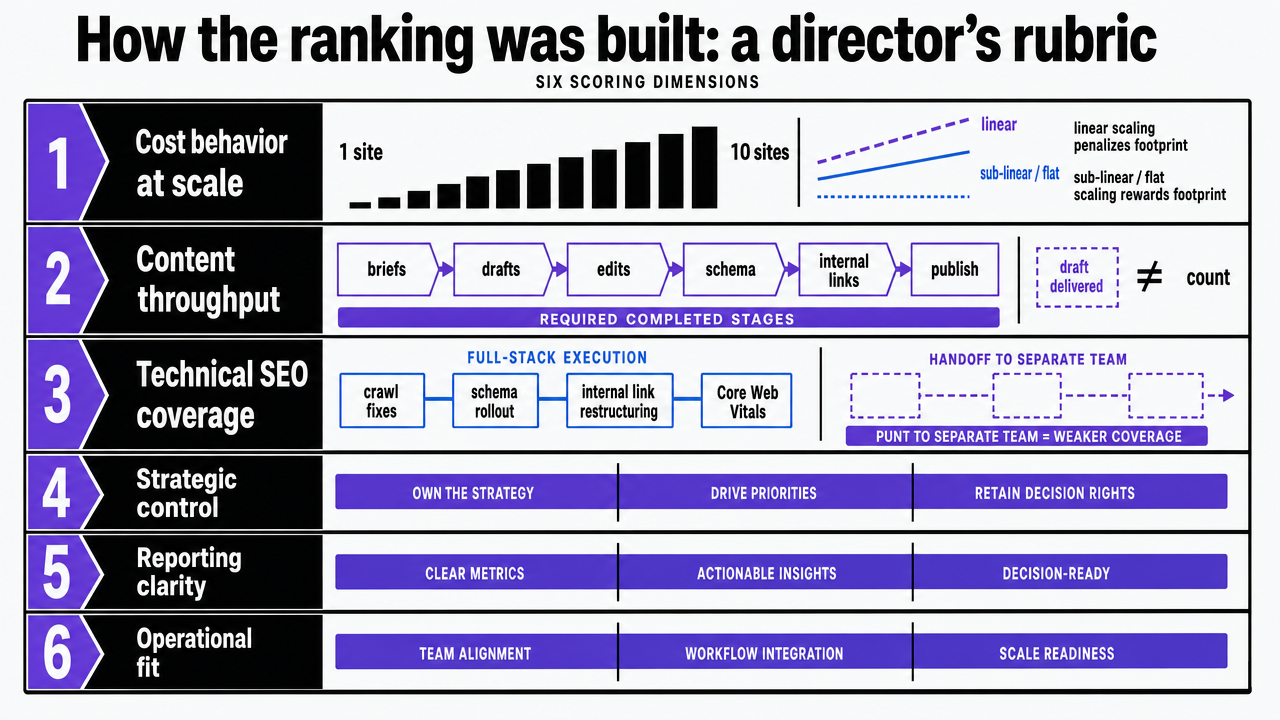

Every model in this ranking was scored against the same six dimensions, chosen because they map to the line items a growth director defends in budget review — not the ones a vendor likes to show in a pitch deck.

Cost behavior at scale. : Not the sticker price, but how the monthly spend moves when a portfolio grows from one site to ten. Linear scaling (per-location retainers, per-seat licenses) penalizes operators with footprint. Sub-linear or flat scaling rewards them.

Content throughput. : Published assets per month at a defined quality bar, including briefs, drafts, edits, schema, internal links, and publish. Velocity that stops at "draft delivered" does not count.

Technical SEO coverage. : Whether the model can actually execute crawl fixes, schema rollout, internal link restructuring, and Core Web Vitals work — or whether it punts those to a separate vendor.

Multi-location fit. : Whether strategy and execution run at the account level across many sites or get rebuilt site-by-site. Peer-reviewed work on omnichannel patient engagement already documents how brittle siloed execution becomes once locations multiply 6.

Compliance fitness. : For healthcare operators, this means the model can sit inside a HIPAA business associate framework where required 2and respect FTC obligations on health-related personalization and data use 1. For SaaS, it means defensible substantiation of claims.

Coordination tax. : Hours spent in status calls, brief reviews, approval threads, and rework — the invisible cost that eats the marketing team's week before a single asset ships.

Each model is scored qualitatively against these six. The ranking reflects the composite, not any single column.

Visualize the six-dimension scoring rubric used throughout the article, giving readers a reference frame before the model-by-model ranking

Visualize the six-dimension scoring rubric used throughout the article, giving readers a reference frame before the model-by-model ranking

Experience Automated SEO Execution Risk-Free Today

Test-drive full-scale SEO campaigns and publish live content without commitment during your trial period.

The six delivery models, ranked

1. AI execution platforms with human approval

AI execution platforms with a human approval gate top this ranking because they are the only model that posts strong scores across all six rubric dimensions for a multi-site portfolio. Strategy, content production, technical SEO, internal linking, schema, and link acquisition run as parallel execution lanes off a single account-level plan. A marketing director or compliance lead approves work at defined checkpoints before anything publishes. The platform fee is flat or near-flat as locations are added, which inverts the per-location math that defines retainer billing.

The operational shape matters. A 10-location dermatology group, a 30-site dental support organization, and a SaaS company with four product lines all share the same structural problem: strategy decisions made centrally have to fan out into coordinated execution across many surfaces. Peer-reviewed work on patient engagement already identified this as the integration challenge at the heart of multi-channel healthcare communication 6. Platforms solve it by treating the account, not the site, as the unit of work.

Throughput is where the model separates from the rest. Specialist lanes for content, technical, conversion, and backlinks run concurrently rather than queuing behind an account manager. Generative AI is now documented in peer-reviewed literature as a working layer for healthcare marketing content production and patient communication tasks 3, 4. The human approval gate is what keeps that throughput from becoming the scaled content abuse Google has warned against.

Where the model breaks: novel brand creative, original research projects, and crisis communications still benefit from a human strategist who can sit in a room with a clinical director and rewrite a positioning document. Platforms execute strategy well; they are not yet the right home for inventing it from a blank page.

Representative entries in this category include Vectoron, which scores AI platforms against the rubric described in section 2 with specialist lanes and an approval-driven Command Center.

2. Hybrid agency plus AI stack

Hybrid models pair a smaller human agency or in-house lead with an AI production layer underneath. A senior strategist owns the roadmap and the relationship; AI tools handle drafts, schema, technical audits, and reporting. The agency markup shrinks because headcount shrinks. Throughput rises because the bottleneck moves from "junior writer capacity" to "approval bandwidth."

This model scores well on content throughput and decently on technical coverage, but the rubric exposes two weak columns. Cost behavior is better than a pure retainer but still grows with locations, because the human partner usually bills time. Coordination tax stays meaningful: there is still an account manager, still a weekly call, still a separate tool stack the agency uses internally that the operator never sees.

The model earns its second-place ranking on a specific scenario. A growth team that needs senior strategic judgment on a complex roadmap — multi-brand portfolio rationalization, an international expansion, a regulated product launch — but does not want to pay a full-service retainer for the execution layer underneath. The hybrid arrangement buys the strategist's hours where they matter and pushes the rest to automation.

Where it breaks: most hybrid agencies are agencies first and AI users second. The AI layer is bolted onto an existing services business, which means quality varies wildly by which team is assigned. Operators evaluating this model should ask which AI tools the agency actually runs in production, who reviews the output, and what the agency's published-asset throughput per month looks like at current staffing. If the answers are vague, the hybrid label is marketing rather than operating reality.

For a SaaS director, this model fits when the company already has a strong internal SEO lead who needs leverage, not direction.

3. Full-service retainer agencies

The classic model — a monthly retainer, an account manager, a strategist, a content team, a technical lead, and a link-building function bundled under one contract. For one site, one brand, one roadmap, this is still a defensible choice. The retainer aligns incentives around a single account, and the agency owns the coordination problem internally.

The ranking falls in the middle because the rubric punishes the model on cost behavior and coordination tax. Retainers scale linearly with footprint: ten locations typically means ten times the scope, even if the strategy is the same across sites. Coordination overhead is the line item agencies do not advertise — weekly status calls, brief approvals, draft reviews, and rework loops eat the operator's calendar long before the asset publishes.

Full-service agencies score well on two columns the others struggle with: strategic depth and creative range. A senior strategist with twenty years of category experience is genuinely useful at the start of a program, during a rebrand, or when the operator is entering a new market. For a SaaS company launching a category-defining product, that judgment is worth the markup.

Where the model breaks: throughput is capped by junior staff hours, and quality drifts as the agency wins more accounts. Healthcare operators face a sharper version of the problem because a HIPAA business associate agreement 2and FTC obligations on health-related claims 1require compliance discipline that not every agency builds in. The retainer model is strongest for one-off strategic engagements and weakest for ongoing multi-site execution at scale.

4. Boutique technical and content specialists

Boutique shops specialize: technical SEO audits, schema rollout, programmatic content for travel and ecommerce, link acquisition only. They charge premium hourly or project rates and deliver narrow, deep work that a generalist agency cannot match.

For a growth director, the boutique is a scalpel, not a program. A specialist firm rebuilding a site's faceted navigation, fixing a six-figure crawl budget waste, or running a programmatic content build is often the right call. Scoring this model against a continuous-execution rubric, though, mostly highlights what it is not. Multi-location fit is low because boutiques engage per project, not per account. Coordination tax is high because operators have to integrate boutique outputs with whoever runs the rest of the program. Cost behavior is project-based, which is unpredictable rather than scalable.

The model ranks fourth because it is genuinely the best at one column of the rubric — depth on a specific technical or content discipline — and weak on the others. Operators get the most value when they hire a boutique as a contractor inside another execution model, not as the execution model itself.

Where it breaks for healthcare: boutiques rarely sign HIPAA business associate agreements 2, which limits what they can touch on patient-data-adjacent systems and forces awkward scope carve-outs. For SaaS, the limit is volume — a boutique that bills hourly does not scale to forty briefs a month without becoming an agency.

5. In-house SEO pods

An in-house pod usually means two to five people: an SEO lead, one or two content producers, sometimes a technical specialist, occasionally a dedicated link builder. Salaries plus benefits plus tooling produce a cost structure that grows in headcount steps rather than retainer increments.

The pod scores well on a few columns the rubric weights heavily: institutional knowledge, brand voice control, and direct accountability. Strategy lives inside the company, which matters for SaaS growth teams whose roadmap is tied to product launches the agency would not be looped into. Compliance fitness is also strong because the pod sits inside the company's existing data and legal governance — no external business associate agreement scope debate 2.

Where the pod ranks lower: throughput and multi-location fit. Five people cannot produce the volume of assets a 20-site healthcare operator needs without either burning out or quietly hiring contractors, at which point the pod has reinvented an agency on internal headcount. The model also struggles with technical coverage breadth — one specialist cannot stay current on Core Web Vitals, schema evolution, internal link architecture, and entity SEO all at once.

The pod is the right choice when the company has fewer than five sites, a strategic roadmap closely tied to product, and the patience to recruit specialists in a thin labor market. It is a poor choice when the volume math says the team would need to double in twelve months. Most pods that scale eventually adopt one of the AI execution layers above to keep up with their own roadmap.

6. Freelancer networks and marketplaces

Freelancer networks fill the bottom of the ranking because they optimize for one variable — unit cost of a draft — and lose on every other column the rubric measures. Per-asset pricing is low. Throughput is flexible in theory and unreliable in practice. Quality varies by individual contributor, not by the network, which means operators end up running their own editorial QA on top of the marketplace fee.

The model breaks immediately on multi-location fit and compliance. A freelance writer pulled from a marketplace will not sign a HIPAA business associate agreement 2, will not maintain a defensible audit trail of claims substantiation under FTC guidance for health-related content 1, and will not coordinate with the rest of the operator's program. Coordination tax is the highest of any model because the operator is now the project manager for every assignment.

Freelancer networks earn a place in the ranking only as a tactical overflow valve — a one-off brief, a translation, a niche subject expert for a single article. As an execution model for a continuous SEO program, they finish last.

Compliance fitness: where the ranking gets stress-tested

The rubric's compliance column is where most delivery models lose points they cannot recover. It is also where the ranking gets interesting, because compliance fitness is not just a legal checkbox — it is a proxy for whether the execution model was designed with governance in the architecture or bolted on after the fact.

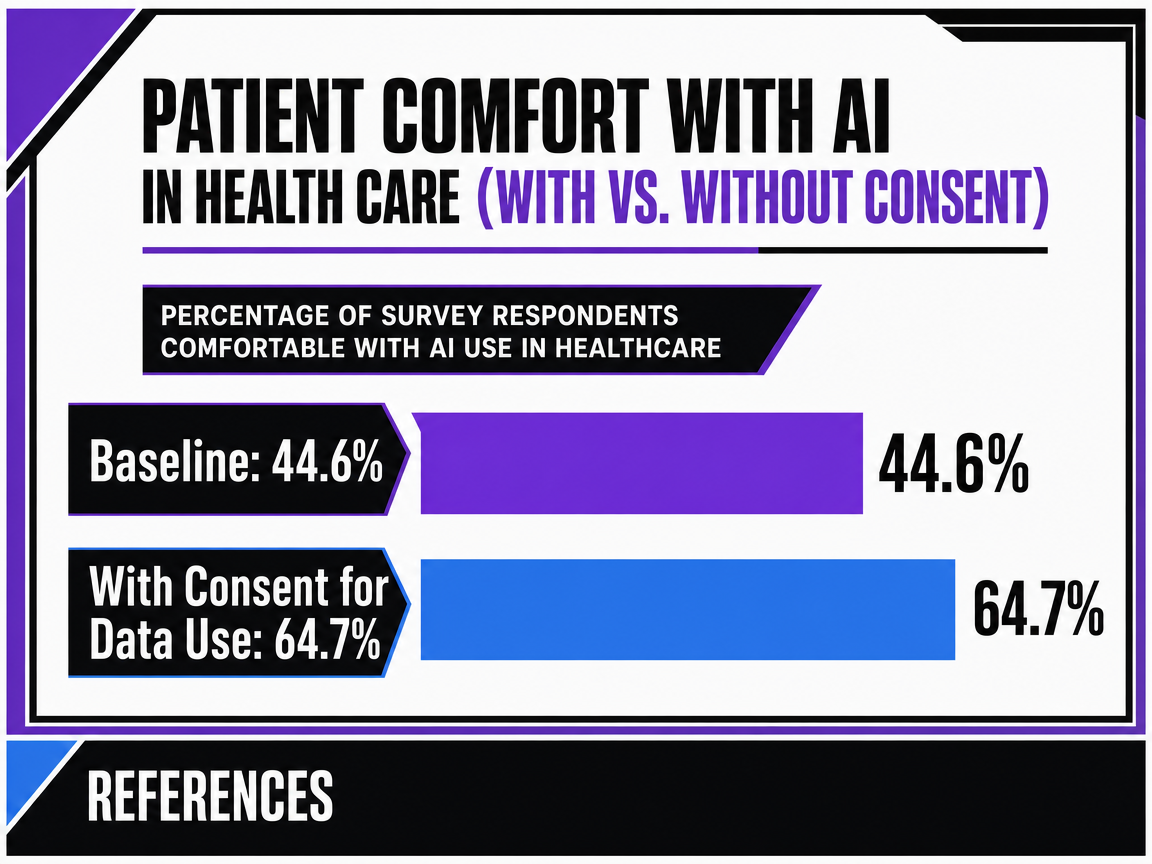

The stress test starts with patient acceptance, because acceptance shapes what marketing is allowed to say and how. A 2025 survey found that 44.6% of respondents were comfortable with AI use in healthcare at baseline, rising to 64.7% when personal health data were used with consent 8. The 20-point delta is the design instruction. Consent-aware governance is not a brand-safety nicety; it is the difference between a program patients tolerate and one they actively endorse. Models that route AI-assisted personalization through explicit consent capture and human approval inherit the higher number. Models that scrape together drafts from a marketplace and publish them across location pages inherit neither.

From there, the rubric applies two regulatory filters. The first is HIPAA scope: any vendor touching protected health information has to sit inside a business associate agreement that defines permitted uses and disclosures under the Privacy Rule 2. AI platforms, in-house pods, and full-service agencies can typically sign one. Freelancer networks and most boutique specialists cannot or will not. The second filter is the FTC's standing authority over deceptive practices and privacy or security failures involving personal information, which applies to mobile health apps, location pages making treatment claims, and any personalization tied to health signals 1. Substantiation discipline — keeping an audit trail of what was claimed, where the support came from, and who approved it — is what makes the difference defensible.

The scoping review on AI threats in healthcare adds the missing column: patient trust and acceptance depend on transparency and oversight, not just legal compliance 7. A delivery model can be technically inside HIPAA scope and still erode trust if patients cannot see where the human judgment sits. That is why the top of this ranking is reserved for models with explicit approval gates, not the ones with the most automation.

See Side-by-Side SEO Performance Metrics: Agency vs. Autonomous AI

Request a detailed comparison of multi-location SEO outcomes, execution speed, and cost efficiency between leading agencies and next-gen AI platforms—built for teams managing complex growth operations.

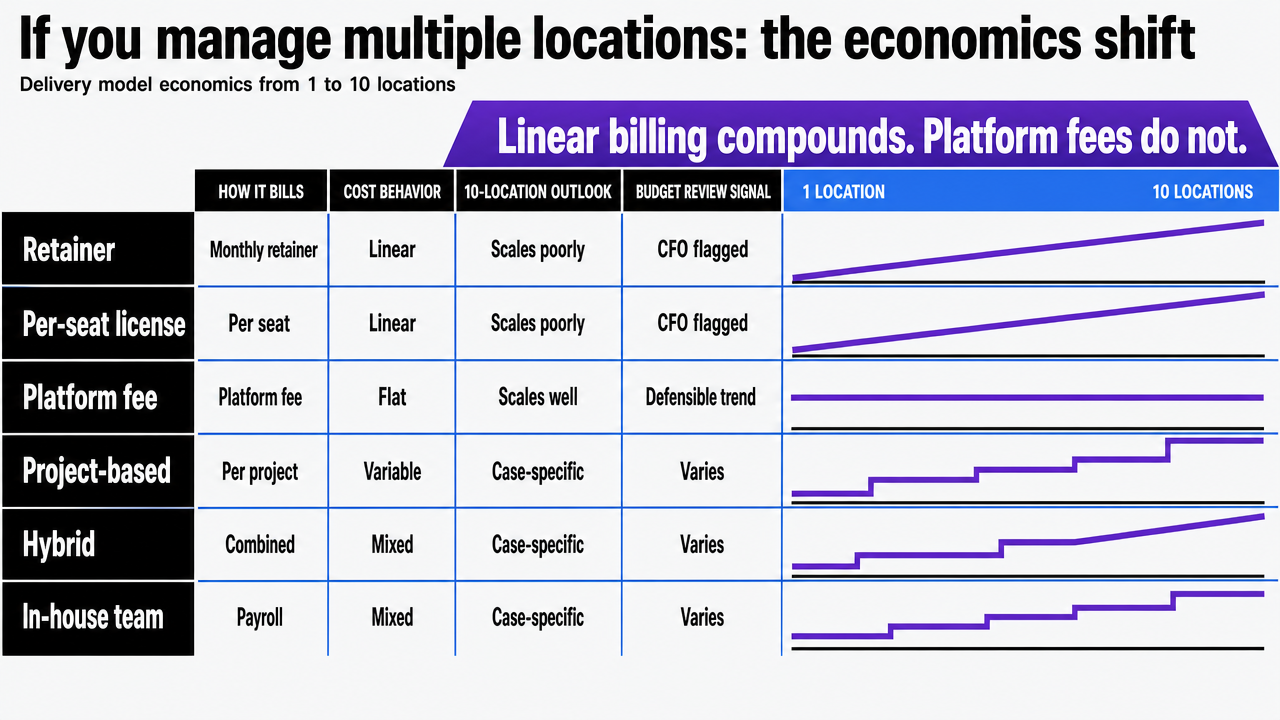

If you manage multiple locations: the economics shift

A note on audience scope: this section is written for operators running ten or more sites under one brand or holding company — multi-location healthcare groups, franchise systems, and SaaS companies with regional or product-line subsites. The single-site math in the rest of the ranking does not apply here.

The variable that breaks most delivery models at scale is not quality. It is how billing behaves when the operator adds the eleventh location. Retainers and per-seat licenses scale linearly. Platform fees do not. That difference compounds across a fiscal year and shows up in the budget review as either a defensible unit-cost trend or a line item the CFO flags.

The table below maps the six delivery models against the four columns that actually move at scale: how the model bills, how the cost behaves as locations are added, how much coordination overhead the operator absorbs, and whether the model can sit inside the regulatory perimeter healthcare operators need. Only one dollar figure appears — Vectoron's published $599/mo post-trial platform fee — because it is the single supplied price point. Every other cost is marked industry-variable; operators should drop in their own quotes rather than trust an invented number.

| Delivery model | Billing structure | Scaling behavior (1 → 10 locations) | Coordination overhead | Compliance fitness (HIPAA / FTC) ||---|---|---|---|---|| AI execution platform with human approval | Flat platform fee at account level (Vectoron: $599/mo post-trial; others industry-variable) | Flat to sub-linear | Low — approval gate replaces account-manager layer | Strong when vendor signs BAA 2and supports audit trail for health claims 1|| Hybrid agency + AI stack | Retainer plus tool seats (industry-variable) | Sub-linear on production, linear on strategist hours | Medium — fewer humans, still weekly cycles | Depends on agency's BAA willingness 2|| Full-service retainer agency | Monthly retainer, often per-site or per-scope (industry-variable) | Linear | High — account managers, status calls, brief loops | Strong with mature agencies; varies by shop 2|| Boutique technical/content specialist | Project or hourly (industry-variable) | Project-based, unpredictable | High — operator integrates outputs | Limited; most decline BAA scope 2|| In-house SEO pod | Salaries + benefits + tooling (operator-supplied input) | Step function at each new hire | Internal but real | Strong — inside existing governance || Freelancer network | Per-asset (industry-variable) | Linear with volume | Highest — operator project-manages | Weak — no BAA, no claims audit trail 1, 2|

Two readings of the table matter. First, only two rows hold their cost line as locations are added: the AI execution platform and, partially, the hybrid stack on its production layer. Everything else grows with footprint. Second, the compliance column is binary in practice. A delivery model either signs a business associate agreement that defines permitted uses and disclosures under the HIPAA Privacy Rule 2and maintains the substantiation trail the FTC expects on health-related claims 1, or it does not. There is no partial credit at audit time.

The operational takeaway for a director managing a multi-site portfolio: model the next twenty-four months at the location count you actually plan to operate, not the one you have today. The delivery model that wins at three sites is rarely the one that wins at fifteen.

Visualize the comparison table of six delivery models scaling from 1 to 10 locations, supporting the section's core claim about linear vs. flat cost behavior

Visualize the comparison table of six delivery models scaling from 1 to 10 locations, supporting the section's core claim about linear vs. flat cost behavior

What changes when you actually pick one

Picking a delivery model is the easy part. The harder work starts in the ninety days after the contract is signed, when the org chart, the approval flow, and the measurement system all have to bend to fit the choice.

Three changes show up first.

- Approval authority concentrates. Whoever signs off on published content becomes the rate-limiter for the entire program, which is fine if that person has bandwidth and clear standards, and a quiet disaster if they do not.

- Reporting cadence shortens. Platform-led and hybrid models produce data weekly or daily; quarterly business reviews stop being the unit of accountability.

- Tooling consolidates. The seat licenses, briefing docs, and screenshot threads that defined the agency relationship collapse into one workspace or get replaced entirely.

For healthcare operators, a fourth change matters more than the others: the governance perimeter has to be drawn on day one. Which vendor signs the business associate agreement, which assets touch patient data, and where the audit trail for health claims lives are decisions that get expensive to revisit 1, 2.

The rubric picks the model. The first ninety days decide whether the model actually delivers what the rubric promised.

Patient Comfort with AI in Health Care (With vs. Without Consent)

Patient Comfort with AI in Health Care (With vs. Without Consent)

Comparison of the percentage of survey respondents comfortable with AI use in healthcare, showing a significant increase when consent for personal health data use is given.

Frequently Asked Questions

References

- 1.Mobile Health App Interactive Tool | Federal Trade Commission.

- 2.What may a HIPAA covered entity's business associate agreement authorize?.

- 3.Generative Artificial Intelligence Use in Healthcare - PMC.

- 4.Role of Artificial Intelligence (AI) in Patient Education and Communication - PMC.

- 5.Chatbots in Health Care: Connecting Patients to Information.

- 6.Omnichannel Communication to Boost Patient Engagement and Experience.

- 7.Artificial intelligence in healthcare: a scoping review of perceived threats.

- 8.Listening to Patients' Voices on the Use of AI in Health Care.

- 9.Use of AI-based tools for healthcare purposes: a survey study on perceived advantages and concerns.

- 10.Patients' Perceptions Toward Human–Artificial Intelligence Interaction in Health Care.