Key Takeaways

- SEO procurement has shifted from comparing vendor deliverables to selecting an operating model that defends pipeline contribution and CAC payback inside a 25% growth envelope 10.

- The coordination tax across separate SEO, PPC, and link vendors shows up as conflicting recommendations, lagging reports, and duplicated discovery work that no invoice itemizes.

- Vendor scorecards weighted across 200 ranking signals miss what actually moves results: intent-satisfying content, backlinks, and user signals, plus readiness for AI-mediated extraction 6, 7.

- AI content governance is now a procurement filter, with NIST trustworthy-AI attributes and FTC substantiation pressure separating defensible vendors from those selling adjectives 2, 3.

The Operating Model Question Has Replaced the Vendor Shortlist

The SEO procurement conversation inside SaaS marketing organizations has changed shape. A decade ago, evaluating SEO services meant ranking three or four agencies on deliverables: keyword maps, content calendars, link velocity, technical audits. That checklist is still in circulation, but it answers the wrong question. The real question facing a VP of Marketing today is which operating model produces qualified pipeline at an acceptable CAC payback, not which vendor produces the most assets.

Two models now dominate the market, and they are not interchangeable. The first is the retainer execution shop, priced for human throughput and structured around monthly deliverable counts. The second is an integrated growth system that coordinates content, technical, paid search, and link acquisition against a single acquisition target. The gap between them is not service quality. It is whether the program can defend its budget line when the CFO asks what organic search contributed to pipeline last quarter, and at what marginal cost.

This matters because search itself is still where B2B buyers begin. Roughly 80% of B2B buyers use search engines in their research process, which keeps organic discovery central to SaaS pipeline math 8. What has changed is the surface area: AI Overviews intercept queries, ranking-factor obsession has been replaced by content quality and user-signal consolidation 6, and enterprise SEO programs are being asked to operate across AI-mediated discovery as well as the blue links 7.

The sections that follow treat SEO as an operating decision. The vendor shortlist is downstream of that choice.

Why SEO Efficiency Now Outranks SEO Output

Growth Compression Changes the Math

Private B2B SaaS growth has slowed. SaaS Capital's 2025 benchmark survey of private B2B SaaS companies reported median growth of 25%, down from 30% the prior year 10. That five-point compression is not a rounding error. It is the difference between a board that funds expansion and a board that asks every channel owner to defend their line item with a payback model.

For SEO, the consequence is structural. When growth was running at 30% or higher, organic programs could justify themselves on directional pipeline contribution and brand search lift. A retainer that produced twelve briefs a month and a steady backlink trickle was acceptable cover. Inside a 25% growth envelope, that posture stops working. Every dollar routed to organic competes against paid acquisition with clearer attribution, product-led signups with shorter feedback loops, and outbound motions priced per booked meeting.

The Pavilion 2024 benchmark report flagged decreasing revenue growth efficiency through 2023, which translates directly into tighter scrutiny of any channel that cannot tie its output to acquisition cost 9. SaaS marketing leaders are being asked a sharper question than they were two years ago: not whether SEO works, but whether the version of SEO currently funded is the most efficient way to convert a finite budget into qualified pipeline.

This is why output metrics—articles published, links acquired, average position—have lost their standing as primary KPIs. They measure activity inside a budget that no longer has slack for activity. The relevant scoreboard is marginal cost per pipeline dollar produced, which forces a different question about who is doing the work and how it is coordinated.

The operating model determines that math more than the tactics do. A program built on isolated deliverables will always carry more overhead per pipeline dollar than one where content, technical, and link decisions share a single acquisition target.

CAC Payback Is the Real Scoreboard

CFOs do not ask about domain authority. They ask how long it takes a new customer to repay the cost of acquiring them, and whether that window is moving in the right direction. CAC payback is the metric that connects every marketing channel—organic included—to the cash position of the business. SEO programs that cannot speak in those terms get reclassified as discretionary spend during the first budget review of a soft quarter.

The Pavilion 2024 SaaS benchmark report documented declining revenue growth efficiency, which means the average SaaS company is spending more to acquire each dollar of new revenue than it did during the prior cycle 9. That trend raises the bar for organic. A channel that historically justified itself through low marginal cost per lead now has to prove that its leads convert at a payback period the CFO will accept, not just at a volume the marketing dashboard will display.

Reframing SEO around CAC payback changes what gets measured. Pipeline-influenced revenue from organic sessions matters. Time-to-first-touch for accounts that close matters. The blended cost of producing the content, earning the links, and maintaining the technical surface matters as a single number, not three separate invoices. Rankings and traffic become diagnostic inputs, not headline results.

This is where the gap between operating models becomes visible. A retainer agency reports on deliverables and surface metrics because its contract is priced that way. An integrated program reports on pipeline contribution and unit economics because that is what the budget is being evaluated against. The reporting cadence a SaaS VP can take to a CFO without translation is a strong signal of whether the SEO function is built for the current growth environment.

Test Unified SEO and Paid Campaign Execution Now

Experience coordinated SEO, content, and PPC workflows in your live environment before making a commitment.

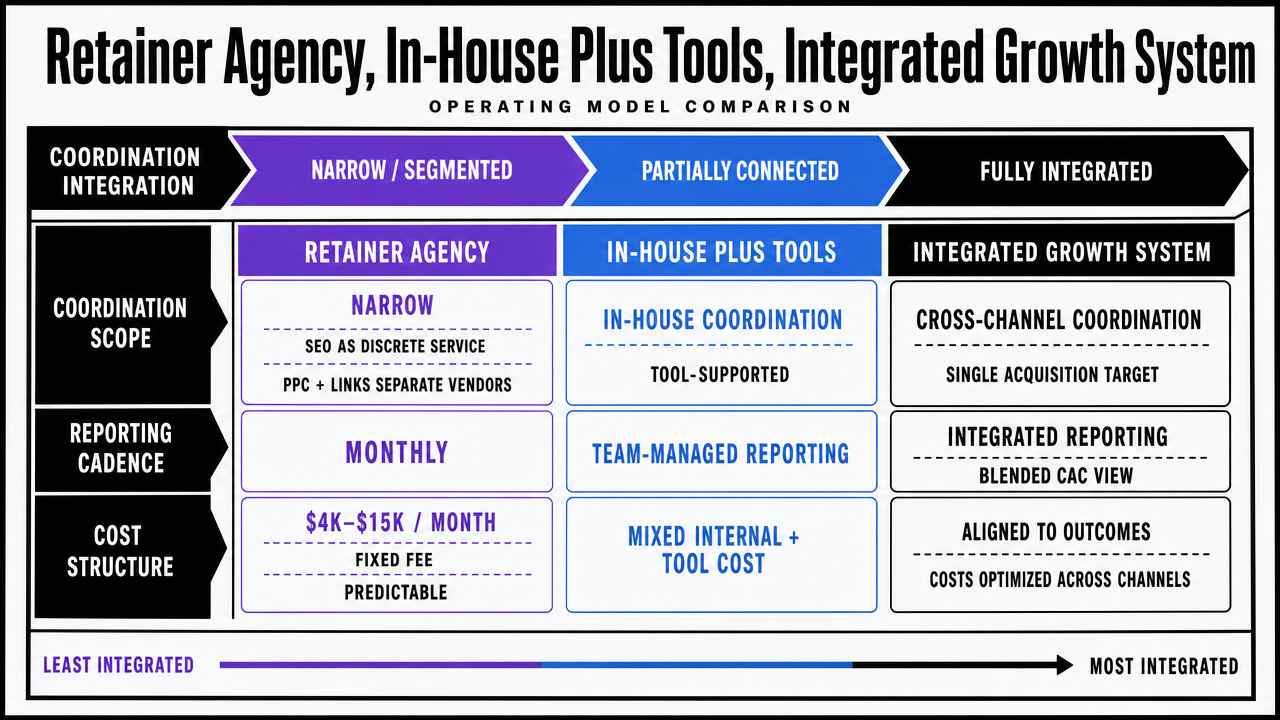

Three Operating Models, Compared on Coordination

Retainer Agency, In-House Plus Tools, Integrated Growth System

Three operating models dominate how SaaS marketing teams resource organic growth today, and they differ less on tactic quality than on how channels are coordinated against a single acquisition target.

The retainer agency model is the legacy default. A SaaS team pays a fixed monthly fee, typically in an industry-reported range of four to fifteen thousand dollars depending on scope, in exchange for a defined deliverable count: briefs, drafts, technical recommendations, and sometimes outreach for links. Reporting runs on a monthly cycle. Channel coordination is narrow—SEO is bought as a discrete service, with PPC and link acquisition usually contracted separately, often from different vendors. The cost structure is predictable, but the model treats organic as a standalone workstream rather than a contributor to blended CAC.

The in-house plus tools model trades agency margin for headcount and platform licenses. A SaaS company hires one to three SEO specialists and equips them with an enterprise platform, a rank tracker, a content brief tool, and a link prospecting subscription. Annual cost lands in a wider range depending on seniority and tooling depth. Output cadence is steadier than agency work, and channel coordination improves because the team sits closer to product marketing and demand gen. The limits show up in scale: a small in-house team cannot maintain content velocity, technical hygiene, and link acquisition simultaneously without either burnout or quality compression.

The integrated growth system is the newer entrant. It coordinates content, technical SEO, paid search, and link acquisition under one plan against one acquisition target, with reporting cycles measured in days rather than months. Cost is structured around the program, not the deliverable count, with entry points as low as the $599 monthly trial range used by some platforms in this category. The relevant question is not whether this model is cheaper per asset—it usually is not—but whether it produces a tighter CAC payback window than the alternatives, which is the trend the Pavilion 2024 benchmark report flagged as the new bar for SaaS channel efficiency 9.

Visualize the three operating models compared in this section across coordination scope, reporting cadence, and cost structure — directly supporting the comparison the section walks through

Visualize the three operating models compared in this section across coordination scope, reporting cadence, and cost structure — directly supporting the comparison the section walks through

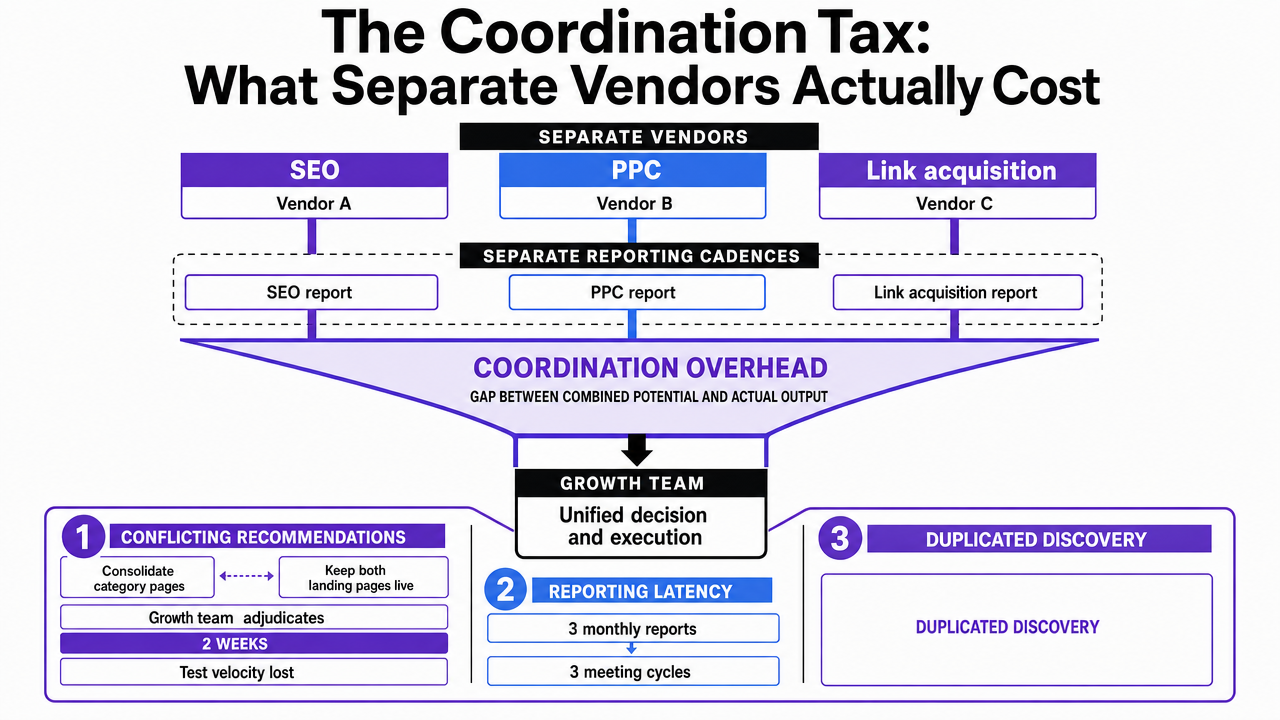

The Coordination Tax: What Separate Vendors Actually Cost

The coordination tax is the overhead a marketing organization absorbs when SEO, PPC, and link acquisition run as separate vendor relationships with separate reporting cadences. It rarely appears on an invoice, but it shows up in the gap between what the channels could produce together and what they actually produce apart.

The tax has three components:

- Conflicting recommendations. The SEO agency advises consolidating two product category pages to concentrate ranking authority. The PPC agency wants both pages live as distinct landing experiences for two ad groups with different match types. Neither vendor is wrong inside its own scope. The growth team spends two weeks adjudicating, and a quarter of test velocity disappears.

- Reporting latency. Three vendors mean three monthly reports, three meeting cycles, and three sets of attribution assumptions that do not reconcile. By the time a VP can see a unified view of pipeline contribution across organic, paid, and referred sessions, the data is six to eight weeks old. Decisions made on lagging composite reports are decisions made too late.

- Duplicated discovery work. Each vendor runs its own keyword research, competitor analysis, and audience segmentation, and each bills for it. The same target accounts get researched three times, the same competitor gaps get flagged three times, and the marketing team funds three parallel discovery functions that should be one.

None of this is hypothetical. It is the operating reality inside most mid-stage SaaS companies running a blended vendor stack. The cost does not appear as a line item, which is why it tends to be defended rather than measured. A useful diagnostic is to ask what percentage of the marketing leader's week is spent translating between vendor reports rather than acting on them. When that figure crosses twenty percent, the coordination tax has overtaken the channel performance it was supposed to enable, and the operating model—not the vendor roster—is the thing that needs to change.

Visualize the three named components of the coordination tax the section defines (conflicting recommendations, reporting latency, duplicated discovery), reinforcing the section's framework without inventing statistics

Visualize the three named components of the coordination tax the section defines (conflicting recommendations, reporting latency, duplicated discovery), reinforcing the section's framework without inventing statistics

Buying Criteria That Survive AI Overviews

Scorecards Built on 200 Ranking Factors Are Obsolete

The vendor scorecards that circulated through SaaS marketing teams five years ago are no longer diagnostic. They graded agencies on coverage of two hundred or more ranking signals, with separate columns for schema markup density, internal link ratios, anchor text diversity, and dozens of other inputs that read as rigorous but produced almost no decision value. Search Engine Journal's consolidation of the ranking-factor literature reduces the field to three categories that consistently move results: intent-satisfying content, backlinks, and user signals processed through systems like RankBrain, with the caveat that the weighting shifts by vertical and query type 6.

That consolidation has procurement consequences. A scorecard that awards equal weight to fifty micro-signals will rate two vendors as comparable when one produces content that resolves buyer intent and one produces content that hits a brief template. The first vendor earns rankings the second cannot. The scorecard cannot see the difference because it was built to measure activity, not intent satisfaction.

The replacement criterion is simpler and harder to game. For each priority query a SaaS team wants to own, the vendor should be able to describe what the searcher is trying to decide, what evidence resolves that decision, and how the proposed asset delivers that evidence better than the current top result. Vendors who answer in deliverable counts—word targets, link velocity, schema coverage—are operating on the obsolete model. Vendors who answer in intent and evidence are operating on the one Google's systems have been consolidating toward for several update cycles.

Readiness for AI-Mediated Discovery

AI Overviews and generative answer engines have changed where SaaS buyers encounter brand information for the first time. The question for procurement is no longer only whether a vendor can rank a page on Google. It is whether the vendor can structure content so that AI systems extract it accurately during the discovery, validation, and purchase stages of the buying cycle. Enterprise SEO commentary now treats search-generative experiences and AI-assisted search as core inputs to content strategy, not as edge cases 7.

A practical recommendation has emerged from the enterprise SEO platform discussion: rather than chasing visibility across every AI surface, most businesses should focus on Google plus one AI platform plus one community platform, and structure content for easy extraction by AI models across decision points in the buyer journey 11. For a SaaS team, that usually means Google, one of ChatGPT or Perplexity depending on where the ICP actually researches, and one community surface—Reddit, G2, or a category-specific forum where peer validation happens.

This collapses the vendor evaluation question into something concrete. Ask any prospective SEO partner how they structure content for AI extraction at each stage:

- Discovery-stage content needs definitional clarity and citable claims.

- Validation-stage content needs comparison frames and evidence the model can quote without distortion.

- Purchase-stage content needs unambiguous answers to objection patterns the buyer has already surfaced in earlier sessions.

A vendor that cannot articulate which content type belongs at which decision point is selling assets from the blue-link era to a buying process that has already moved past it.

Readiness is observable. Schema implementation, internal citation discipline, claim-evidence pairing inside paragraphs, and source attribution patterns all signal whether a content program is built for extraction or only for ranking.

See How Unified SEO, PPC, and Backlink Automation Drives Measurable SaaS Growth

Connect with a strategist to benchmark your current SEO service stack against autonomous, AI-driven marketing systems designed for SaaS and multi-location enterprises.

AI Content Governance as a Procurement Filter

Procurement teams now have a defensible reason to ask SEO vendors hard questions about how AI is used inside the content workflow. The reason is not aesthetic preference for human writing. It is regulatory exposure and trust-signal degradation, both of which a SaaS VP has to absorb if a vendor's process produces content that cannot withstand scrutiny.

The NIST AI Risk Management Framework defines trustworthy AI through a specific set of attributes: validity, safety, security, accountability, transparency, explainability, privacy, and fairness 2. These are not academic categories. They translate directly into procurement questions. Can the vendor explain how a given asset was produced? Can they document which claims were generated by a model and which were verified by a human reviewer? Can they demonstrate the editorial controls that catch factual drift before publication? A vendor that cannot answer in those terms is not necessarily producing bad content, but they are producing content the buyer cannot defend if a regulator, a customer, or a board member asks how it was made.

Content provenance is the second filter. NIST's report on synthetic content describes provenance tracking as a way to establish the authenticity, integrity, and credibility of digital material by recording its origin and history 1. For SaaS marketing programs publishing at any meaningful cadence, provenance is becoming part of the trust stack alongside backlinks and engagement signals. Vendors who treat AI as a black-box productivity multiplier, without records of model inputs, source verification, or human review checkpoints, are creating a future audit problem for the buyer.

The third filter is the claims the vendor makes about its own AI capabilities. The FTC's September 2024 enforcement sweep targeted companies that used AI as a vehicle for deceptive or unfair conduct, including fabricated reviews and misleading earnings claims 3. The relevant lesson for SaaS procurement is not that AI vendors are uniquely suspect. It is that exaggerated performance promises about AI-driven SEO output—10x content velocity, guaranteed ranking lift, autonomous link acquisition at unspecified quality—now sit inside a regulatory frame that did not exist two years ago. A vendor whose pitch deck cannot survive a substantiation review is a vendor whose contract cannot either.

These three filters collapse into a short diligence script. Ask how AI is used in production, what is documented, and which claims the vendor will put in writing. A partner operating on the right side of NIST's trustworthy AI attributes will answer in specifics. One operating on the wrong side will answer in adjectives.

What VPs Should Brief the CFO On

A CFO briefing on SEO is a budget defense, not a marketing update. The frame that holds up under scrutiny is unit economics: pipeline contribution, CAC payback, and the marginal cost of the next dollar of organic revenue. Everything else is supporting detail.

Four data points carry the conversation:

- The share of new pipeline influenced by organic search over the trailing four quarters, expressed as a percentage of total pipeline, with the absolute dollar figure attached.

- The blended monthly cost of producing that pipeline—content, technical, links, and platform fees rolled into one number rather than three vendor invoices.

- The implied CAC payback period for organic-sourced customers, compared against the company's blended target and against the SaaS efficiency trend Pavilion documented through 2023 9.

- The trajectory: is the marginal cost per pipeline dollar falling, flat, or rising over the last three quarters?

The macro context belongs in the briefing too, but only once. Private B2B SaaS median growth has compressed to 25% from 30% the prior year 10, which is the reason every channel is being asked to defend its line. That framing pre-empts the question before it gets asked.

Two items deserve explicit mention. AI Overviews and AI-mediated discovery have changed where buyers encounter the brand, which means traffic declines on some terms are expected and not a signal of program failure if pipeline contribution holds 7. And the operating model carries a coordination cost that does not appear on any single invoice—if the company runs SEO, PPC, and link acquisition through separate vendors, the briefing should quantify the internal hours spent reconciling their reports.

The CFO does not need rankings. They need to know whether the channel earns its place in the next budget cycle, and what changes if it does not.

Frequently Asked Questions

References

- 1.Reducing Risks Posed by Synthetic Content.

- 2.AI Risk Management Framework | NIST.

- 3.FTC Announces Crackdown on Deceptive AI Claims and Schemes.

- 4.McKinsey Technology Trends Outlook 2025.

- 5.Strengthening Multimedia Integrity in the Generative AI Era.

- 6.The Top 3 Google Ranking Factors That Really Matter.

- 7.5 Key Enterprise SEO And AI Trends For 2024.

- 8.B2B Marketing Statistics and Trends to Follow.

- 9.2024 B2B SaaS Performance Metrics Benchmark Report.

- 10.2025 Private B2B SaaS Company Growth Rate Benchmarks.

- 11.Current Trends in Enterprise SEO Platforms.