Key Takeaways

- Every public URL an advisor publishes is an advertisement under 17 CFR § 275.206(4)-1, so SEO pages function simultaneously as ranking assets and compliance artifacts subject to the Marketing Rule's seven prohibitions 9, 11.

- Testimonial blocks, third-party ratings, and Google reviews carry dual-track obligations under both SEC Marketing Rule conditions and FTC endorsement guidance, requiring clear disclosures on client status, compensation, and material conflicts 3, 11.

- Local SEO architecture must map each location URL to a jurisdiction where the firm holds required registrations, with named representatives and service claims matching what is operationally authorized in that state 2, 14.

- Principals should report qualified consultation rate, discovery-to-engagement conversion by source, disclosure visibility audits, intake uptime, and AUM attributable to organic search rather than sessions or keyword positions 8, 13.

Why Advisor SEO Is a Regulated Lead-Qualification System

Search visibility for financial planners is shaped less by ranking algorithms than by the Investment Advisers Act of 1940 and its 2020 modernized Marketing Rule, which treats most one-to-many digital communications as advertisements subject to seven general prohibitions and specific testimonial conditions 9, 11. A blog post, a service page, a Google Business profile description, and a downloadable retirement guide all sit inside that scope.

That reframes the work. Every URL is simultaneously a ranking asset and a compliance artifact, and the firms that design for both at once tend to convert better. Investors arrive primed to verify: the CFPB directs prospects to check IAPD and FINRA BrokerCheck before engaging anyone 10, and academic work on information search shows that the path from query to advice relationship runs through repeated trust checks, not a single click 8.

The practical implication for principals is straightforward. SEO should be measured by qualified consultation requests from asset-eligible prospects, not sessions or keyword positions. The sections that follow treat the SEC Marketing Rule, FTC endorsement guidance, and the FTC Safeguards Rule as the actual design spec for that pipeline.

The Marketing Rule Is the Real Design Spec

What Counts as an 'Advertisement' Under 17 CFR § 275.206(4)-1

The codified definition is broader than most marketers assume. Under 17 CFR § 275.206(4)-1, an advertisement covers "any direct or indirect communication an investment adviser makes to more than one person, or to one or more persons if the communication includes hypothetical performance," with limited exceptions 9. A homepage, a service page, a blog post indexed by Google, a downloadable retirement-readiness checklist, a YouTube explainer embedded on a content hub, and a LinkedIn post linking to a firm landing page all clear that threshold.

That definitional reach is the design constraint advisor SEO has to start from. The 2020 modernization consolidated and replaced the prior advertising and cash-solicitation rules and pulled testimonials, endorsements, and third-party ratings into a single framework with explicit conditions 11, 12. Anything published once and read by many is in scope.

One practical consequence: editorial content frequently treated as "informational" by content teams — a market commentary, a tax-law explainer, an inflation primer — is still an advertisement when the firm publishes it, even if the page never names a product or fee. The relevant question is not whether the page sells, but whether a reasonable investor could view it as promoting the adviser or its services. Firms that map every URL against that question avoid the most common compliance gap: assuming "thought leadership" sits outside the rule.

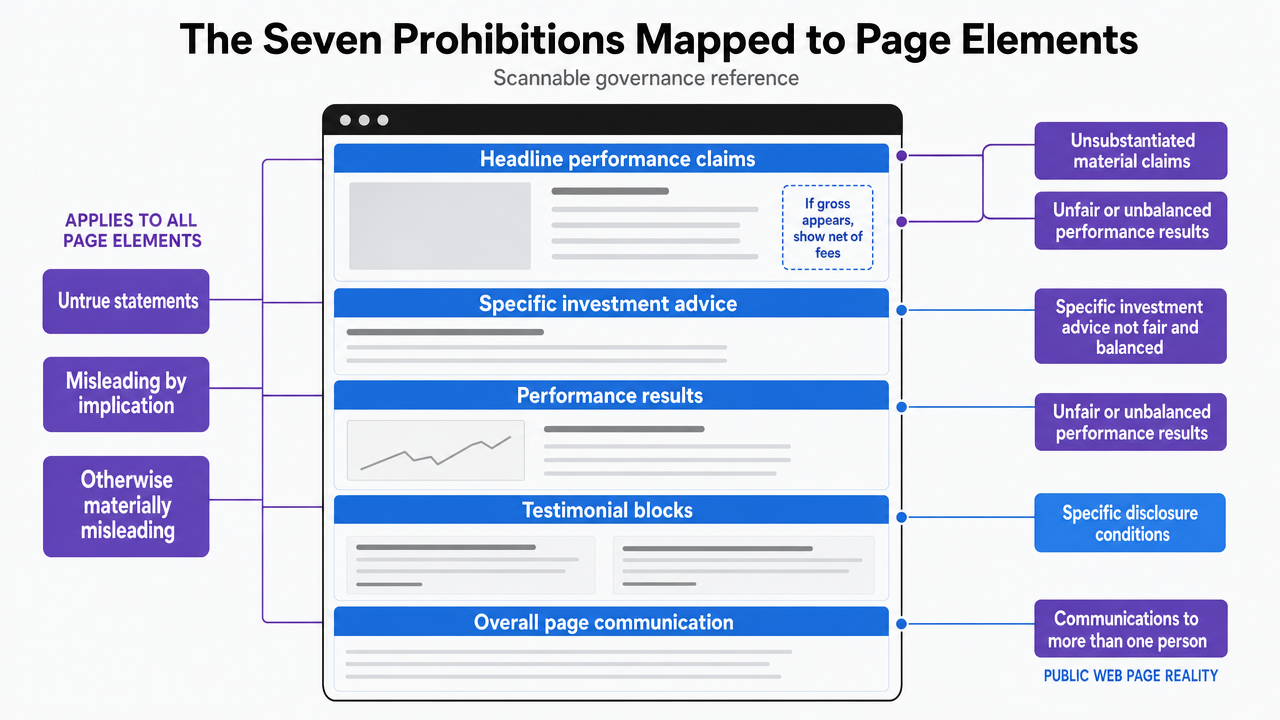

The Seven Prohibitions Mapped to Page Elements

The Marketing Rule sets seven general prohibitions: untrue statements, unsubstantiated material claims, statements that would mislead by implication, references to specific investment advice that are not presented in a fair and balanced manner, unfair or unbalanced inclusion or exclusion of performance results, and presentations that are otherwise materially misleading 9. The rule applies to communications made to more than one person, which is the operating reality of every public web page 11, 12.

Mapping the prohibitions to the actual surface of a landing page sharpens the work. Headline performance claims sit under the unsubstantiated-claim and balanced-presentation prohibitions and, when gross performance appears, must also show net-of-fees figures 12. Testimonial blocks must satisfy the rule's specific disclosure conditions on compensation, status of the endorser, and material conflicts 11. Case studies and "client story" modules trigger the fair-and-balanced requirement for references to specific investment advice, which usually means including unfavorable as well as favorable examples or a methodology disclosure 9. Adviser bios that imply expertise or outcomes — "helped clients retire early," "top-ranked planner" — pull in the unsubstantiated-claim and misleading-implication prohibitions unless the underlying support is documented and presentable on request.

The practical workflow is to assign each prohibition to a named page element and a named owner before the page is built, not after legal review flags it.

Visualize the seven Marketing Rule prohibitions mapped to specific page elements as described in this section, giving principals a scannable governance reference

Visualize the seven Marketing Rule prohibitions mapped to specific page elements as described in this section, giving principals a scannable governance reference

Performance References, Calculators, and Hypothetical Returns

Performance content is where SEO ambition and the Marketing Rule collide most often. When a public page presents gross performance, the rule requires net performance to accompany it, calculated over comparable periods and using the same methodology 12. That requirement applies to any composite, related performance figure, or representative account result the firm chooses to publish.

Hypothetical performance is the higher-risk surface. The rule pulls any communication that includes hypothetical performance into the advertisement definition even when sent to a single recipient, and it conditions use on policies and procedures designed to ensure the presentation is relevant to the likely financial situation and objectives of the intended audience 9. A public retirement calculator, a Monte Carlo widget, or a "what could your portfolio earn" tool indexed by search engines is, by default, distributed to an audience the firm cannot screen.

Firms that want calculators to rank should treat them as gated educational tools with documented assumptions, clear non-prediction language, and supervisory review of the model behind the output. Search-friendly calculator pages can still earn rankings; what they cannot do is publish projected return figures without the conditions the rule imposes 11.

Intent Mapping for an Audience That Verifies Before Booking

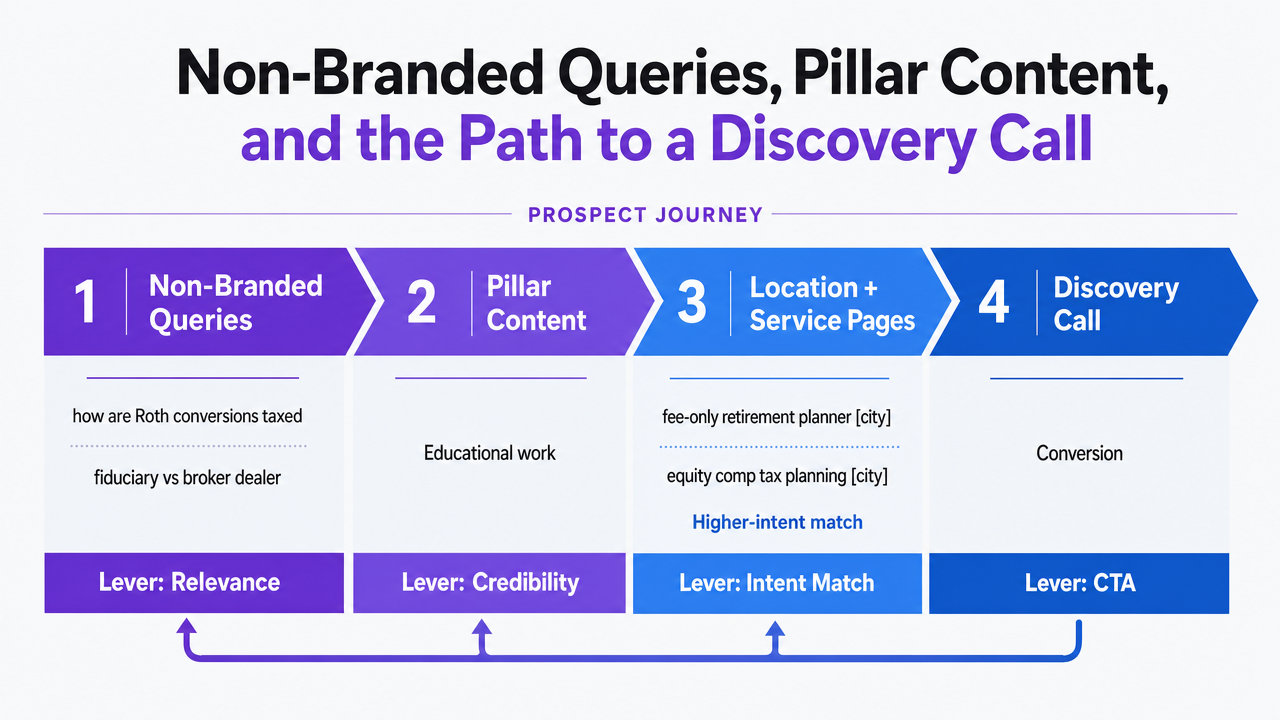

Non-Branded Queries, Pillar Content, and the Path to a Discovery Call

Prospects rarely arrive at a planner's site through a single query. Academic work on information search and financial advice use shows consumers move through a sequence of search and evaluation steps before engaging an adviser, with each step shaped by perceived relevance and credibility of the source 8. The implication for keyword strategy is concrete: non-branded informational queries ("how are Roth conversions taxed," "fiduciary vs broker dealer") sit at the top, and they should route to pillar content that does the educational work, not to a service page asking for a meeting.

Pillar pages then hand off to location and service landing pages that match a narrower, higher-intent query ("fee-only retirement planner [city]," "equity comp tax planning [city]"). The landing page exists to convert, and it carries the trust attributes investors actually weight when shortlisting an adviser: knowledge, trustworthiness, and listening skills 6. The consultation form sits on that page, governed by Safeguards Rule intake requirements covered later 13. Disclosure copy on any testimonial or endorsement block has to be clear and conspicuous, per FTC endorsement guidance, or the conversion lever silently becomes a compliance gap 3.

The funnel below names the operative lever at each stage so principals can audit a page against its actual job.

Visualize the four-stage prospect journey from non-branded query to discovery call described explicitly in this section, naming the operative lever at each stage

Visualize the four-stage prospect journey from non-branded query to discovery call described explicitly in this section, naming the operative lever at each stage

Content Pillars Anchored to What Clients Actually Weigh

Topic clusters earn their keep when they answer the questions a prospect uses to evaluate fit, not the ones the firm finds easiest to write about. Survey data synthesized by The American College of Financial Services finds that investors prioritize advisers who are knowledgeable, trustworthy, and good listeners, and a growing share want their portfolios to reflect ESG preferences 6. That maps to four durable pillars:

- technical planning depth (tax, retirement income, equity compensation, estate),

- fiduciary and fee transparency,

- communication and process, and

- values-aligned investing.

Each pillar should produce ranking content that signals the underlying attribute rather than asserting it. A piece on Roth conversion sequencing demonstrates technical depth; a page comparing fee-only, fee-based, and commission models demonstrates transparency; a process walkthrough of a first-year client engagement demonstrates listening and pacing. The CFPB directs prospects to verify credentials and registration history through IAPD and FINRA BrokerCheck before hiring anyone 10, which makes credential context inside pillar content a search-relevant trust signal, not boilerplate.

Pillars that lack a verifiable attribute behind them tend to underperform on both ranking and conversion. Firms get better results by trimming the pillar list to what the bench can actually substantiate.

Evaluate live SEO performance with real content

Test-drive data-driven SEO execution and see measurable impact before making any commitment.

Testimonials, Third-Party Ratings, and Reviews as a Compliance-Controlled Lever

Dual-Track Disclosure: Marketing Rule Conditions Plus FTC Material-Connection Rules

Two rulebooks govern a single testimonial block on an advisor's site, and they do not say the same thing. The SEC's modernized Marketing Rule permits testimonials and endorsements only when the firm provides clear and prominent disclosure of whether the speaker is a client, whether cash or non-cash compensation was paid, and whether material conflicts of interest exist 11. The codified rule layers on additional conditions: oversight of the endorser's compliance with the rule, written agreements when compensation exceeds the de minimis threshold, and disqualification screening for bad-actor endorsers 9. The Federal Register text confirms these conditions apply across advertisements as defined, which includes the SEO surfaces principals tend to think of as "reviews pages" or "client wins" 12.

FTC endorsement guidance runs in parallel. Endorsements must be truthful, must reflect honest experiences, and any material connection between endorser and firm has to be disclosed 3. The agency's FAQ resource makes clear that the rules apply across digital channels, including social posts that link back to ranking pages 4. The influencer disclosure guide adds placement specifics: disclosures must be easy to see and understand, and cannot be buried in a cluster of hashtags or pushed below a "read more" fold 5.

For SEO-driven pages, the operating rule is to draft testimonial copy and disclosure copy as a single unit. The disclosure sits adjacent to the quote, names the compensation status and client relationship in plain language, and remains visible on mobile. A five-star Google rating embedded on a service page carries the same dual-track obligation as a written quote, and the firm's compliance log should record which endorsements were paid, which were solicited, and which were screened for disqualifying events under the rule 9.

Review Behavior and Why Reputation Pages Earn Their Real Estate

Reputation surfaces convert because prospects look at them before they ever fill out a form. Pew Research Center found that 82% of U.S. adults at least sometimes read online ratings or reviews before purchasing items for the first time, based on a 2016 survey of general first-time purchase behavior across consumer categories rather than financial-advice engagements specifically 7. The figure travels because the underlying habit is durable, not because the study measured advisory shortlisting. Principals should read it as directional evidence that a governed reputation surface is worth the real estate, not as a benchmark to forecast against.

The operational question is how to build that surface without violating the conditions covered in the prior section. Three design choices tend to separate reputation pages that rank and convert from those that get rebuilt after a compliance review.

- The firm curates which third-party rating sources appear, since the Marketing Rule's testimonial and third-party rating conditions apply to whatever the site chooses to display 11.

- Disclosure copy is written once at the page template level so every quote inherits the required language about client status, compensation, and conflicts 3.

- The page links out to verification destinations prospects are already told to check — IAPD and FINRA BrokerCheck — which reinforces the trust signal the reviews are meant to carry 10.

A reputation page built that way functions as a ranking asset and a vetted shortlist artifact at once.

US adults who read online reviews before first-time purchases

US adults who read online reviews before first-time purchases

US adults who read online reviews before first-time purchases

Local SEO Under State Adviser Registration

Jurisdictional Marketing Rules and Location Page Architecture

Local search visibility for advisers is bounded by where the firm or its personnel are actually registered. State securities regulators set registration and compliance expectations for investment adviser representatives operating in a given jurisdiction, and those expectations extend to how the firm presents itself in that market 14. A location page that ranks for "fee-only retirement planner [city]" but lists no registered representative in that state is a compliance exposure, not just a thin SEO page.

Architecture follows from that constraint. Each location URL should map one-to-one with a jurisdiction where the firm holds the registrations required to solicit and advise, and the page copy should name the registered representatives associated with that office. Service descriptions need to align with what the firm is actually authorized to deliver in-state, since the 2024 internet adviser exemption release reinforced that website-based service claims have to match operational reality 1, 2. Generic "we serve clients nationwide" copy on a city page invites both a state-level inquiry and an underwhelming local ranking signal.

The seven Marketing Rule prohibitions apply identically to local pages, so testimonial blocks, performance language, and credential references on a city page carry the same disclosure load as the homepage 9. Firms that templatize disclosure copy at the location-page level avoid drift as new offices come online.

Surfacing IAPD, BrokerCheck, and Credentials on Adviser Bios

Adviser bio pages convert when they answer the verification questions prospects are already told to ask. The CFPB directs consumers to check the SEC's Investment Adviser Public Disclosure system and FINRA BrokerCheck and to weight advanced education and recognized certifications when shortlisting a professional 10. A bio that links directly to the representative's IAPD or BrokerCheck record shortens that verification step instead of forcing the prospect to leave and search.

The structural elements worth surfacing are concrete:

- full legal name as registered,

- CRD number,

- state registrations relevant to the office,

- fiduciary status,

- compensation model, and

- named certifications with issuing body.

Each of these doubles as an entity signal search engines use to disambiguate practitioners with similar names. Credential claims sit under the Marketing Rule's unsubstantiated-claim prohibition, so "award-winning" or "top-ranked" language needs documented support on file 9. A bio built this way functions as a ranking page and a pre-vetting artifact in one pass.

Lead Capture Is Covered by the Safeguards Rule

The moment a consultation form collects a name and email on an advisor's website, the page falls inside the FTC Safeguards Rule. Covered financial institutions are required to develop, implement, and maintain a written information security program that protects customer information, and the obligation extends to the systems and vendors handling that intake 13. SEO teams that treat the lead form as a conversion widget separate from the security stack tend to discover the overlap during a regulator inquiry rather than a design review.

Three intake decisions sit downstream of that rule.

- Form fields should collect the minimum data needed to qualify the consultation — investable asset bracket, planning need, jurisdiction — rather than full financial detail before the discovery call.

- Hosting and form vendors become in-scope service providers, which means contracts, access controls, and breach-notification terms have to match the written program rather than the marketing team's procurement preference.

- Embedded chat widgets, calendar bookings, and gated-content gates that capture identifiers carry the same obligations as the primary form.

There is a second-order point for digital-first firms. The SEC's 2024 update to the internet adviser exemption requires advisers relying on it to maintain at all times an operational interactive website providing digital investment advisory services on an ongoing basis 1, 2. A lead form that breaks, a calculator that goes offline, or an intake vendor that fails uptime is not just an SEO drag — it can puncture the exemption a digital-first model depends on. Intake reliability and intake security are the same operational discipline.

See How Top Financial Planners Streamline SEO Execution With AI Coordination

Request a walkthrough of integrated, approval-first SEO workflows designed for compliance-driven financial services teams—built for agencies and enterprises managing complex, multi-channel campaigns.

If a Firm Operates Across Multiple Offices or States

The audience shifts here from solo practitioners and single-office RIAs to firms with multiple offices, multi-state registrations, or both. The SEO footprint scales non-linearly because each new jurisdiction adds registration verification, location pages, testimonial governance load, and intake vendor scope.

Principals planning that expansion can use the comparison below to size the operational lift before commissioning the build.

| SEO footprint dimension | Single office, single state | Multi-office, same state | Multi-state firm |

|---|---|---|---|

| State registrations to verify against location copy 14 | One; align bio and service claims with one jurisdiction | One; verify each office’s registered representatives are listed accurately | One per state of operation; reconcile each location page to its jurisdiction’s rules |

| Location and landing page count | Homepage plus service pages; no city-specific URLs required | One location URL per office, each naming registered representatives | One location URL per office plus state-level pillar pages where service scope differs |

| Testimonial governance review load 9, 11 | Single template with one disclosure block | Shared template; per-office endorser screening and conflict logging | Shared template; per-state review where state rules layer additional conditions on top of the Marketing Rule |

| Intake and Safeguards Rule vendor scope 13 | One form vendor, one CRM, one written information security program | Same vendor stack; access controls scoped to office-level users | Same vendor stack; written program documents jurisdictional data handling and breach-notification variance |

Two patterns separate firms that scale cleanly from those that paper over the gaps. Testimonial and disclosure copy lives at the template level, not the page level, so a new office inherits the governed block instead of regenerating it. And the 2024 internet adviser exemption update tightened service-description accuracy across the web presence 1, 2, which means a multi-state firm cannot use the same generic copy on every city page without re-verifying that the named services are authorized in each jurisdiction.

Measuring Pipeline Quality, Not Traffic

Sessions and keyword positions answer the wrong question for a principal reporting to partners. The metric that matters is whether non-branded organic search produced consultation requests from prospects who clear the firm's asset and planning-need thresholds, and whether those consultations converted into engagements. Research on information search and financial advice use shows prospects move through repeated evaluation steps before booking, which means a single SEO touch rarely closes the loop on its own 8. Reporting has to follow the actual path.

Five measurements tend to carry the weight.

- Qualified consultation request rate, defined as forms that pass the firm's pre-screen on investable assets and jurisdiction.

- Discovery-to-engagement conversion by source, so pillar content, location pages, and reputation pages can be compared on actual book-of-business contribution.

- Disclosure-block visibility on mobile, audited quarterly against Marketing Rule conditions on testimonials and third-party ratings 11.

- Intake form uptime and vendor incident logs, since the Safeguards Rule and the 2024 internet adviser exemption both treat operational reliability as a baseline expectation 13, 1.

- The fifth is the one most teams skip: the share of new assets under management traceable to organic search within a defined attribution window. That number is what the partnership actually wants reported.

Frequently Asked Questions

References

- 1.SEC Adopts Reforms Relating to Investment Advisers Operating Through the Internet.

- 2.Exemption for Certain Investment Advisers Operating Through the Internet.

- 3.Advertisement Endorsements.

- 4.FTC's Endorsement Guides: What People Are Asking.

- 5.Disclosures 101 for Social Media Influencers.

- 6.What Do Clients Want from Financial Advisors?.

- 7.Online reviews and ratings.

- 8.Information Search, Financial Advice Use, and Consumer Outcomes.

- 9.17 CFR § 275.206(4)-1 - Investment adviser marketing..

- 10.Choosing a financial professional.

- 11.SEC Adopts Modernized Marketing Rule for Investment Advisers.

- 12.Investment Adviser Marketing.

- 13.FTC Safeguards Rule: What Your Business Needs to Know.

- 14.Compliance Tips - Office of Financial Regulation.